MNI EUROPEAN OPEN: Precious Metals Higher To Start 2026

EXECUTIVE SUMMARY

- US DISCUSSES STRONGER UKRAINE SECURITY GUARANTEES WITH ALLIES - BBG

- GOLD AND SILVER OPEN 2026 WITH GAINS FOLLOWING HUGE ANNUAL SURGE - BBG

- AT LEAST 7 KILLED DURING WIDENING PROTESTS IN IRAN SPARKED BY AILING ECONOMY - AP

- ASIA'S FACTORIES END 2025 ON FIRMER FOOTING AS ORDERS PICK UP - RTRS

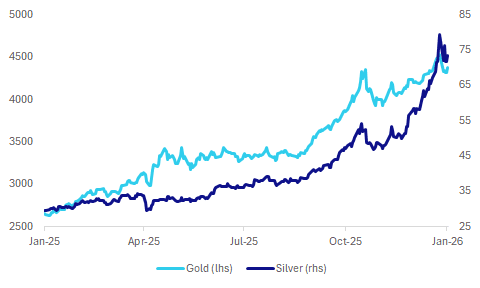

Fig 1: Gold & Silver Spot Price Trends

Source: Bloomberg Finance L.P./MNI

EU

ITALY (RTRS): “The United States sharply lowered proposed new duties on several Italian pasta makers following a preliminary review of their alleged anti-dumping activities, the Italian foreign ministry said on Thursday.”

RUSSIA (BBG): “President Donald Trump appeared to signal his displeasure with Russian President Vladimir Putin by sharing a New York Post editorial that sharply criticizes the Kremlin and argues Trump should “turn up the heat” on Russia.”

RUSSIA (NYT): “The tanker, which had been sailing to Venezuela to pick up oil, has claimed Russian protection, although the U.S. authorities say it is a stateless vessel.”

EUR (BBG): “ European Central Bank President Christine Lagarde said Bulgaria joining the euro area on Thursday is a testament to Europe’s ability to collaborate and defy international headwinds.”

US

TARIFFS (BBG): "President Donald Trump delayed tariff increases on upholstered furniture, kitchen cabinets and vanities, easing the pace of his levies as voter frustration over price levels continues to simmer."

UKRAINE (BBG): “US envoy Steve Witkoff said he held a “productive call” with European leaders on the next steps in President Donald Trump’s efforts to bring a halt to Russia’s war in Ukraine, following new challenges in the peace negotiations this week.”

CORPORATE (BBG): “Tesla Inc. ended last year with investors buying into Elon Musk’s views on autonomous vehicles, but the company likely sold fewer vehicles in the last six months than a year earlier.”

OTHER

IRAN (AP): “ Widening demonstrations sparked by Iran's ailing economy spread Thursday into the Islamic Republic's rural provinces, with at least seven people being killed in the first fatalities reported among security forces and protesters, authorities said.”

COMMODITIES (BBG): "- Gold and silver advanced as trading in 2026 kicked off, building on their best annual performances since 1979."

ASIA (RTRS): "Asia's factory powerhouses closed 2025 on a firmer footing, with activity swinging back to growth in several key economies as export orders picked up, helped by new product launches."

SOUTH KOREA (BBG): “Bank of Korea Governor Rhee Chang Yong said the recent won weakness doesn’t reflect the real strength of the country’s economy, and he vowed to oppose any US investment decisions that could threaten the foreign-exchange market’s stability.”

SINGAPORE (DJ): “Singapore's economy logged stronger-than-expected growth in 2025 due to expansion across the manufacturing and construction industries.”

CHINA

EVS (BBG): " BYD Co. met its full-year sales target and likely surpassed Tesla Inc. to become the world’s largest electric-vehicle maker in 2025 — a milestone overshadowed by a challenging outlook for the Chinese auto market in the year ahead."

MARKET DATA

AUSTRALIA DEC F S&P GLOBAL PMI MFG 51.6; PRIOR 52.2

SOUTH KOREA DEC S&P GLOBAL PMI MFG 50.1; PRIOR 49.4

MARKETS

US TSYS: Futures Slightly Weaker, No Cash Dealings With Japan Out

TYH6 is dealing weaker at 112-09+, -0-04+ from closing levels in today's Asia-Pac session, after subdued dealings.

- There has been no cash trading in the Asia session today, with Japan out on holiday.

