EU-UK: Politico-Reeves Will Call To Rebuild EU Ties

Politico reports that the UK's Chancellor of the Exchequer, Rachel Reeves, is set to call for ties with the European Union to be rebuilt. Politico reports an extract from the speech stating, "There are three big economic blocks: US, China and Europe. We will always seek every opportunity to grow our economy and these trading relationships, but ultimately only one of these is on our doorstep, and so the biggest prize is closer integration with Europe.”

- Reeves is due to speak at a Bruegel event at the LSE this evening at 18:00GMT (13:00ET, 19:00CET).

- Discussing Brexit has become of a 'third rail' for the governing centre-left Labour party, something that it avoids touching at all costs. In the 2016 referendum, Labour backed the Remain campaign. Prior to the UK formally leaving the EU in 2020, Labour supported a second referendum, but since then, under PM Sir Keir Starmer, it has not formally advocated for a new vote.

- The issue has recently raised its head, with Health Secretary Wes Streeting appearing to back the UK joining a customs union with the EU in a Dec 2025 interview, despite this not being the gov'ts official position. This was seen as laying down a challenge to Starmer, a view that will only intensify amid today's reports that Streeting could look to oust the PM sooner rather than later.

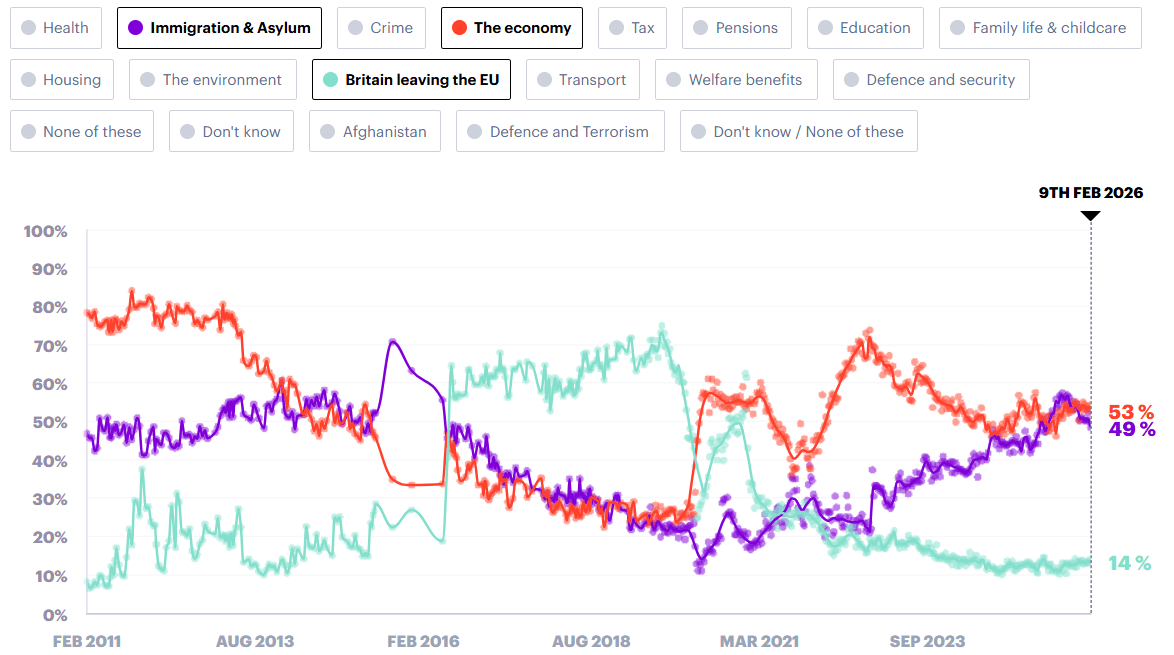

- The Brexit issue has slipped down the list of main political issues facing the country, according to polls. YouGov's issues tracker has just 14% of respondents in February selecting it as one of their three key issues, compared to 53% for the top issue (the economy) and 49% for immigration in second.

Chart 1. Opinion Polling, Most Important Issues Facing the Country, %

Source: YouGov

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD Slips as DoJ Targets Powell

- Greenback has stabilised at the session's lower levels, helping keep EURUSD propped toward 1.1700 and GBPUSD above the Friday high of 1.3451. Resultantly, the USD is weaker against all others in G10. The sustainability, and potential extension, of this USD weakness will take the lead from the US curve - which trades bear steeper so far Monday. Following Powell's video statement, it seems Trump's next comments on the topic are the primary market risk - even as the President denied knowledge of the filings over the weekend.

