JGBS: Holding Richer Despite BOJ Words, BoJ Uchida Speech Due

JGB futures are sharply stronger, +43 compared to settlement levels.

- (MNI Policy) Bank of Japan officials are watching for signs that some businesses are struggling to pass on cost pressures to selling prices as consumer spending lacks momentum amid persistent high prices and negative real wages, a development that could further complicate the central bank’s efforts to normalise policy smoothly, MNI understands.

- (Bloomberg) “Bank of Japan Governor Kazuo Ueda indicated that the bank will continue tightening if confidence in achieving its economic outlook strengthens — keeping the door open for a near-term interest-rate hike.

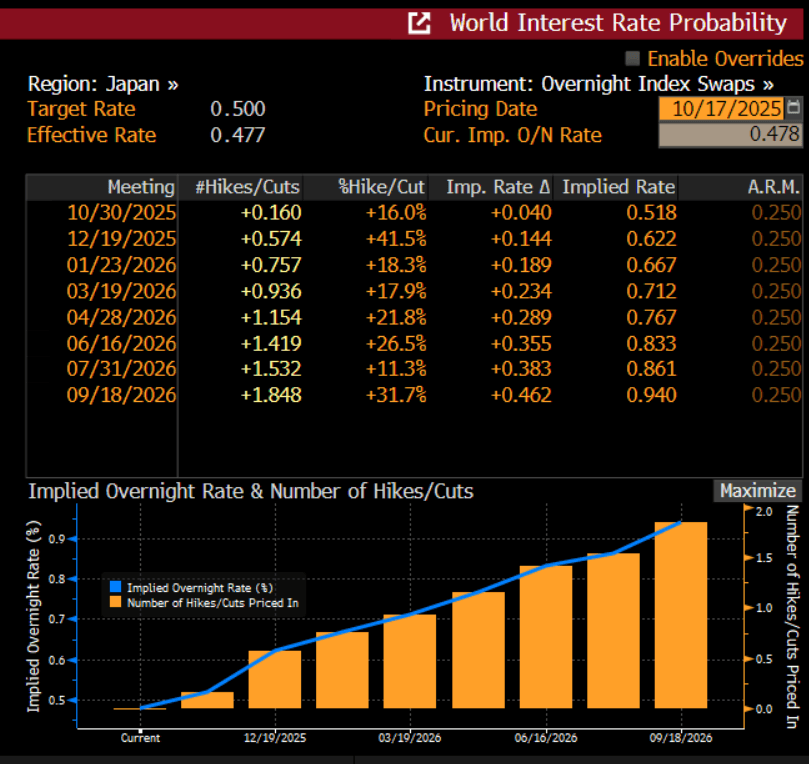

- Markets doubt the BOJ will raise its 0.5% policy rate at the Oct. 30 meeting, pricing in a 42% chance of a hike at the Dec. 19 session, with a 0.75% rate not fully expected until at least April. (see chart)

- Cash US tsys are 3-4bps richer in today’s Asia-Pac session after yesterday’s solid gains.

- Cash JGBs are 1-4bps richer across benchmarks, with the futures linked 7-year leading.

- 2/30 yield curve is closing in on near support around 220bps.

- Swap rates are 1-3bps lower.

- On Monday, the local calendar will be empty apart from a speech from BOJ Board Takata. Speech by BOJ Deputy Governor Uchida is due later today.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Asia FX Wrap - The Market Is Going Into The FOMC Short USD's

