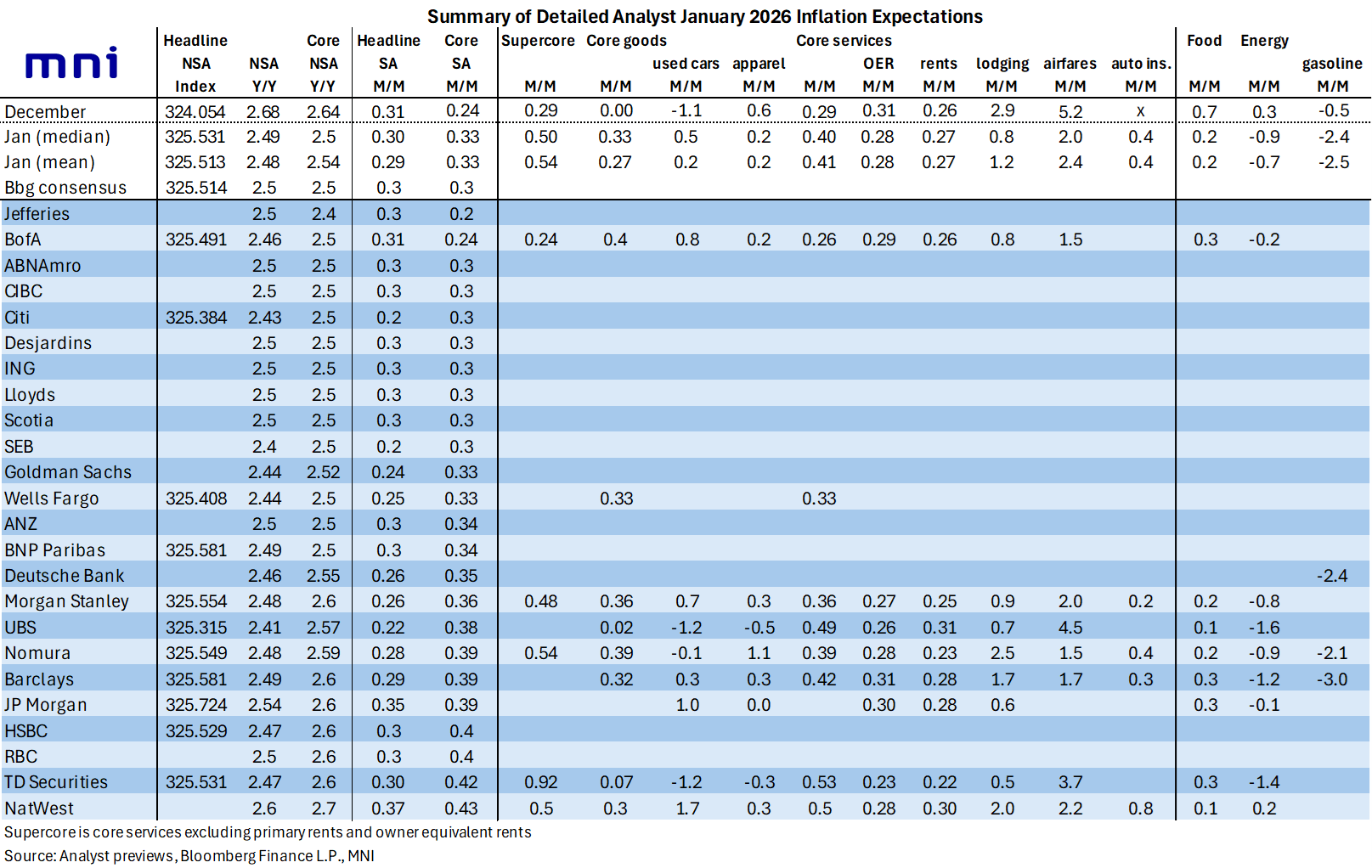

US PREVIEW: Used Cars and Smaller Services Behind Expected Core CPI Firming

Analysts look for the acceleration in core CPI to come from both goods and services:

- on the core goods side, used cars are on balance expected to play a large role in the sequential firming, shifting from -1.1% M/M in December to perhaps a small positive. That’s far from a uniform view though with an analyst range of -1.2% to 1.7%.

- going against this but with a smaller weight, apparel is on balance expected to moderate with a median 0.2% estimate after a strong 0.6% M/M in December.

- on the core services side, the sequential firming comes despite relative softening in some of the noisier non-housing categories that can swing broader inflation from month-to-month. In particular, airfares (no feed through to PCE) and lodging away from home (feeds through to PCE) are expected to moderate after strong increases in December.

- rental inflation is expected to be fractionally softer than in December, with an average estimate of 0.28% for OER (range 0.23-0.31) after 0.31% but tenants’ rents at 0.27% (range 0.22-0.31) after 0.26%.

