MNI US MARKETS ANALYSIS - AI Sell Off Persists; Stocks Sink

Highlights:

- AI-led sell off leads e-mini S&P lower for a second session, further through the 100-dma

- Government bonds see support on stock weakness; US 10y yields pressed to a new November low

- US prelim PMIs and final UMich sentiment mark the data highlights

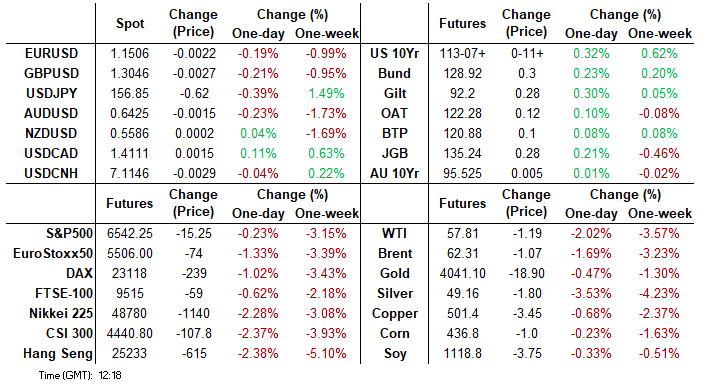

US TSYS: Off Latest Highs But Holding A Breach Of TY Resistance

Treasuries have extended post-payroll gains as US equity futures consolidate yesterday’s heavy AI-driven losses, amidst heavy volumes even allowing for roll activity. Today’s scheduled focus will be on front-loaded Fedspeak from current year voters and November flash PMIs.

- Cash yields are 1.7-2.8bp lower on the day, with declines led by 7s.

- Curves modestly extend yesterday’s post-NFP steepening, with 5s30s at 108bps off a two-month high of 108.8bps earlier today.

- TYZ5 trades at 113-07+ (+11+) off an earlier high of 113-10+ that has comfortably cleared resistance at 113-02, an area of congestion since Nov 5. It marks a bullish development and opens 113-18+ (Oct 28 high), also cancelling a recent short-term bearish theme.

- Volumes are elevated at 610k, boosted by the quarterly roll (estimate at now more than 30% complete) but still ~500k allowing for that.

- Data: Real av earnings Sep (0830ET), S&P Global US PMIs Nov prelim (0945ET), U.Mich consumer survey Nov final (1000ET), KC Fed services Nov (1100ET)

- Fedspeak: Williams (0730ET), Collins (0800ET), Barr (0830ET), Miran (0830ET), Jefferson (0845ET), Logan (0900ET) – see FED bullet.

- Politics: Trump meets with NYC Mayor-Elect Mamdani (1500ET)

