MNI: RBA To Remain Cautious Despite Unemployment Surge

The sharp rise in Australia’s unemployment rate makes a November cash rate cut more likely, but the Reserve Bank of Australia is expected to wait for further confirmation from inflation and labour data before easing, with a move in December or early Q1 seen as more probable, former Bank staffers and economists told MNI.

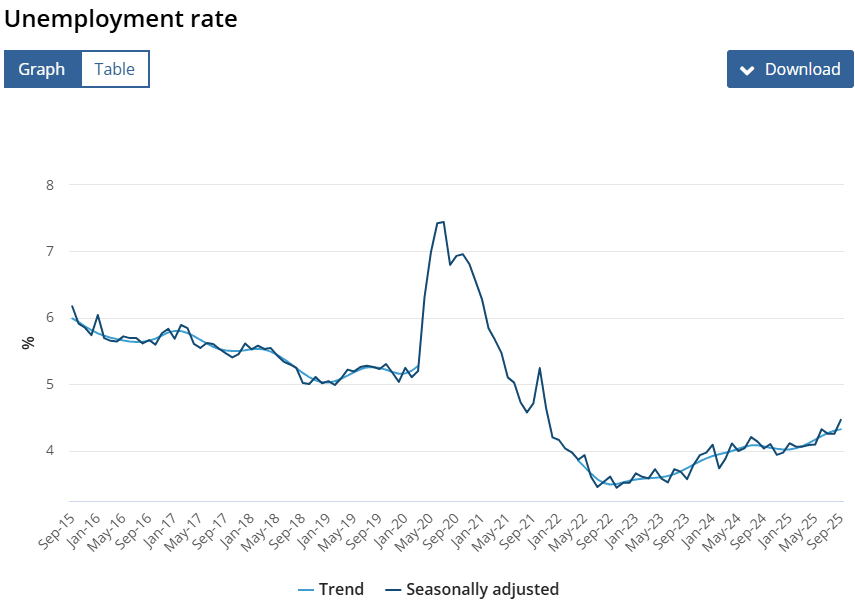

The jobless rate climbed to its highest since late 2021 in September at 4.5%, reinforcing that policy is at restrictive levels, however, former RBA economist Blair Chapman said the central bank’s conservative nature and uncertainty around upcoming data made a near-term move less likely.

“The only thing this data did was slightly increase the chance of a November cut, but only from a low base,” Chapman said.

Markets lifted the implied probability of a November rate cut by about 33 percentage points to 73% after the data’s release, with December sitting at 24%.

“December becomes potentially live if all the incoming data falls the right way, but it’s not binary at the moment," Chapman argued. "They can be patient, and the conservative approach is to do nothing.”

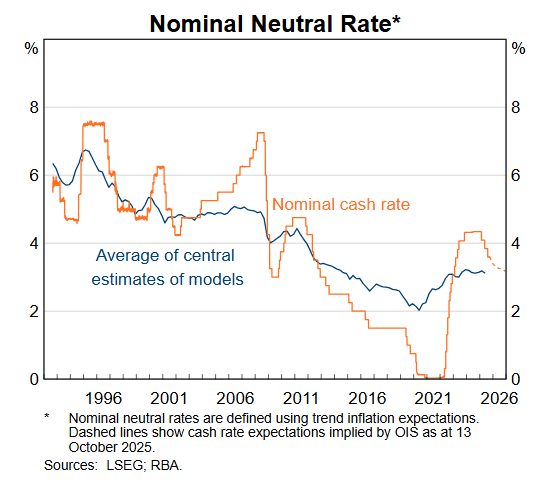

He said recent comments by RBA Assistant Governor Chris Kent showed the Bank viewed the 3.6% cash rate as close to its estimate of neutral, which would drive its reluctance to rush into easing. (See chart)

Chapman added that while one more rate cut this cycle is likely, it is far from guaranteed. “They don’t want to be active and risk getting it wrong in either direction. The economy is flowing roughly as they wanted, and they can afford to wait,” he said.

“It's an interesting time ... is the cycle over? Is there one more? If the data wasn't bouncing around as much and considering the stronger CPI, I'd say they were done, but today's labour market data with last month's results suggests there's another one coming.”

NEARING NEUTRAL

University of Sydney macroeconomics professor James Morley said the key determinant for a November move would be Q3 inflation due Oct 29.

“If they come in higher than the last forecast, then I think they will hold but note they will be tracking further slackening in the labour market,” Morley said. “If 4.5% [unemployment] or higher persists, I think it would indicate policy is tight, as I believe it is higher than NAIRU, so it could also lead to a notion that r* would justify a few more cuts in the next six months. Indeed, if the unemployment rate continues to increase, then they will start cutting below a perceived neutral level, assuming, again, no big upsides on inflation.”

He added that the RBA’s communication shows it believes the cash rate remains restrictive, but less so than previously thought, as private demand has held up better than expected.

“They’re trying to convey that policy is converging on neutral, but there’s a lot of uncertainty around what that actually is,” Morley said. “They’re effectively learning from the data what neutral means in real time. They’re also weighing the effects of recent rate changes – not just the level of the cash rate – and have seen some stimulative impacts, especially in housing.”

Morley noted that while the RBA could ease in December if upcoming pricing and GDP data confirm inflation is continuing to slow, a Q1 move was also possible. “They need confirmation that the disinflation trend is intact,” he said. “If Q3 inflation is higher than forecast, they’ll hold off, unless there’s a major shock – such as a sharp deterioration in China – that justifies a quicker response. But absent that, patience will dominate.”