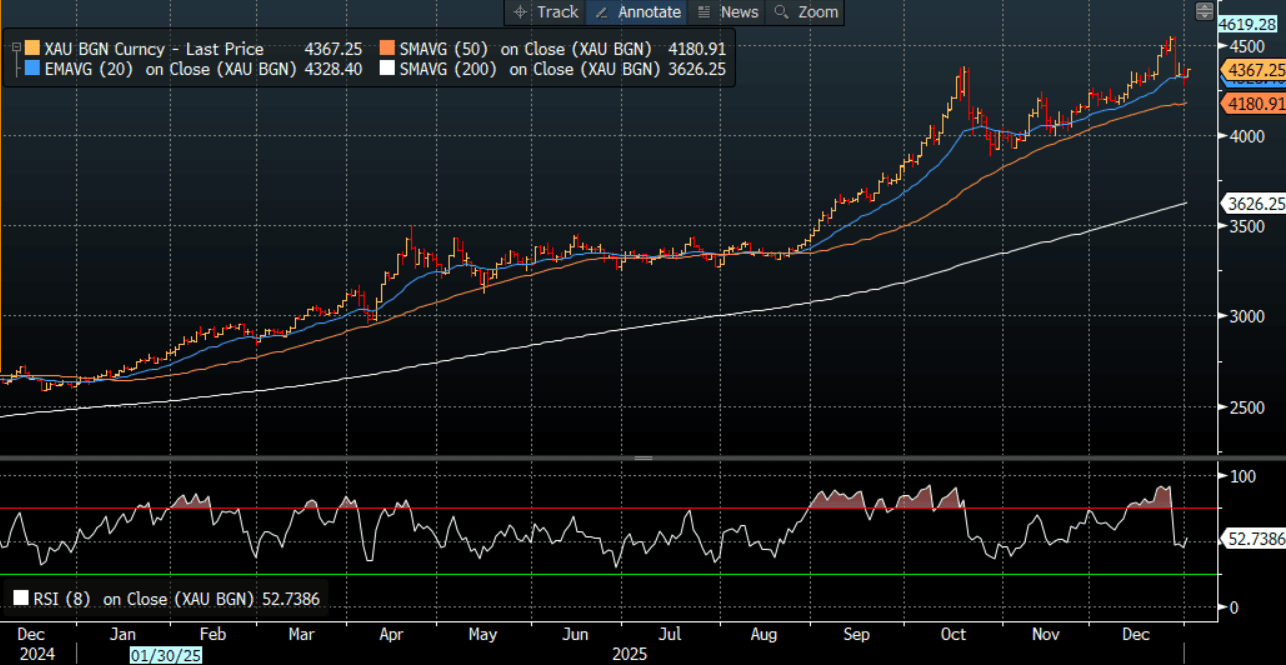

- Gold is ~1% higher at $4367/oz in today’s Asia-Pac session, with geopolitical risks continuing to provide strong safe-haven demand, underpinning the precious metal.

- Nonetheless, US equity-index futures for the Nasdaq 100 Index advanced ~0.5%, the S&P 500 Index contracts up +0.25%.

- Cash US tsys reversed early support on Wednesday following the final weekly claims data for 2025, which came out lower than expected. Volume, however, was moderate ahead of the early close for New Year's Eve.

AUSSIE BONDS: Heavy Session, Light Volume With No Cash Trading Of US Tsys

ACGBs (YM -4.5 & XM -6.0) are weaker, hovering near the session's worst levels.

- "Australia's manufacturing sector continued to expand in December 2025, supported by rising orders, increased production, and stronger hiring, even as supply constraints and cost pressures intensified, according to a survey by S&P Global published Friday. The headline seasonally adjusted S&P Global Australia Manufacturing Purchasing Manager's Index (PMI) held steady at 51.6, indicating a modest improvement in manufacturing sector conditions for the second consecutive month." - MTN via BBG

- There has been no cash trading in US tsys in today's Asia-Pac session with Japan out. 10-year US tsy futures are dealing at 112-10, -0-04 from closing levels.

- Cash ACGBs are 7-10bps cheaper with the AU-US 10-year yield differential at +65bps (based on US closing levels). At this level, the differential sits around its cycle high, the widest since mid-2022. December's price action has consolidated the differential's breakout above the 30bps range that had prevailed since November 2022.

- The bills strip has bear-steepened, with pricing flat to -5 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for February to 108% by June and 181% by December 2026.

- On Monday, the local calendar will be empty.

FOREX: USD Index Edges Lower, Higher Equities/Precious Metals Aid AUD, Yen Lags

After edging up in the final few trading days of 2025, the BBDXY index is down modestly in the first part of 2026 trade. The index is off a little under 0.10%, last near 1202.50/00. This leaves us above recent lows under 1200, but still in a downtrend that has persisted since late Nov last year. A clean break under 1200 is likely to see the low 1180 region targeted, which marked Sep lows last year for the index. In the G10 space, yen has lagged so far today, while the AUD has outperformed, up around 0.40%. Japan and China remain closed for the New Year break, which has no doubt curtailed liquidity and market interest to a degree.

- AUD/USD was last near 0.6700, up from late 2025 lows of 0.6660. Upside focus will rest on Dec highs of 0.6725/30. Beyond that level is 0.6800 and then 2024 highs around 0.6940/45.

- Cross asset sentiment is helping the AUD, with gold and silver posting solid gains so far today, while regional equity sentiment is positive (albeit led by the tech side). US equity futures are also higher, led by Nasdaq futures, but remain under 2025 highs.

