MNI EUROPEAN OPEN: USD/JPY Testing Sub 150.00

EXECUTIVE SUMMARY

- TRUMP SAYS PUTIN WAR SUMMIT WILL HAPPEN IN ‘TWO WEEKS OR SO’ - BBG

- FED’S KASHKARI: INFLATION LINGERING, JOBS WEAKENING - MNI BRIEF

- BOJ IS LOOKING FOR SIGNS OF SLOWING INFLATION - MNI POLICY

- CHINA ANALYSTS SHARE THEIR Q3 GDP OUTLOOK - MNI

- ECONOMISTS & FORMER STAFFERS SHARE THEIR RBA CASH RATE OUTLOOK - MNI

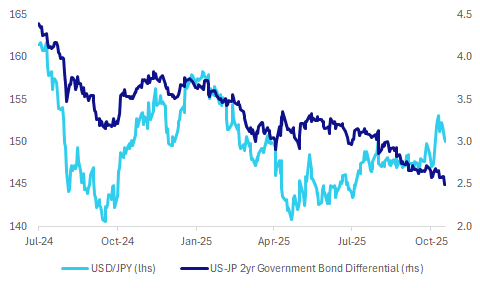

Fig 1: USD/JPY& US-JP Yields Differentials

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

BOE (MNI BRIEF): Domestic factors are driving headline UK inflation higher and elevated food inflation is pushing inflation expectations above levels consistent with the Bank of England's target, Catherine Mann, Bank of England Monetary Policy Committee said at a Washington event.

INVESTMENT (MNI BRIEF): Chancellor of the Exchequer Rachel Reeves announced a new fully operational Office for Investment: Financial Services on Thursday.

GEOPOLITICS (BBG): “Reform UK leader Nigel Farage criticized Vladimir Putin as irrational and backed shooting down Russian jets that enter NATO airspace, following criticism that his views on Moscow could threaten his bid to become prime minister.”

EU

RUSSIA (BBG): “US President Donald Trump said he would hold a second meeting with Russian President Vladimir Putin “within two weeks or so” aimed at ending the war in Ukraine.”

ECB (BBG): “ The European Central Bank mustn’t rush further interest-rate action, also because the effects of higher US trade levies on prices aren’t yet clear, Governing Council member Edward Scicluna said.”

TARIFFS (BBG): “President Donald Trump announced a deal with Germany’s Merck KGaA to cut the price of its fertility medicines in exchange for relief from threatened tariffs, a step toward fulfilling his campaign promise of making IVF less expensive and more widely available in the US.”

US

FED (MNI BRIEF): It's too soon to tell whether tariffs will have a persistent effect on inflation while demand for workers is weakening, Minneapolis Federal Reserve Bank President Neel Kashkari said Thursday.

FISCAL (MNI BRIEF): The United States federal budget deficit totaled USD1.775 trillion in fiscal year 2025, 2% lower than last year’s deficit of USD1.817 trillion, the Treasury Department said Thursday, estimating the deficit-to-GDP eased from 6.3% in 2024 to 5.9% in 2025 on a growing economy.

TARIFFS (BBG): “The White House is poised to ease tariffs on the US auto industry, a move that would deliver a major win for carmakers that have aggressively lobbied to stem the fallout from record-level import duties.”

OTHER

CANADA (MNI BRIEF): Bank of Canada Governor Tiff Macklem said Thursday he will move policy carefully as the extent of damage from the U.S. trade war remains unclear, adding economic growth will be "soft" in the second half of this year.

JAPAN (MNI POLICY): The BOJ is looking for signs of slowing inflation amid sluggish private consumption. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

JAPAN (RTRS): "Japan's lower house scheduling committee board has agreed to hold a parliamentary vote to select the next prime minister on October 21, a senior committee member told Reuters on Friday."

AUSTRALIA (MNI): Economists and former staffers share their RBA cash rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

CHINA

GDP (MNI): Chinese analysts and advisors share their Q3 GDP outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

US/CHINA (BBG): " China’s Commerce Minister Wang Wentao on Thursday blamed the recent escalation in trade tensions with the US on American actions following the latest bilateral round of talks, in Madrid last month."

DEPOSTITS (YICAI): "China's slowdown in deposit relocation towards the capital markets in September may be related to the weakening wealth effect caused by stock indices fluctuating at high levels, analysts told Yicai."

MNI: PBOC Net Drains CNY244.2 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY164.8 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY244.2 billion after offsetting maturities of CNY409 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4023% at 10:09 am local time from the close of 1.4225% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Thursday, compared with the close of 48 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.0949 Fri; -0.16% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0949 on Friday, compared with 7.0968 set on Thursday. The fixing was estimated at 7.1196 by Bloomberg survey today.