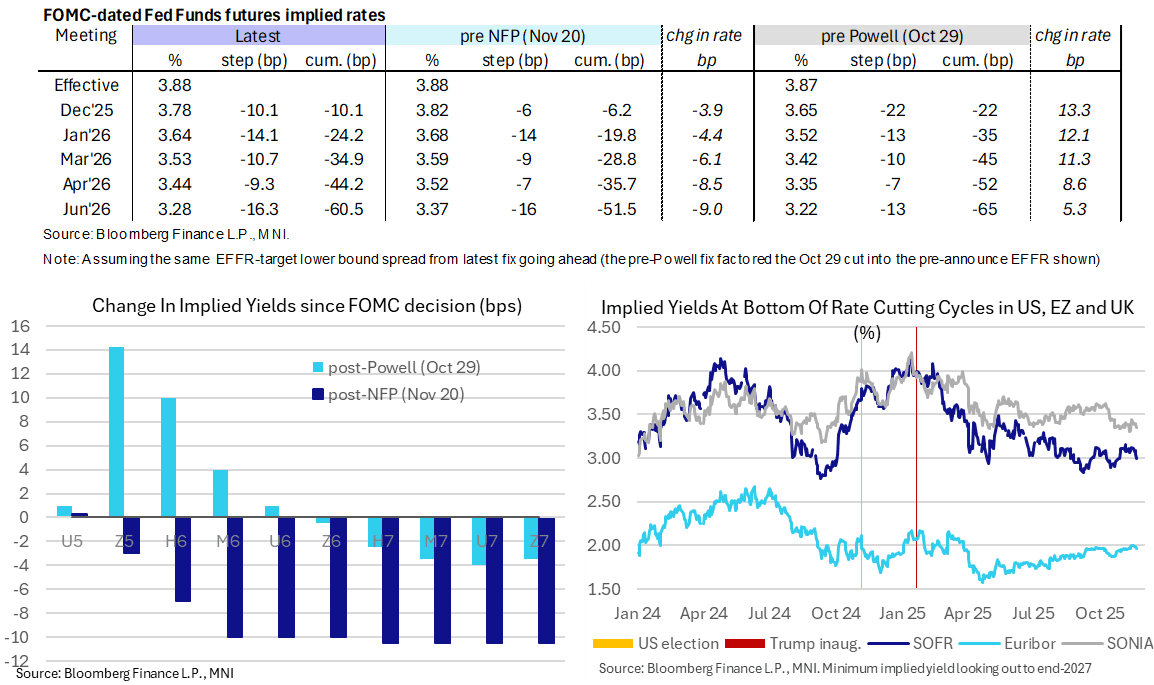

STIR: US Rates Extend Post-NFP Rally, Dec Pause Still Deemed Slightly In Favor

- Fed Funds implied rates are 0.5-1.5bp lower on the day for meetings out to mid-2026.

- Cut prospects for the Dec 9-10 FOMC meetings have increased to 10bp (+1bp from the close) vs as little as 6bp prior to yesterday’s September payrolls report, as investors continue to weigh up a higher unemployment rate against stronger than expected payrolls growth.

- It was 11-12bp prior to the BLS decision on Wednesday to roll the Oct establishment survey into the Nov payrolls release not due until Dec 16 (a delayed date also published at that time).

- Cumulative cuts from 3.87% effective: 10bp Dec, 24bp Jan, 35bp Mar, 44bp Apr, 60.5bp Jun.

- SOFR futures are 1 tick firmer for the SFRZ5 through to 4.5 ticks firmer through 2027 contracts as US equity futures consolidate yesterday’s heavy losses.

- The SOFR implied terminal yield has dipped under 3% (SFRH7) for fresh lows since Powell's Oct 29 FOMC press conference.

- Today’s heavy Fedspeak can help shape market assessments for next month’s meeting, with members yesterday not sounding concerned, along with the flash November PMIs.

- JPMorgan and Morgan Stanley both altered their Fed calls yesterday, eyeing no change next month. JPM see cuts in Jan and May before going on hold, MS see cuts in Jan, Apr and June for the same 3-3.25% terminal they had pre-payrolls.

FED: Front-Loaded Fedspeak To Offer Current Voter Views On Payrolls

- It’s another heavy schedule for Fedspeak today, this time more front-loaded, and importantly with five of the six speakers voting at next month’s FOMC meeting (four are permanent voters) and Logan to have a voting role from January.

- Focus will be on their reaction to yesterday’s September payrolls report. Barring an ever dovish Miran, FOMC members so far haven’t appeared concerned by the rise in the u/e rate to 4.44% in September.

- Goolsbee (’25) said the latest data including the September payrolls report didn't change his mind that the labor market has cooled but has largely been stable, with recent gains near the Chicago Fed's breakeven rate.

- Hammack (’26) said the jobs report is 'a bit stale' but is in line with expectations, looked a bit mixed and highlighted challenges faced by monetary policy.

- Paulson (’26) said the higher u/e rate is still in the “neighborhood of full employment” and generally viewed the September data as encouraging.

- 0730ET - NY Fed Williams (voter) keynote speech at Central Bank of Chile conference (text + Q&A)

- 0800ET - Boston Fed’s Collins (’25) on CNBC

- 0830ET - Fed Gov. Barr (voter, most hawkish permanent voter) welcoming remarks

- 0830ET - Fed Gov. Miran (voter, outright dove) on Bloomberg TV. He said after payrolls yesterday that it’s “incumbent upon” the Fed to move rates closer to neutral.

