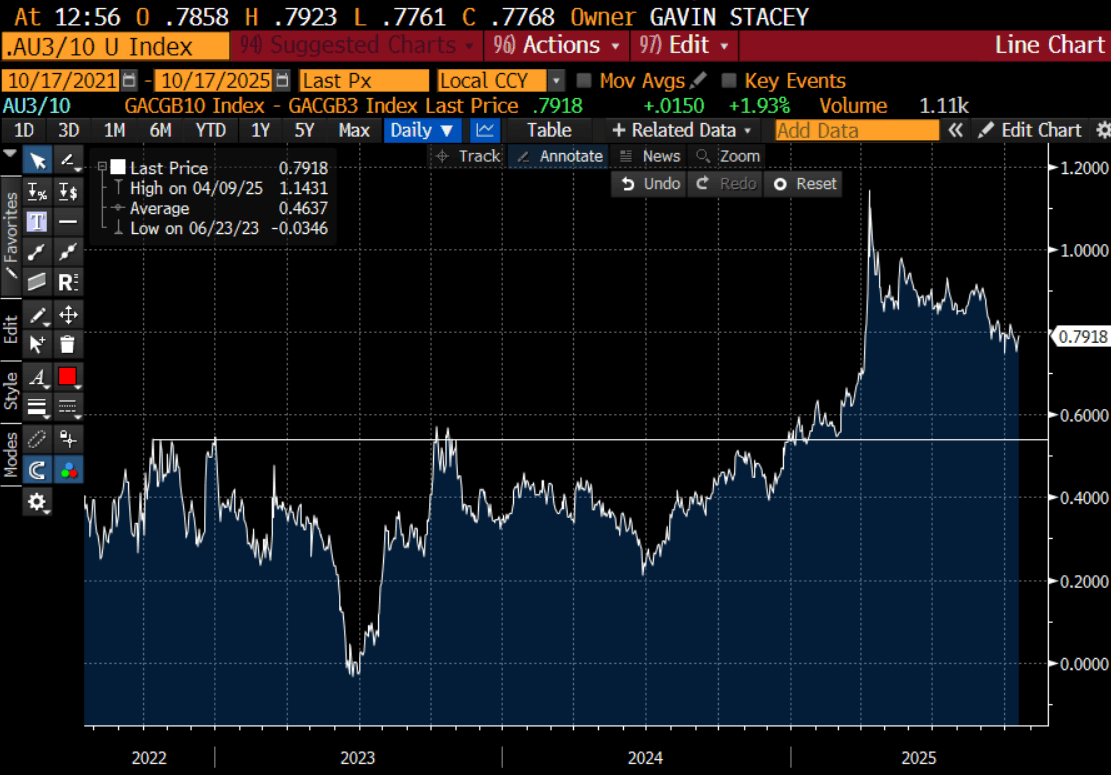

AUSSIE BONDS: Extends Post-Jobs Gains, Curve Steeper After An Extende Flattening

ACGBs (YM +6.0 & XM +4.0) are richer and at session highs. Today’s move currently leaves futures 10-14bps stronger than yesterday’s pre-jobs data levels, with the YMXM curve 4bps steeper. However, the curve remains near its flattest point since April, having broken out of a well-defined range earlier in the year (see chart).

- Cash US tsys are 1-2bps richer in today’s Asia-Pac session after solid gains.

- Cash ACGBs are 4-5bps richer with the AU-US 10-year yield differential at +15bps.

- The latest ACGB Dec-30 supply delivered a weighted average yield of 0.46bps through prevailing mids, according to Yieldbroker. However, the cover ratio declined to 2.7625x from 4.2350x, reflecting weaker demand. The weaker demand may have reflected an outright yield that was 10-15bps lower than the previous auction and sat near the lowest level in the past 12 months. Being excluded from both the YM and XM baskets—placing it in a less favoured segment of the yield curve — may also have impacted demand.

- The bills strip has bull-flattened, with pricing +2 to +5.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in November is given a 79% probability, with a cumulative 27bps of easing priced by year-end.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LNG: Gas Prices Higher On Demand Outlook

Natural gas took direction from oil on Tuesday with prices trending higher driven by concerns that geopolitical issues could impact global fossil fuel supplies. European prices rose 0.8% to EUR 32.42, close to the intraday high, after a low of EUR 31.62 early in the session. They are now 2.5% higher this month.