MARKET DATA

SOUTH KOREA SEP EXPORT PRICE Y/Y 2.2%; PRIOR -1.1%

SOUTH KOREA SEP IMPORT PRICE Y/Y 0.6%; PRIOR -2.2%

SOUTH KOREA SEP UNEMPLOYMENT RATE 2.5%; MEDIAN 2.6%; PRIOR 2.6%.

MARKETS

US TSYS: Yields Lower, 10-Yr Resetting Recent Ranges

- UST's strength overnight followed through into the Asia trading day with TYZ5 up +06 at 113-30+ after touching near term highs overnight. The NIKKEI is down as other regional bourses start their trading day, watching to see if the lead in from the US follows through.

- US 2-Yr is down further at 3.40% (-2bps today)

- US 5-Yr is at 3.52% (-2.5bps)

- US 10-yr is consolidating below 4.00% with a further rally to 3.94%. The key will be whether it can hold below 4% overnight and reset recent trading ranges.

- US 30-yr is down -1bps at 4.55% and is back to levels of April due the peak of the trade war volatility.

- Data out tonight include housing starts and Import and Export price index.

- The rally in bonds overnight is being attributed to regional bank fears with two banks reported exposure to the sub prime lender Tricolor Holdings which has collapsed. Looking at the current discussions on exposures to the balance sheets of these banks it appears manageable and the market will watch closely tonight for further details.

JGBS: Holding Richer Despite BOJ Words, BoJ Uchida Speech Due

JGB futures are sharply stronger, +43 compared to settlement levels.

- (MNI Policy) Bank of Japan officials are watching for signs that some businesses are struggling to pass on cost pressures to selling prices as consumer spending lacks momentum amid persistent high prices and negative real wages, a development that could further complicate the central bank’s efforts to normalise policy smoothly, MNI understands.

- (Bloomberg) “Bank of Japan Governor Kazuo Ueda indicated that the bank will continue tightening if confidence in achieving its economic outlook strengthens — keeping the door open for a near-term interest-rate hike.

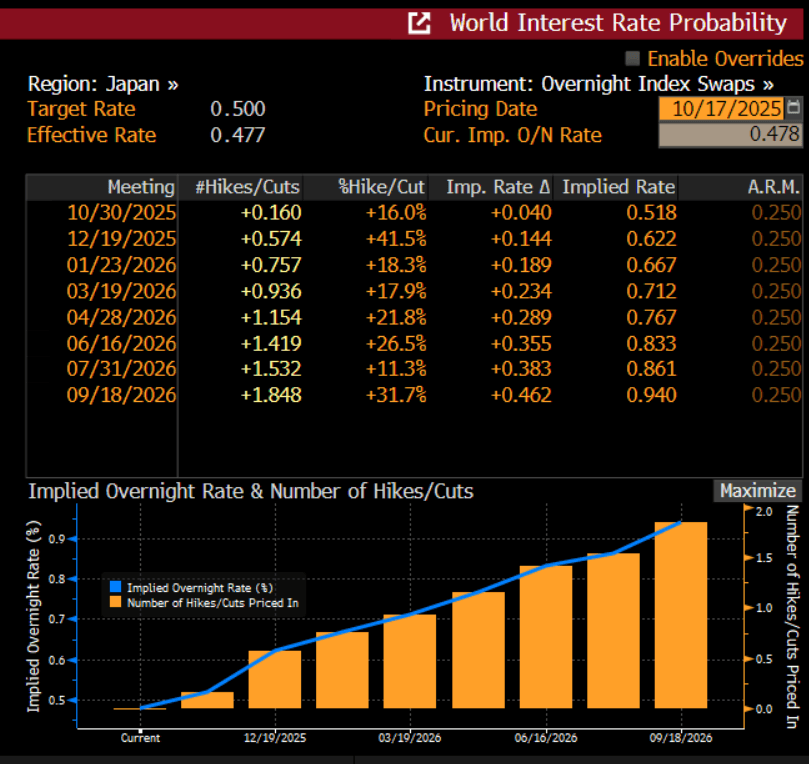

- Markets doubt the BOJ will raise its 0.5% policy rate at the Oct. 30 meeting, pricing in a 42% chance of a hike at the Dec. 19 session, with a 0.75% rate not fully expected until at least April. (see chart)

- Cash US tsys are 3-4bps richer in today’s Asia-Pac session after yesterday’s solid gains.