- 0845ET - Fed Gov. Jefferson (voter) on financial stability (text + Q&A)

- 0900ET - Dallas Fed’s Logan (’26, hawk) in SNB panel (text + Q&A)

SOFR: Mix Of Net Long Setting & Short Cover Seen Thursday

OI data points to net long setting dominating in the SOFR white, green and blue packs on Thursday, while net short cover was more prominent in the reds as most contracts settled higher.

| 20-Nov-25 | 19-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,401,556 | 1,386,121 | +15,435 | Whites | +59,422 |

SFRZ5 | 1,484,002 | 1,440,702 | +43,300 | Reds | -14,342 |

SFRH6 | 1,351,448 | 1,343,824 | +7,624 | Greens | +17,922 |

SFRM6 | 1,110,590 | 1,117,527 | -6,937 | Blues | +20,028 |

SFRU6 | 1,146,853 | 1,138,785 | +8,068 |

|

|

SFRZ6 | 1,158,559 | 1,167,004 | -8,445 |

|

|

SFRH7 | 860,651 | 868,267 | -7,616 |

|

|

SFRM7 | 794,356 | 800,705 | -6,349 |

|

|

SFRU7 | 845,673 | 819,957 | +25,716 |

|

|

SFRZ7 | 819,177 | 823,092 | -3,915 |

|

|

SFRH8 | 454,320 | 452,630 | +1,690 |

|

|

SFRM8 | 395,558 | 401,127 | -5,569 |

|

|

SFRU8 | 357,992 | 345,025 | +12,967 |

|

|

SFRZ8 | 333,744 | 324,355 | +9,389 |

|

|

SFRH9 | 192,485 | 195,637 | -3,152 |

|

|

SFRM9 | 187,877 | 187,053 | +824 |

|

|

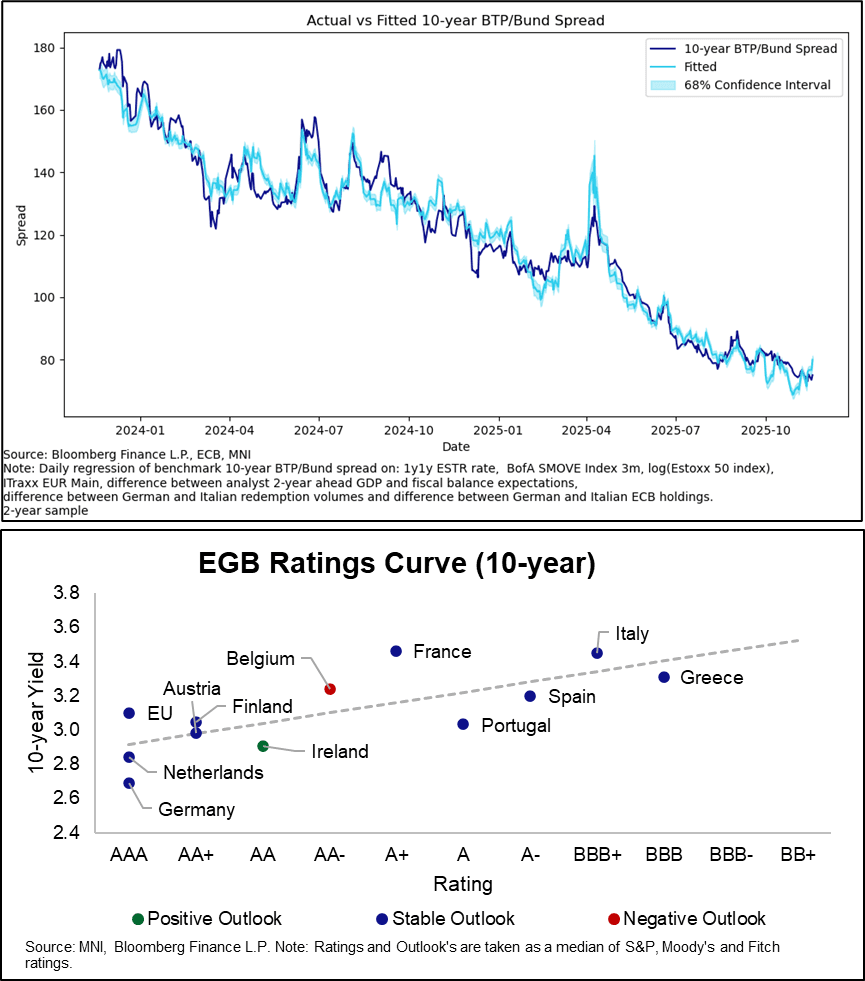

ITALY: One Notch Upgrade From Moody's Expected After Hours; Already In The Price

Moody's is scheduled to review Italy's sovereign rating after hours (current rating Baa3; Outlook Positive). We lean in favour of a one-notch upgrade, but believe this is already in the price for BTPs. A BTP-positive risk would be a one-notch upgrade to Baa2 and a maintained Positive Outlook, but this is not our base case.

- Moody's moved Italy to "Positive" in May, and have since noted that the draft budget for 2026 reflects fiscal discipline and is a "credit positive".

- Even with a one-notch upgrade, Moody's rating will still be below that of S&P and Fitch (both BBB+). This suggests there may be scope for further positive ratings action next year, but we await Moody's write-up of conditions for further upgrades before making such an assumption.

- At the end of October, Scope upgraded Italy's outlook to Positive (rating affirmed at BBB+), but noted that "the main credit challenges reflect i) high government debt and funding needs,...ii) weak longer-run economic growth performance; and iii) an ageing and declining working-age population weighing on productivity and fiscal sustainability". The still-high debt/GDP ratio was also noted as a potential ratings hindrance by Director General of the Treasury Barbieri last week.