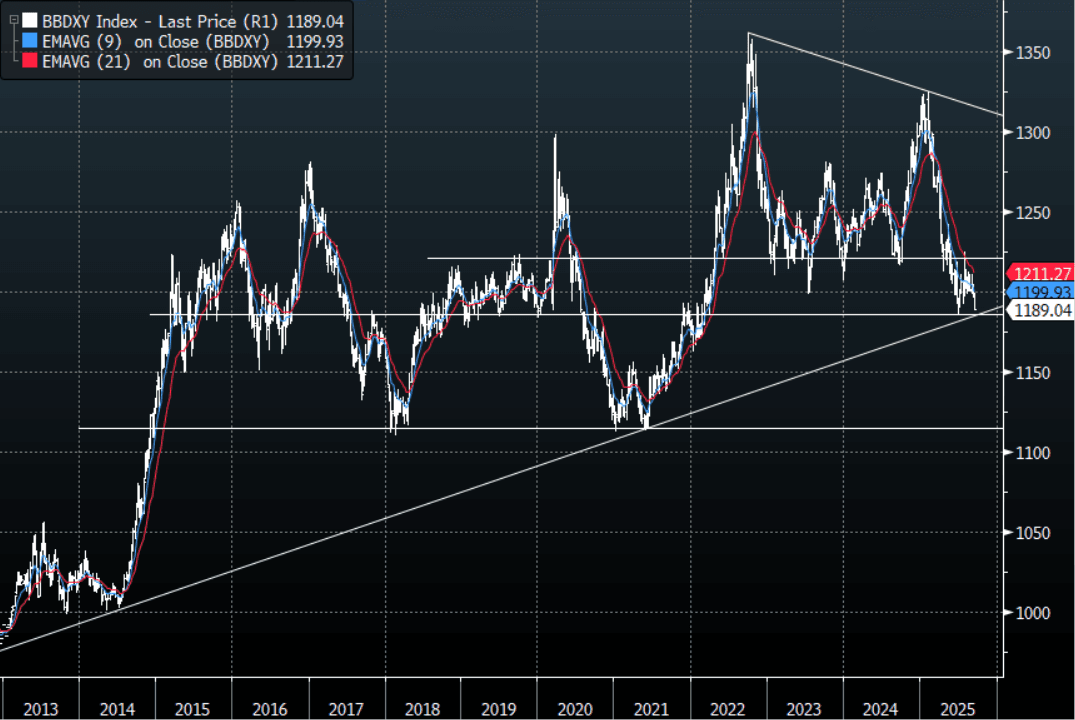

The BBDXY has had a range of 1187.79 - 1189.50 in the Asia-Pac session; it is currently trading around 1189, +0.02%. The USD’s move lower gained pace overnight breaking below its recent support around 1195/97, first target is the year's lows back towards 1180. A sustained break below 1180 would be extremely bearish, should the USD start another leg lower it would have big implications for FX and potentially see a lot of the recent ranges in G10 broken. The market is clearly going into the FOMC short the USD so there is some obvious danger of disappointment, but if the market gets the dovish cut it's looking for the USD could be poised for its next big leg lower.

- EUR/USD - Asian range 1.1851 - 1.1873, Asia is currently trading 1.1855. The pair is making new highs heading into the FOMC as the USD breaks down. Should this break be sustained after the FOMC the first target is 1.2000 then the 1.2200/2300 area.

- GBP/USD - Asian range 1.3639 - 1.3659, Asia is currently dealing around 1.3645. The pair is probing the top-end of its recent 1.3350-1.3650 range, price action suggests it may be looking to break these highs and reassert its momentum higher. A sustained break above 1.3650 will initially target the year's highs just below 1.3800, through here it would open a move back to the 1.4200/1.4300 area.

- USD/CNH - Asian range 7.1004 - 7.1077, the USD/CNY fix printed 7.1013, Asia is currently dealing around 7.1050. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.05%, Gold $3681, US 10-Year 4.024%, BBDXY 1189, Crude Oil $64.43

