AUSSIE BONDS: Sharply Stronger As Post-Jobs Rally Extends

ACGBs (YM +8.5 & XM +6.5) are richer and at session highs. Today's move currently leaves futures 11-16bps stronger than yesterday's pre-jobs data levels, with the YMXM curve 5bps steeper. However, the curve remains near its flattest point since April, having broken out of a well-defined range earlier in the year.

- Cash US tsys are 3-4bps richer in today's Asia-Pac session after yesterday’s solid gains.

- Cash ACGBs are 6-8bps richer with the AU-US 10-year yield differential at +15bps.

- The bills strip has bull-flattened, with pricing +4 to +9.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in November is given an 80% probability, with a cumulative 28bps of easing priced by year-end.

- Interest rate expectations across the $-bloc have softened over the past week, led by Australia (-15bps) and the US (-9bps), with New Zealand (-3bps) and Canada (-2bps) lagging.

- The local data calendar is fairly quiet through the course of the next week, with Oct preliminary PMIs out next Friday, with the RBA's Bullock also speaking that day.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$900mn of the 2.75% 21 June 2035 bond on Wednesday and A$800mn of the 2.75% 21 November 2029 bond on Friday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

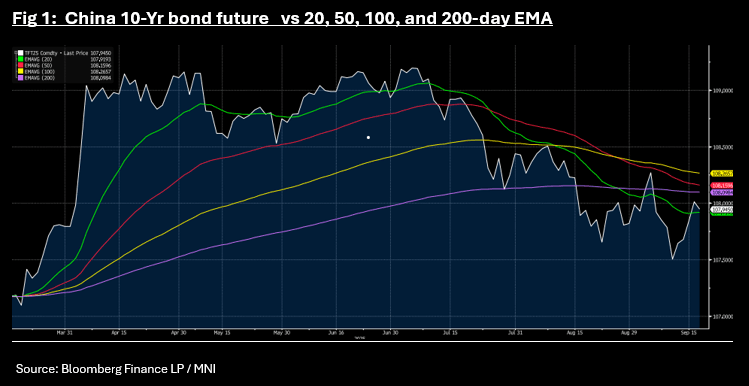

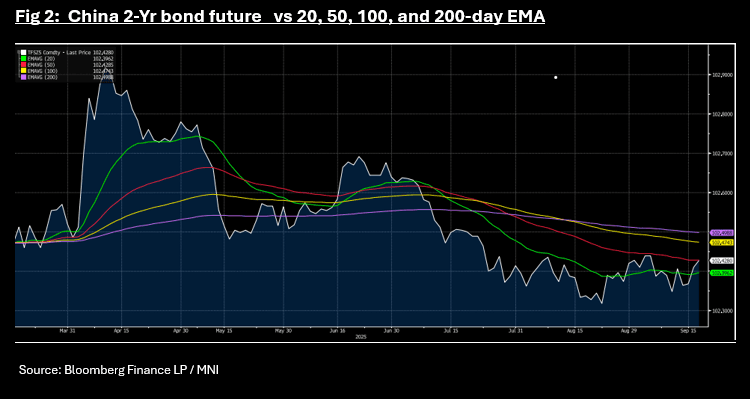

CHINA: Bond Futures Approach Key Technical Levels

- China's bond futures are mixed today with the 10-Yr down and the 2-Yr marginally up.

- The 10-Yr is down -0.06 at 107.94. Having traded through the 20-day EMA, the decline today sees it again approach the 20-day of 107.91.

- China's 2-Yr bond future is up +0.01 at 102.42 and is near to the 50-day EMA , which it has not traded through since early July.

- China's 10-Yr CGB is at 1.78% .