- The 10-year BTP/Bund spread is currently at 76bps, with upward pressure intraday stemming from a renewed pullback in global risk sentiment. A linear model that captures ECB pricing, risk/vol proxies and fiscal/issuance fundamentals points to a fair value of ~78bps, so not far from current levels. On the other hand, we note that BTPs screen as slightly cheap on a simple ratings vs 10-year yield chart.

RUSSIA: Kremlin: No Official Talks On 28 Point Plan, Putin To Chair NSC Today

Kremlin spox Dmitry Peskov, when asked if Russia had taken part in talks with the US on the mooted 28-point Ukraine peace plan, says, "No, we haven't received anything officially. We're seeing some innovations. But we haven't received anything officially. And there hasn't been any substantive discussion of these points,". Says that "Our contacts [between Russia and the United States] are not ceasing, and we have never stopped them,". Appears to be little credence to Peskov's claims, with US presidential envoy Steve Witkoff's apparently accidental reply on X implicating 'K' in the initial story on the plan, seemingly implicating Russian presidential envoy Kirill Dmitriev.

- Says the Russia and US "are not discussing the US proposals yet in detail", but that "Russia remains open to negotiations". Peskov says that Ukrainian President Volodymyr Zelenskyy's room for manoeuvre is "shrinking due to Russian battlefield progress", and that Zelenskyy must make a "responsible decision" and do it now.

- Peskov says he has no idea what rumours of a 27 November peace deal signing are based on, but that Russia wants the talks to be successful, "which is why it does not want to publicly discuss proposals".

- Confirms that President Vladimir Putin will hold a meeting with the permanent members of the National Security Council later today, with the topic to be determined by Putin. Comes as reports claim Russia will call up military reservists to guard key oil and gas infrastructure amid a spate of Ukrainian drone strikes.

- Peskov: "A meeting [of Putin and Trump] is certainly necessary and important. But it will be preceded by a great deal of homework at the expert level,"

FOREX: USD Supported by Risk Off Sentiment, JPY Outperforming

- An extension of equity weakness early Friday is providing support to the US dollar, as the DXY edges higher towards the recovery highs at 100.36. Ongoing concerns relating to AI valuations continue to permeate global markets, and waning sentiment across crypto markets and pressure on precious metals appear to finally be providing headwinds for Cross/JPY and pressuring the EM FX basket.