- Cash JGBs are 1-4bps richer across benchmarks, with the futures linked 7-year leading.

- 2/30 yield curve is closing in on near support around 220bps.

- Swap rates are 1-3bps lower.

- On Monday, the local calendar will be empty apart from a speech from BOJ Board Takata. Speech by BOJ Deputy Governor Uchida is due later today.

Bloomberg Finance LP

AUSSIE BONDS: Sharply Stronger As Post-Jobs Rally Extends

ACGBs (YM +8.5 & XM +6.5) are richer and at session highs. Today's move currently leaves futures 11-16bps stronger than yesterday's pre-jobs data levels, with the YMXM curve 5bps steeper. However, the curve remains near its flattest point since April, having broken out of a well-defined range earlier in the year.

- Cash US tsys are 3-4bps richer in today's Asia-Pac session after yesterday’s solid gains.

- Cash ACGBs are 6-8bps richer with the AU-US 10-year yield differential at +15bps.

- The bills strip has bull-flattened, with pricing +4 to +9.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in November is given an 80% probability, with a cumulative 28bps of easing priced by year-end.

- Interest rate expectations across the $-bloc have softened over the past week, led by Australia (-15bps) and the US (-9bps), with New Zealand (-3bps) and Canada (-2bps) lagging.

- The local data calendar is fairly quiet through the course of the next week, with Oct preliminary PMIs out next Friday, with the RBA's Bullock also speaking that day.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$900mn of the 2.75% 21 June 2035 bond on Wednesday and A$800mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Rally Extends But Lags $-Bloc, Q3 CPI On Monday

NZGBs closed showing a bull-flattener, with benchmark yields 3-5bps lower, on a data-light session.

- On a relative basis, NZGBs lagged the $-bloc, with the NZ-US and NZ-AU 10-year yield differentials 4bps and 2bps wider, respectively.

- Nevertheless, the NZ-US differential is holding around levels last seen in February.

- Swap rates closed 4-6bps richer with the 5-year leading.