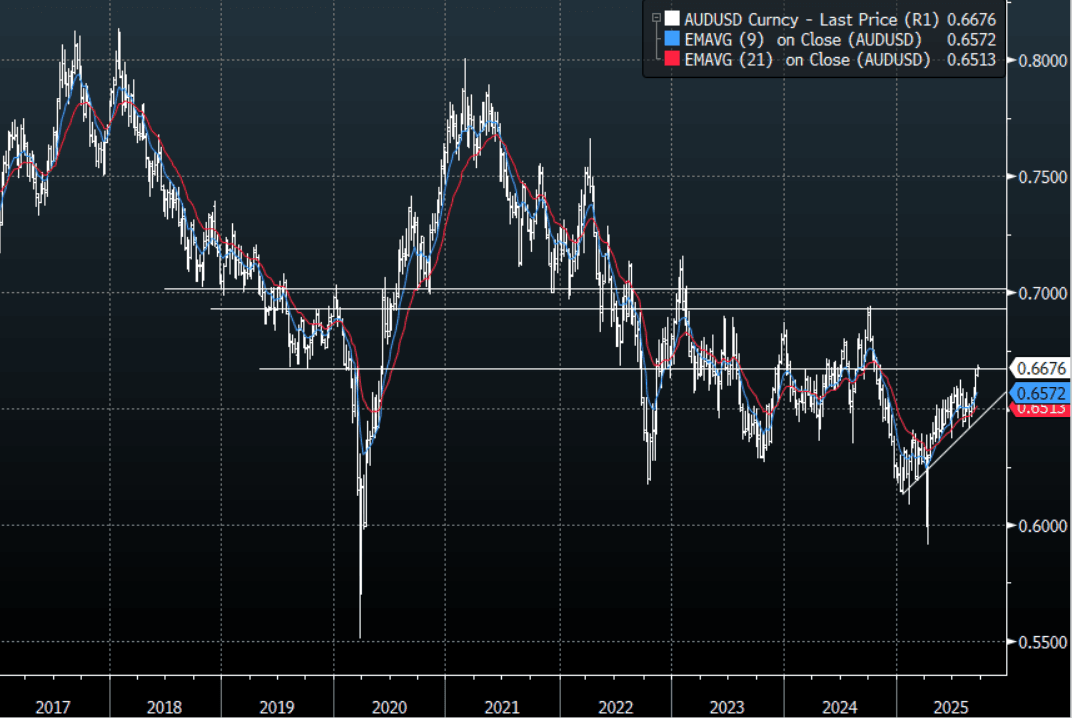

AUD: Asia Wrap - AUD/USD Pressing Resistance Heading Into FOMC

The AUD/USD has had a range of 0.6672 - 0.6690 in the Asia- Pac session, it is currently trading around 0.6675, -0.15%. US stocks finally paused for a breath ahead of the FOMC, but the USD can’t catch a break and looks to be breaking lower even before the market hears from Powell. The AUD continues to be supported and grinds higher. How the USD reacts after the FOMC will be key as the market has already priced in some significant negativity. If the USD can follow through with this move then we could see the AUD gain momentum above 0.6650/0.6700 and potentially target levels back towards 0.6900/0.7000. The price action suggests dips will be supported for now as we await confirmation of this potential break higher, the first buy-zone is back towards the 0.6550 area.

- MNI AU: Unchanged Unemployment Rate Expected On Thursday, Analysts Split. August labour market data are released on Thursday and remain a point of focus. Employment is forecast to rise 21k after July’s +24.5k with the unemployment rate expected to remain at 4.2%. It will also be important to monitor underemployment, the split between full-time & part-time and hours worked. The RBA is currently expected to leave rates unchanged on September 30 as it waits for Q3 CPI on October 29.

- MNI - Westpac Lead Indicator Signals Slower Growth: Westpac’s lead index signalled slowing growth in August with the 6-month annualised rate turning negative (-0.16% down from July’s +0.11%) for the first time since September 2024. Almost all variables have eased over the last 6 months. It is signalling that growth on a 2q/2q basis could slow over the coming quarters.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD457m). Upcoming Close Strikes : 0.6600(AUD894m Sept 18), 0.6750(AUD1.16b Sept 19) - BBG

- AUD/JPY - Asia-Pac range 97.79 - 97.96, Asia is trading around 97.80. The pair’s move higher has finally stalled towards 98.50. Dips back towards 96.50/97.00 should be expected to be supported now first up.