- Data/Events : EZ CPI

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Stalls ahead Of 0.6000

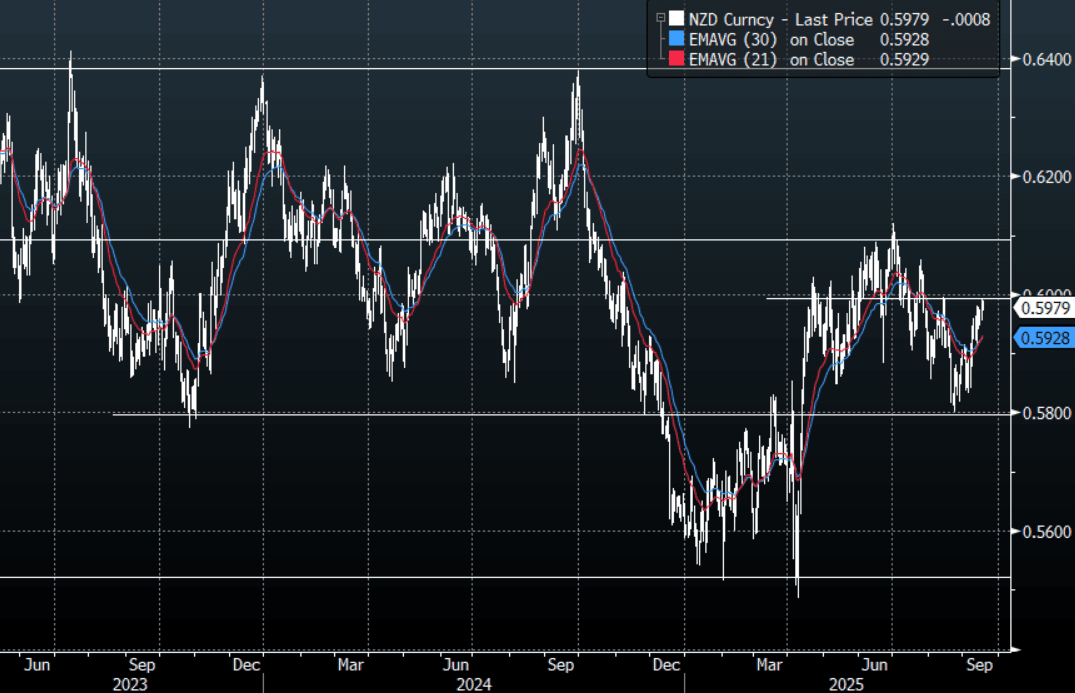

The NZD/USD had a range of 0.5975 - 0.5990 in the Asia-Pac session, going into the London open trading around 0.5980, -0.10%. US stocks finally paused for a breath ahead of the FOMC, but the USD can’t catch a break and looks to be breaking lower even before the market hears from Powell. The USD continues to extend lower, which is supporting the NZD. A close back above 0.6000 would negate any semblance of the downward pressure it was exhibiting, but for those that have a bearish view this remains a decent entry point to express that, the FOMC tomorrow morning could be the catalyst needed for a clearer direction.

- MNI AUS - NZ Q2 GDP Forecast At -0.3% q/q But Some Locals Expect A Deeper Drop. Q2 GDP prints on Thursday, 18 September and Bloomberg consensus is forecasting it to contract 0.3% q/q in line with the RBNZ’s projection in August. The goods-producing sector was particularly weak over the quarter. The central bank said that activity stalled in Q2 driven by weaker business and consumer sentiment following the US’ announcement of higher tariffs. Chief Economist Conway noted that the data in July signalled that the recovery looks to have continued in Q3.

- "NZ’s Willis Says Economic Growth Is Picking Up After 2q stutter, acknowledges GDP report is expected to show 2q contraction" - BBG

- MNI AUS - “Current Account Deficit Lowest In 4 years: There was a sharp narrowing in the Q2 YTD NZ current account deficit as a share of GDP with it printing at 3.7% after 4.2% and the peak in Q4 2022 of 9%. Q1 was revised sharply lower at $0.709bn (nsa) and 4.2% of GDP from $2.324bn and 5.7%. The deficit in Q2 widened marginally to $0.97bn (nsa) but seasonally adjusted it narrowed $0.7bn driven by a smaller primary income deficit.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD1.01b Sept 17), 0.5900(NZD860m Sept 17), 0.5935(NZD537m Sept 18) - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

INDONESIA: BI On Hold But Likely To Retain Easing Bias

Indonesia is widely expected to keep rates at 5% today with only 2 out of 38 analysts surveyed by Bloomberg forecasting a 25bp cut (see MNI BI Preview). Bank Indonesia (BI) holds monthly meetings and so has space to be cautious given its focus on FX stability and that it intervened to defend the rupiah in recent weeks following political instability and the replacement of respected Finance Minister Indrawati. However with signs of weakening growth and moderating inflation, it will keep its easing bias.

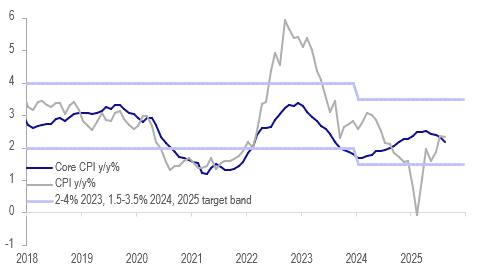

- Headline inflation moderated 0.1pp to 2.3% y/y in August with lower transportation inflation offsetting higher food driven by rice prices. Core moderated to 2.2% y/y from 2.3%, the lowest since October, reflecting softer domestic demand.

- Both measures are now below the mid-point of BI’s 1.5-3.5% target band but in August the central bank said that it is “confident” that inflation will remain within the corridor this year and next with inflation expectations anchored, spare capacity, effects from digitalisation and “managed imported inflation”.

Indonesia CPI y/y%

Source: MNI - Market News/LSEG

- The August S&P Global PMI showed an increase in manufacturers’ cost inflation due to the stronger USD which was passed on to customers driving selling price inflation to its highest since July 2024.

- Economic data since the August meeting have been mixed. Consumer confidence fell to its lowest in almost three years. Weak household sentiment is signalling a slowdown in consumption in Q3.

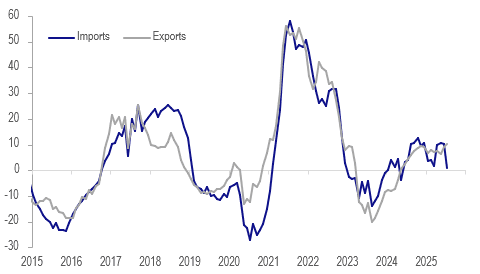

- July merchandise exports were robust rising 9.9% y/y with shipments to key destinations China and the US robust but also to the rest of ASEAN and the EU. In contrast, imports fell 5.9% y/y, a tentative signal of weak domestic demand.

- The S&P Global manufacturing PMI returned to positive territory with both domestic and export orders growing.

Indonesia merchandise exports vs imports y/y% 3-mth ma

Source: MNI - Market News/LSEG