- Data has been limited to final PMI reads for Dec. On the manufacturing side, Australia's print was revised down a touch but remained above 50. South Korea and Taiwan both moved back above 50.0, a positive sign for the global growth/trade backdrop.

- NZD/USD is little changed, last near 0.5760/65. NZ markets remain out for the New Year break. The AUD/NZD cross remains supported on dips. We were last near 1.1620, not far off 2025 highs (1.1635/40).

- USD/JPY has traded fairly narrow ranges, last 156.80/85, little changed for the session. Some underperformance may reflect the firmer equity start for regional markets and US futures.

- AUD/JPY is pushing back above 105.00, tracking towards late 2025 highs.

- EUR/USD has edged up, last 1.1760, with upside focus likely to rest around 1.1800, which marked late 2025 highs. GBP/USD is back to 1.34801, against late 2025 highs of 1.3530/35.

- Looking ahead, we have final PMI prints (for Dec) for the UK, EU and the US.

ASIA STOCKS: Tech Gains Continue, HK Higher, South Korea & Taiwan To Fresh Highs

The tone is mostly positive for those Asia Pac markets which are open today. Hong Kong gains are the strongest, the HSI up over 2% at this stage, while the Kospi has also risen strongly. Notably Japan and China markets remain closed for the new year period, returning next Monday. This is likely driving some lighter liquidity/interest in broader markets. US equity futures are tracking higher led by the tech side, with Emini's around 0.40% firmer, while Nasdaq futures are up close to 0.55%.

- The gains in US futures follow a modestly softer period in between Christmas and the new year. For Eminis near 6920, we remain short of recent cycle highs just above 7000.

- For the Hong Kong's HSI we are back above 26000, but still some distance to 2025 highs. The tech sub index is over 3.6%. This puts the index back to mid Nov levels. Sentiment is being aided by a 119% surge in Shanghai Biren Technology Co., after a successful IPO for the company. Baidu is also up strongly, after it submitted a proposal to spin-off its AI chip unit called Kunlunxin via a Hong Kong IPO, in which it currently holds around 60% (via BBG).

- Elsewhere, South Korea's Kospi is up over 1.3%, last around 4273. This puts the index at fresh record highs. Samsung has risen on reported positive customer feedback around one of its chips. The Taiex is up over 1.1% (also to fresh record highs).

- Trends are more muted elsewhere, the ASX 200 in Australia, a touch higher and holding above 8700.

- South East Asian markets are higher, except for Malaysia. Gains elsewhere are less than 1% at this stage.

OIL: Benchmarks Edge Up But Bear Threat Remains

Oil benchmarks have drifted a little higher in the first part of Friday trading, with both WTI and Brent up close to 0.50%. For Brent, we were last around $61.15/bbl, with support still evident under $60 at this stage, as this region has marked lows on a number of occasions through 2025. Still we are under all key EMAs, with the 50-day, currently around $62.65/70, acting as an upside resistance point through Nov/Dec of last year.

- WTI was last around $57.70/bbl. For WTI techs, MA studies are in a bear-mode position, highlighting a dominant downtrend. A key support and the bear trigger at $56.11, the Oct 17 low, has recently been breached. The break highlights a continuation of the downtrend and opens $53.77, a Fibonacci projection. Key S/T resistance is $61.25, the Oct 24 high.

- Focus remains on longer term over supply as a headwind for prices, the International Energy Agency is still forecasting a meaningful glut this year (3.8 million barrels per day, via BBG). There is some support in the near term given geopolitical risks around Venezuela, whilst domestic protests in Iran recently have also been in focus. Via BBG: "President Donald Trump’s administration stepped up a campaign against Venezuela’s oil exports by sanctioning companies in Hong Kong and mainland China, along with vessels accused of evading curbs."

GOLD: Strong Start To New Year After Best Year Since 1979

Gold is ~1% higher at $4367/oz in today’s Asia-Pac session.

- Geopolitical risks continue to provide strong safe-haven demand, underpinning the precious metal.

- Tensions between Saudi Arabia and the United Arab Emirates have flared when the kingdom warned its Gulf rival against endangering its security and said it would take all necessary measures to counter the threat.

- Today’s gains in bullion, along with silver's, build on their best annual performances since 1979.

- “While traders have flagged the metals could do well in 2026 on further US interest-rate cuts and dollar weakness, there’s near-term concern that broad portfolio index re-balancing may pressure prices. Given the metals have rallied, their presence in indices may have exceeded target allocations, prompting passive tracking funds to sell some contracts.” – BBG

Bloomberg Finance LP

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/01/2026 | 0815/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 02/01/2026 | 0845/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 02/01/2026 | 0850/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 02/01/2026 | 0855/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 02/01/2026 | 0900/1000 | ** | M3 | |

| 02/01/2026 | 0900/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 02/01/2026 | 0930/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 02/01/2026 | 1445/0945 | *** | S&P Global Manufacturing Index (final) |