AUSSIE BONDS: Heavy Session, Light Volume With No Cash Trading Of US Tsys

ACGBs (YM -4.5 & XM -6.0) are weaker, hovering near the session's worst levels.

- "Australia's manufacturing sector continued to expand in December 2025, supported by rising orders, increased production, and stronger hiring, even as supply constraints and cost pressures intensified, according to a survey by S&P Global published Friday. The headline seasonally adjusted S&P Global Australia Manufacturing Purchasing Manager's Index (PMI) held steady at 51.6, indicating a modest improvement in manufacturing sector conditions for the second consecutive month." - MTN via BBG

- There has been no cash trading in US tsys in today's Asia-Pac session with Japan out. 10-year US tsy futures are dealing at 112-10, -0-04 from closing levels.

- Cash ACGBs are 7-10bps cheaper with the AU-US 10-year yield differential at +65bps (based on US closing levels). At this level, the differential sits around its cycle high, the widest since mid-2022. December's price action has consolidated the differential's breakout above the 30bps range that had prevailed since November 2022.

- The bills strip has bear-steepened, with pricing flat to -5 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for February to 108% by June and 181% by December 2026.

- On Monday, the local calendar will be empty.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

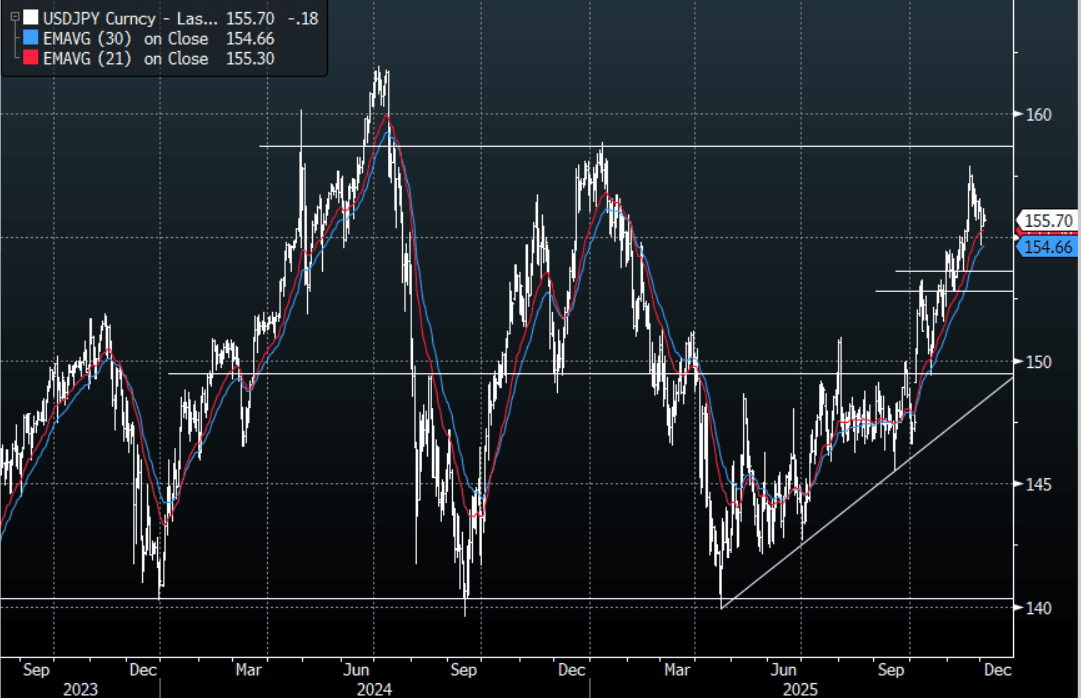

JPY: USD/JPY - Drifts Lower As The USD Trades Heavy

The USD/JPY range today has been 155.61 - 155.91 in the Asia-Pac session, it is currently trading around 155.70, -0.10%. The pair has drifted lower as the USD trades heavy across the board. The market is pricing in the fact that the Yen move looks like it could force the BOJ into action in December and a possible Hassett appointment brings more U.S. cuts into focus. This should keep the move that looked about to go parabolic a little more contained in the short-term but I suspect the market will still look for opportunities to express a long USD. Technically USD/JPY continues to look like it wants to test higher with the first big support back toward the 153-155 area which should see buyers reemerge. On the day I suspect we will continue to consolidate within a wider 155.00-156.50 range, with risk turning around its poor start to the week a short Yen might best be expressed in the crosses.