- The primary beneficiaries have been CHF and EUR as today's move slows, but only partially reverses, the YTD rally in USDCHF and YTD weakness in EURUSD. EUR's growing status as a haven is clear in the today's market reaction - and this will likely remain the case through near-term periods of market fragility, even as the outside pricing of ECB hikes further out the curve has faded.

- Despite the broad USD weakness, JPY has failed to receive a meaningful boost to start the week, with a brief flurry down to 157.52 well supported during APAC hours. Domestic factors are certainly playing their part here, as Friday’s reports of PM Takaichi dissolving the Lower House and associated speculation that she could call for a snap election continues to rise. The Yomiuri newspaper has reported that Feb. 8 or Feb. 15 are likely dates for this to occur.

- Technically, last week’s breach of 157.89 for USDJPY was a meaningful development, confirming a resumption of the medium-term uptrend. The next significant topside target will be 158.87, last year’s high and a key resistance. Support to watch lies much lower down at 155.35, the 50-day EMA.

- Typically for a Monday, there are no major data releases scheduled. This should keep focus on any potential comments concerning the Fed's subpoenas from Trump. The President is due at several public events later today, and also holds a call with the Mexican President. Central bank speak today includes Fed's Bostic, Barkin & Williams as well as ECB's Villeroy.

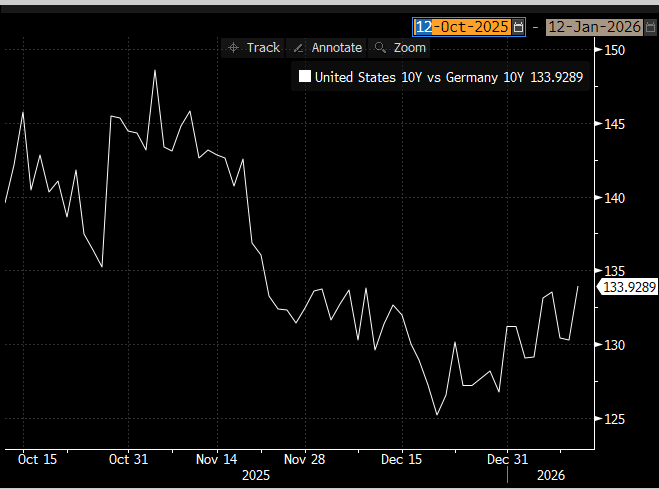

EGBS: Bunds Outperform Treasuries Amid Fresh Fed Independence Concerns

The German curve outperforms its US counterpart, with renewed concerns around Fed independence not spilling over into EGB markets. German yields are up to 1bp lower across the curve, with US yields flat to +5bps in a bear steepening move. The 10-year UST/Bund spread is 3.5bps wider at 134bps.

- Bund futures are unchanged at 127.95. The rally since last Monday does undermine the bear theme and attention is on resistance around the 50-day EMA, at 128.29. A clear break of this average would highlight a stronger reversal and signal scope for a continuation higher.

- The EFSF is holding a dual tranche syndication, launching a new 3- and 10-year bond. We expect a E5-7bln size.

- 10-year EGB spreads to Bunds are biased up to 0.5bps wider. Focus in France remains on budget negotiations, with scope for compromises seeming increasingly slim.

- Regional news flow hasn’t been too market moving. China and the EU have agreed on the need to provide guidance on price commitments for Chinese exporters of pure electric vehicles to the EU.

- Meanwhile, ECB’s Muller pushed back on near-term rate moves in either direction. In line with market pricing, he suggested a rate hike is possible “a few years ahead”.

- The Eurozone Sentix survey was stronger-than-expected at -1.8 (vs -5.0 cons, -6.2 prior).

Figure 1: 10-year UST/Bund Spread (Source: Bloomberg Finance L.P)

OPTIONS: Expiries for Jan12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1620(E625mln), $1.1630-50(E2.5bln), $1.1680(E536mln), $1.1800(E1.3bln)

- USD/JPY: Y157.00($848mln), Y157.85-00($1.5bln)

- AUD/USD: $0.6580(A$579mln), $0.6725(A$598mln)

- USD/CNY: Cny7.2000($547mln)