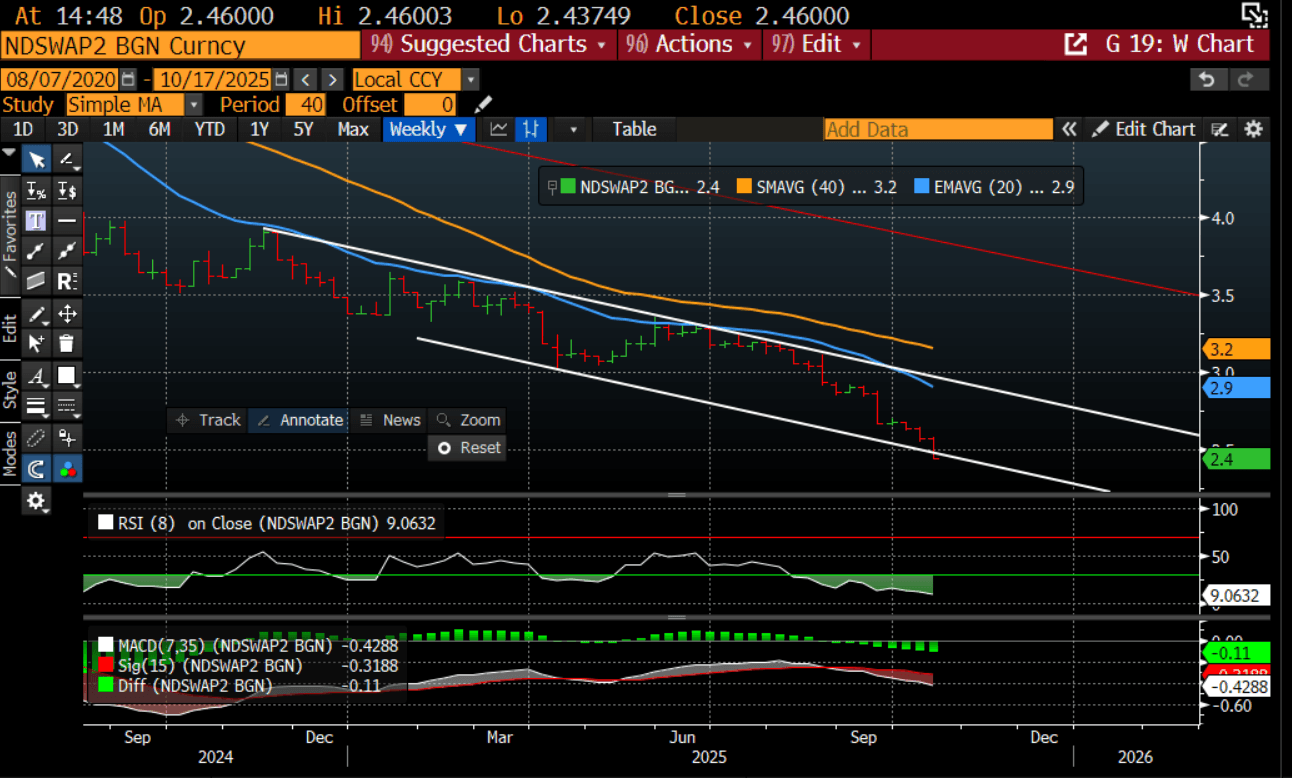

- For context, the 2-year swap rate is around 40bps lower than levels seen before the release of Q2 GDP data in late September, which dramatically undershot expectations. (see chart)

- RBNZ-dated OIS pricing is little changed across meetings. 26bps of easing is priced for November, with a cumulative 36bps by February 2026.

- On Monday, the local calendar will see Q3 CPI, with BNZ expecting the CPI to fall from its Q3 peak at 3%, as the current bout of inflation gradually unwinds. Monthly prices, released yesterday, edged slightly lower compared to prior months, indicating a softer trend and a lower base heading into the fourth quarter. - MTN

Bloomberg Finance LP

ASIA STOCKS: Equities Down from Overnight Leads, CSI 300 Testing Key Levels

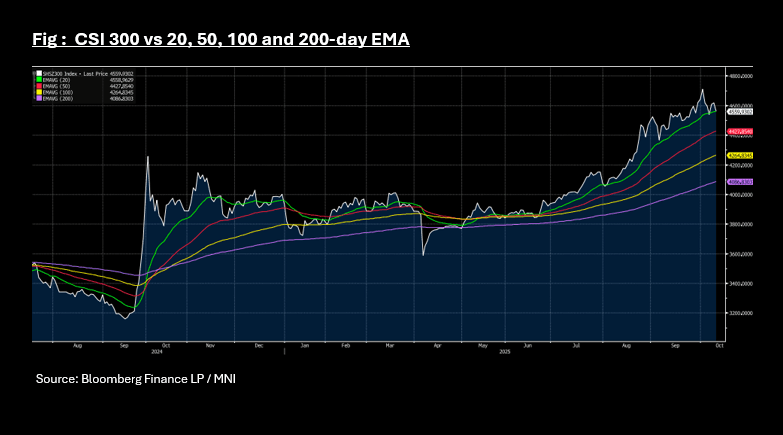

- The overnight lead from the US followed over into major bourses in Asia today, with China and Hong Kong down. Earlier in the week the HSI tested the 50-day EMA support but with the overnight headwinds traded through it has stabilized at the mid-point between the 50 and 100-day EMA. The CSI 300 is down -1.2% and is near the 20-day EMA which it has struggled to hold below since April. An article on BBG suggests that data shows China's households may be stepping back from equities, with cash holdings spiking in September - challenging the last few weeks of positive momentum.

- The NIKKEI is down -1.20% unable to gain further momentum back towards last week's new all time high and could be set to finish down for the week.

- The KOSPI has also reached new highs again and hovering around unchanged on the day, as it outperforms regional peers.

- In Taiwan, the strength of the TSMC results overnight and the accompanying outlook was not enough to see the TAIEX rally, falling by -0.6% today in a subdued day of trading.

- In India, there is renewed hope for trade discussions with the US with the NIFTY 50 holding onto modest gains this morning, looking at a second successive weeks of gains.

FOREX: USD Falters On Further Yields Losses, USD/JPY Tests Under 150, A$ Lower

USD indices continue to tick lower, the BBDXY off a further 0.10% to 1206.5/6 (fresh lows since Oct 7). US Tsy yields have dropped further, amid a continuation of the risk off mood. JPY (testing under 150.00) and CHF (near 0.7900) are the outperformers, particularly against the higher beta AUD. A$ losses have been compounded by China/HK equity market weakness.

- USD/JPY got to lows of 149.90 a short while ago, so sub the 20-day EMA, before stabilizing. The 50-day is further south at near 148.75/80. Risk tones are dictating yen shifts. US equity futures are down a further 0.40% so far today, with eyes on whether the 50-day EMA support zone will be tested. Credit jitters related financial/bank equity sentiment on Thursday. Risk tones are also driving demand for Tsys, with yields down a further 3bps (10yr to 3.94%).

- USD/JPY already looked too elevated relative to US-JP rate differentials, with today's moves reinforcing these trends.