- European gas fell on Monday driven by forecasts for a significant increase in wind-generated power but that is now expected to moderate towards average. Bloomberg reported that 60% of British power yesterday morning was from wind.

- After numerous Ukrainian attacks on Russian oil infrastructure over the weekend, it struck another refinery early in the week. US-EU talks continue on options to reduce the revenue Russia earns from energy exports. Restrictions on companies in India and China involved in oil trade with Russia were delayed by the EU.

- US gas rose 2.4% to $3.117 to be up 4% in September and 6% this week. It has found support from expectations that there will be increased cooling demand in the second half of September as higher temperatures are projected. There are also thoughts now that this warmer weather may mean a delay to the start of heating demand.

- There is also work on a Permian basin pipeline reducing flows, according to EBW AnalyticsGroup.

- Asian LNG demand looks to be picking up as countries take advantage of favourable prices.

JGBS: Slightly Cheaper Ahead Of Today's 20Y Supply

In Tokyo morning trade, JGB futures are slightly weaker, -2 compared to settlement levels.

- Japan headline Aug trade figures were mixed. Exports were -0.1%y/y, against a -2.0% forecast (-2.6% was the July outcome). On the import side, we fell -5.2%y/y, against a -4.1% forecast and -7.4% prior outcome. The trade deficit was -242.5bn, against a -512.6bn forecast, while July's print was -118.4bn. In seasonally adjusted terms the trade deficit was -150.1bn, which was also better than forecast, but sub recent cycle highs for the balance (+166.5bn in Feb).

- Tariff impact was seen, with exports to the US down -13.8%y/y. To the EU exports rose 5.5%y/y, while to China exports were down a modest -0.5%y/y. The trade surplus Japan has with the US narrowed to 324bn. In Feb this year the surplus was at 918.5bn.

- Automobile exports fell 7.9% in August, the fifth consecutive decline following an 11.4% fall in July. Iron and steel exports dropped 14.9%, easing from July's 21.0% fall. Auto exports to the US fell by 28.4%.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s modest rally.

- Cash JGBs are flat to 2bps cheaper across benchmarks. The benchmark 20-year yield is 1.0bp higher at 1.611% ahead of today’s supply.

- Swap rates are ~1bp higher. Swap spreads are mixed.

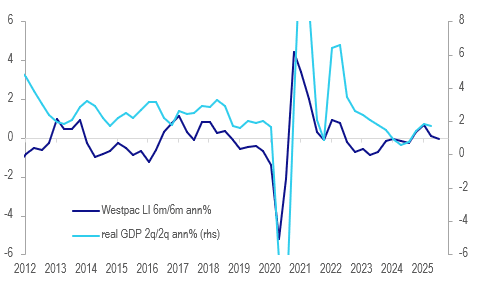

AUSTRALIA DATA: Westpac Lead Indicator Signals Slower Growth

Westpac’s lead index signalled slowing growth in August with the 6-month annualised rate turning negative (-0.16% down from July’s +0.11%) for the first time since September 2024. Almost all variables have eased over the last 6 months. It is signalling that growth on a 2q/2q basis could slow over the coming quarters.

Australia growth outlook %

Source: MNI - Market News/LSEG

- Westpac is forecasting Australian GDP growth of 1.9% in 2025 up from 2024’s 1.3% with it returning to trend next year. Its Card Tracker suggests that private consumption slowed over Q3 to early September. It expects the RBA to be on hold in September but then ease 25bp in November and twice more in 2026.

- Westpac consumer unemployment expectations has been the largest contributor to the moderation in the lead index over the last half year. It rose 4.6% in September’s consumer sentiment survey to the highest in a year and just under the series average. Thus it and confidence (-3.1% m/m Sept) are likely to continue to weigh in the next lead index.

- Commodity prices in AUDs, Westpac consumer sentiment and dwelling approvals also contributed to the moderation. Hours worked, the yield spread and US IP also made slight negative contributions with only Australian equities positive.