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

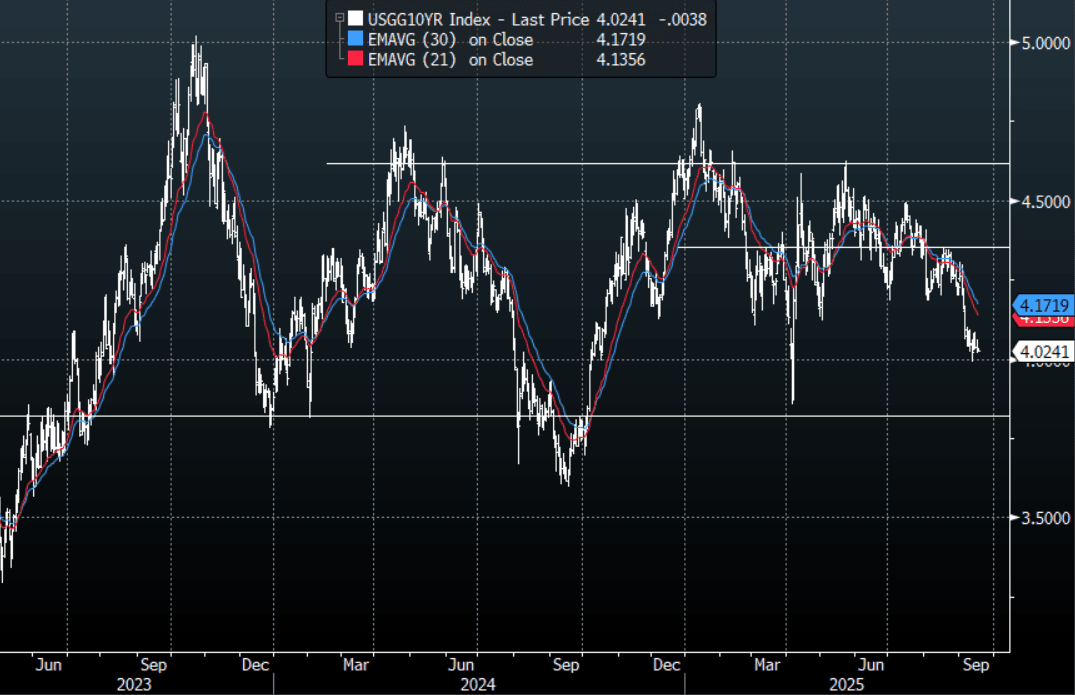

US TSYS: Quiet Session, Looking Toward FOMC

The TYZ5 range has been 113-15 to 113-18+ during the Asia-Pacific session. It last changed hands at 113-17+, down 0-00+ from the previous close.

- The US 2-year yield is trading 3.503%.

- The US 10-year yield has edged lower trading around 4.022%, down 0.01 from its close.

- 10-Year Yields continue to do work just above 4.00% as the market looks towards the FOMC tomorrow morning. The first buy-zone is now back towards the 4.20% area where I suspect decent demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area. The market does seem confident and is pricing in a dovish outcome, the risk is Powell does not deliver.

- Luke Gromen on X: “The weaker the USD gets, the better the LT UST auctions get. It is taking a bit more USD downside to get good auctions than it used to, it seems. Where things get more interesting is when the lagged impact of the weaker USD begins to show up in inflation readings. Let's watch.”

- Nick Timiraos on X: “The Fed is expected to cut rates by 25 bps on Wednesday, with all eyes on how many officials pencil in three cuts for the year, implying consecutive cuts in October and December. A walkup to an FOMC meeting unlike any in recent memory.”

- Data/Events: MBA Mortgage Applications, Housing Starts, FOMC Rate Decision

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P