- The Japan PM vote is scheduled to go ahead on Oct 21. It remains to be seen if there will be a Ishin/LDP coalition (with agreement potentially not coming until early next week). An Ishin co-leader stated earlier coalition chances were 50/50.

- AUD/USD remains in a downtrend, although is still above recent lows of 0.6440 (last 0.6470). This week's jobs data has bought RBA cuts back into focus, which is likely driving some fresh A$ and cross selling, particularly given broader risk off. AUD/JPY got to 96.89 earlier, around earlier Oct lows and we are under the 50-day EMA support (97.46).

- NZD/USD has been relatively steady, last near 0.5730, lagging yen and CHF gains. AUD/NZD is back under 1.1300 with focus on next Monday's Q3 CPI print in NZ.

- Looking ahead it is fairly quiet data wise, but we do have BOE, ECB and Fed (before the blackout period) speak to round out the week.

Oil Falls for Third Week on US China Standoff

- Oil prices continued to fall today and is set for a third successive weekly fall.

- WTI is approaching being oversold after US China trade tensions challenge global growth assumptions, and news of the potential Trump / Putin meeting challenge assumptions on Russian supply.

- This comes as OPEC+ has ramped up production, agreeing to successive increases.

- WTI is down -2.7% at US$57.31 bbl week to date and on the 14-day Relative Strength Index, nears being oversold.

- Similarly Brent is down -2.9% this week and down 13% over the last three weeks.

- EU Commission has published updated guidelines on the documentation, due diligence required for complying with the import ban on refined products that have been processed from Russian crude oil, according to its website. The guidelines set out how importers should exercise due diligence when importing fuels to ensure it has not come from Russian crude (as per BBG).

- This comes as India's refiners have stated that they intend to reduce (but not stop) the purchase of Russian oil, as per comments from India's biggest refiners.

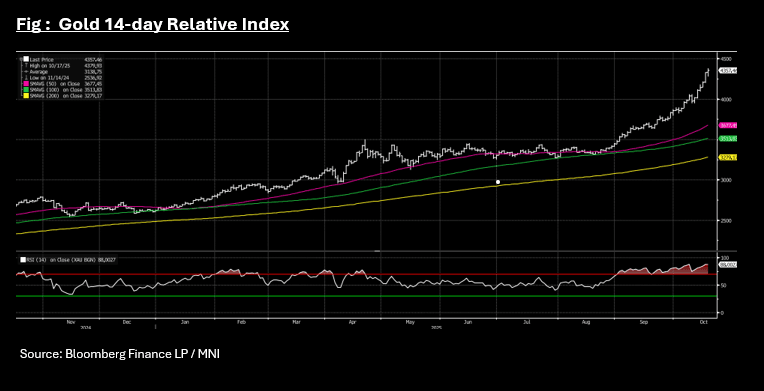

Gold Set for Biggest Weekly Gain of Year

- The relentless rally for gold continued today as new all time highs were reached yet again.

- A rally +0.70% today to US$4,356 sees the precious metal up over 8% for the week.

- Markets turned weaker overnight as credit fears reared over two regional banks in the US. This came following the collapse of a sub-prime lender with two regional banks share prices falling heavily given fears of exposure to the lender.

- That environment is ideal for gold and prices were strong in regional trade today.

- Gold is up over 12% in October alone and over 60% this year and remaining overbought on the relative strength index for a second month.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 17/10/2025 | 0600/0800 | ** | Unemployment | |

| 17/10/2025 | 0900/1100 | *** | EZ HICP Final | |

| 17/10/2025 | 0935/1035 | BOE Pill Speech at Institute of Chartered Accountants Conference | ||

| 17/10/2025 | 1100/1200 | BOE Greene Roundtable at Atlantic Council | ||

| 17/10/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/10/2025 | 1230/0830 | *** | Housing Starts | |

| 17/10/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/10/2025 | 1230/0830 | *** | Housing Starts | |

| 17/10/2025 | 1315/0915 | *** | Industrial Production | |

| 17/10/2025 | 1615/1215 | St. Louis Fed's Alberto Musalem | ||

| 17/10/2025 | 1630/1730 | BOE Breeden in Panel at IMF/World Bank Meetings | ||

| 17/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/10/2025 | 2000/1600 | ** | TICS | |

| 18/10/2025 | 1130/1330 | ECB Cipollone Speech at Euro50Group Meeting | ||

| 18/10/2025 | 1300/1500 | ECB Lagarde in Economic Outlook Panel at G30 | ||

| 18/10/2025 | 1300/1400 | BOE Bailey at G30 International Banking Seminar |