- the gap, with these large service components at similar monthly pace/softer than in December likely reflects a residual seasonality boost expected more broadly.

Away from core CPI, headline inflation is expected to be weighed on by softer food and energy inflation.

- Food inflation is expected to moderate heavily after a far stronger than expected 0.7% M/M in December, its strongest monthly increase since Aug 2022 but also a move that looked suspiciously like a reversal of November holiday discounting (with the later than survey period back in November).

- Energy prices are also expected to have seen a reasonable seasonally adjusted decline after a modest increase in December. Note the wider than usual range to analyst estimates this month (from -1.6% to 0.2%) which we suspect is down to treatment of differing natural gas and electricity price assumptions.

[A quick reminder that the below table shows median/mean figures across all estimates. The core CPI median of 0.33% M/M would be 0.36% M/M if only taking unrounded estimates per the separate table shown above]

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EFSF ISSUANCE: Dual Tranche 3/10-year Syndication: Final terms

New 3-year Benchmark

- Size: E3bln

- Spread set at MS+5bps (guidance was MS +6bps area)

- Books closed in excess of E18bln (inc E1.3bln JLM interest)

- Coupon: Long first

- Maturity: Feb 2, 2029

- ISIN: EU000A2SCAW0

New 10-year Benchmark

- Size: E4bln

- Spread set at MS+30bps (guidance was MS +33bps area)

- Books closed in excess of E37.5bln (inc E2.1bln JLM interest)

- Coupon: Long first

- Maturity: Feb 1, 2036

- ISIN: EU000A2SCAX8

For both:

- Total Size: MNI expected E5-7bln with upside risks. The combined size is therefore the top of our expected range.

- Bookrunners: BARCLAYS (DM/B&D) / DB / GSBE SE

- Settlement: Jan 19, 2026 (T+5)

- Timing: Allocations and pricing to follow

From market source / MNI colour

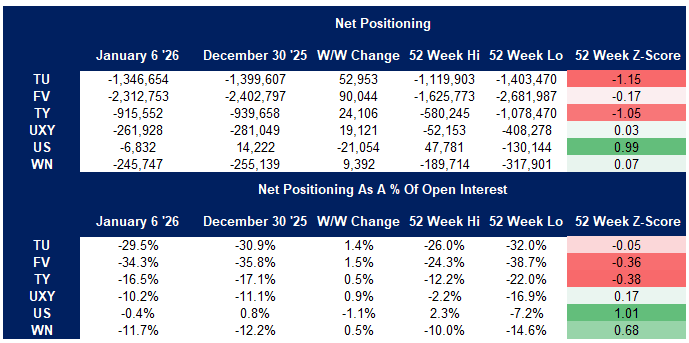

US TSY FUTURES: CFTC CoT Shows Asset Managers Remain Long, Funds Still Short

The latest CFTC report shows a reduction of non-commercial net shorts across much of the futures curve over the New Year period, with the only exception coming via US futures, which saw positioning revert to net short after a single week in net long territory (see table below for greater detail).

- Asset manager positioning was little changed in net DV01 terms, with instances of net long setting (TY, UXY & US) roughly offset by episodes of net long cover (TU, FV & WN). The cohort remains net long across

- Meanwhile, short cover dominated for hedge funds in net curve-wide DV01 terms (short setting in TU & US futures was outweighed by short cover in the remaining contracts). The cohort remains net short across the curve.

- We wouldn’t read too much into positioning swings over this period as they came over the end of the year and do not capture Friday’s post NFP swings (more to come on that in the daily OI bullet).

Source: MNi - Market Nws/CFTC/Bloomberg Finance L.P.

OUTLOOK: Price Signal Summary - S&P E-Minis Pullback Appears Corrective

- In the equity space, the trend structure in S&P E-Minis remains bullish and today’s move down is considered corrective. Price continues to trade above key support at 6771.50, the Dec 18 low. Clearance of this level is required to signal scope for a deeper retracement and would also highlight a possible short-term reversal. First support is at 6933.61, the 20-day EMA. For bulls, a fresh cycle high on Friday reinforces a bull theme. A resumption of the trend would open 7021.79, the 0.618 projection of the Nov 21 - Dec 11 - 18 price swing.

- A bull cycle in EUROSTOXX 50 futures remains intact. Gains last week confirm a resumption of the primary uptrend. Note that MA studies are in a bull-mode position, highlighting a dominant uptrend. The 6000.00 handle has been breached, signalling scope for 6086.99 next, a 1.236 projection of the Nov 21 - Dec 12 - 18 price swing. Firm support to watch is 5819.97, the 20-day EMA. A pullback would be considered corrective and allow an overbought condition to unwind. First support lies at 5912.00, the Jan 8 low.