- JPY is the outperformer this morning, leading USDJPY to reverse around 120 pips from yesterday’s 157.89 cycle high. Overnight inline Japanese core CPI print likely did not move the needle for the December BoJ decision as opposed to recent price action in the yen. Some profit taking dynamics may be at play heading into the weekend, and there is the potential for verbal jawboning from Japanese authorities to pick up next week.

- This week’s rally fell short of the year’s highs at 158.87, however, it is worth noting the pair has entered overbought territory, and the latest dip is seen as corrective. The prior breakout at 155 now provides initial support.

- The most notable implication of this morning's Flash PMIs perhaps were parts of the UK press release which should facilitate BoE Governor Bailey's confidence to cut in December. GBPUSD has seen some downside in recent trade, hovering just above 1.3050, and a reversal through 1.3010, the Nov 4 / 5 low, would confirm a resumption of the downtrend. Focus for GBP is on Wednesday's UK budget.

- Michigan consumer sentiment and inflation expectations alongside US wholesale sales and Canada retail sales are on the data calendar for today. A set of speakers from the ECB, the BoE, the SNB and Fed are scheduled to appear.

OPTIONS: Expiries for Nov21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E1.7bln), $1.1535(E1.3bln), $1.1575(E669mln), $1.1625(E932mln), $1.1675-80(E1.2bln)

- USD/JPY: Y155.00($933mln), Y156.00($881mln)

- AUD/USD: $0.6550(A$2.3bln)

- USD/CAD: C$1.3950-70($1.3bln), C$1.4000($600mln)

EQUITIES: Eurostoxx 50 Futures Below Key Support at 50-Day EMA

- A medium-term bull trend in Eurostoxx 50 futures remains intact, however, the past week’s sell-off highlights a stronger corrective cycle. The contract has breached two key support points; 5600.89, the 50-day EMA, and 5621.00, the base of a bull channel drawn from the Aug 1 low. The breach signals scope for a deeper pullback and opens 5427.01, a Fibonacci retracement. Initial firm resistance to watch is 5645.61, the 20-day EMA.

- S&P E-Minis remain in a short-term bear-mode condition and a steep sell-off yesterday reinforces current conditions. The breach of 6655.70, the Nov 7 low cancels recent bullish signals and signals scope for an extension of the corrective cycle. Sights are on 6540.25 (pierced), the Oct 10 low and a key support. A break would open 6476.62, a Fibonacci retracement point. Initial firm resistance to watch is 6747.78, the 20-day EMA.

COMMODITIES: Move Down in WTI Futures This Week Strengthens a Bearish Theme

- The move down this week in WTI futures strengthens a bearish theme. A stronger resumption of the bear leg would pave the way for a move towards key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $61.84, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction.

- The bearish phase in Gold between Oct 20 and 28 appears to have been a correction and has allowed a recent overbought condition to unwind. The recovery since Oct 28 does suggest the correction is over. Key support to watch lies at the 50-day EMA, at $3948.2. Clearance of this EMA would signal scope for a deeper retracement. The first short-term bull trigger has been defined at $4245.23, the Nov 13 high.

| Date | GMT/Local | Impact | Country | Event |

| 21/11/2025 | 1230/0730 | New York Fed's John Williams | ||

| 21/11/2025 | 1330/0830 | ** | Retail Trade | |

| 21/11/2025 | 1330/0830 | Fed Governor Michael Barr | ||

| 21/11/2025 | 1345/0845 | Fed Vice Chair Philip Jefferson | ||

| 21/11/2025 | 1400/0900 | Dallas Fed's Lorie Logan | ||

| 21/11/2025 | 1400/0900 | Boston Fed's Susan Collins | ||

| 21/11/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/11/2025 | 1445/0945 | *** | S&P Global Services Index (flash) | |

| 21/11/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 21/11/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 21/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 21/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 21/11/2025 | 1540/1540 | BOE Pill in Panel at Swiss National Bank | ||

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 21/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 22/11/2025 | 0800/0900 | ECB Lagarde in Roundtable at Austrian National Bank | ||

| 22/11/2025 | 1100/1200 | ECB Lagarde Keynote on Fiscal and MonPol |