- (Dow Jones) - "Japanese government bond yields are higher as expectations for a near-term rate increase by the Bank of Japan continue. The BOJ's policy board is scheduled to meet on Dec. 18-19 for a final rate decision for the year. To gauge the economy's strength, investors will be focusing on economic indicators, including household spending data due Friday."

- MNI POLICY: Ueda Sharpens Dec Rate Hike, Risks Credibility. A hold at the Bank of Japan’s Dec. 18–19 meeting would be inconsistent with the bank’s recent market communications and would undermine its credibility, following Governor Kazuo Ueda’s comments on Monday that strongly indicated policymakers are set to raise the 0.5% rate this month, MNI understands.

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($1.27b). Upcoming Close Strikes : 153.00($1.2b Dec 4), 155.00($1.4b Dec 5), 156.00($1.14b Dec 8 ) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 88 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

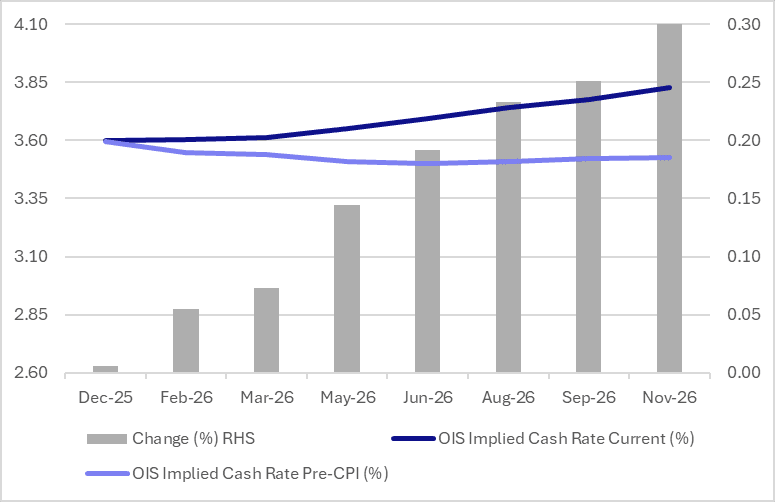

AUSSIE BONDS: Q3 Domestic Demand Drives Yields Higher, Hike Priced By Dec-26

ACGBs (YM -6.5 & XM -3.0) have bear-flattened after today’s Q3 GDP data. The market initially rallied on the data headlines but quickly reversed after details revealed underlying strength.

- Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details were a lot stronger than the headline, with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022.

- Cash US tsys are ~1bp richer in today’s Asia-Pac session.

- Cash ACGBs are 3-6bps cheaper with the AU-US 10-year yield differential at +56bps, the widest since mid-2022.

- The latest round of ACGB Dec-35 supply saw the weighted average yield print 0.30bp through prevailing mids. However, today’s cover ratio slumped to 2.3550x from 3.4875x.

- The bills strip has sharply steepened, with pricing -1 to -10.

- RBA-dated OIS pricing is 1-7bps firmer for meetings beyond May today. Pricing shows zero probability of a 25bp rate cut in December. More notably, the market has shifted to assign a 96% probability of a 25bp hike by December 2026.

- Tomorrow, the local calendar will see Trade Balance and Household Spending data.

- The AOFM plans to sell A$1000mn of the 2.75% 21 November 2028 bond on Friday.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

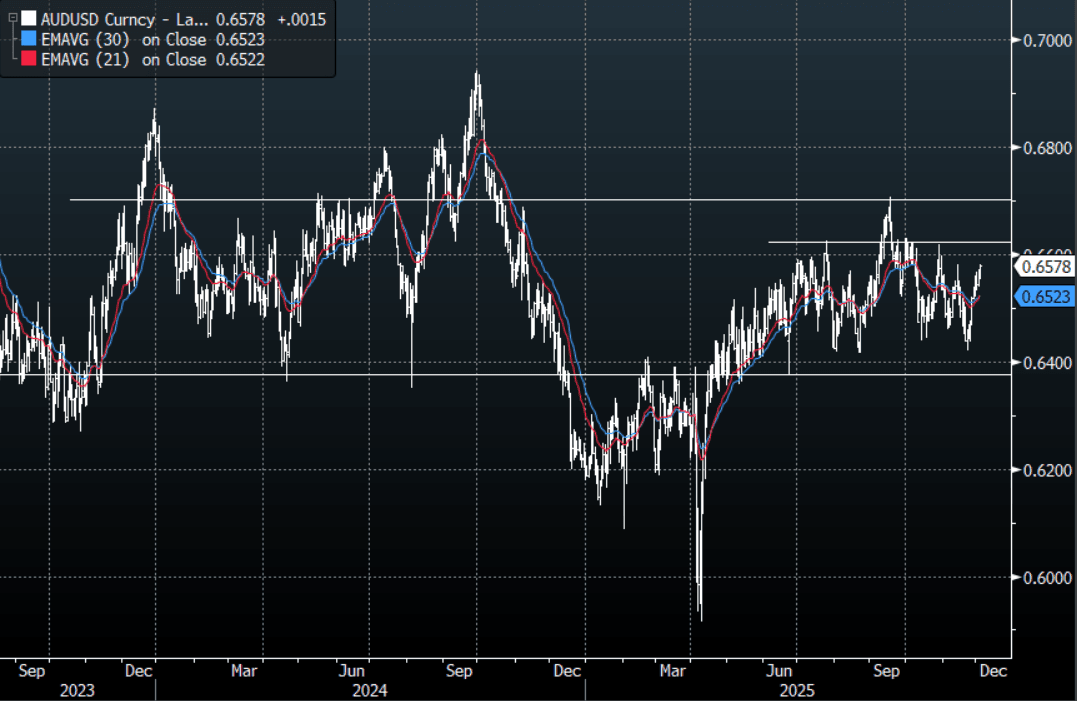

AUD: AUD/USD - GDP Data Not So Bad Sees AUD Bounce Back, Testing 0.6580

The AUD/USD has had a range today of 0.6553 - 0.6578 in the Asia- Pac session, it is currently trading around 0.6575, +0.20%. The AUD/USD had a brief look lower on the immediate GDP print back quickly recovered once the details showed underlying strength. The AUD has not backed off in all the noise and is pressing the pivot around 0.6580 within its wider 0.6350-0.6700 range. On the day, it feels like there is an air of inevitability around the AUD pushing above 0.6580 so I suspect dips back toward the 0.6535-0.6555 area could now be supported. A clear break above 0.6580 and the AUD could build some momentum looking to once again test the top end of its recent range, first target 0.6630 and then 0.6700.

- MNI AU - Strong Domestic Demand Growth To Keep RBA Cautious. Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details are a lot stronger than the headline with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022. The softer GDP print was due to a 0.5pp inventory detraction, largest since Q2 2023, which may reflect stronger demand driving a drawdown and which may be followed by a rebuild.

- MNI AU - RBA-dated OIS pricing is 1-7bps firmer for meetings beyond May today. Currently, pricing shows zero probability of a 25bp rate cut in December. More notable, the market has shifted to assign a 96% probability of a 25bp hike by December 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6475(AUD814m Dec 8), 0.6490(AUD710m Dec 4), 0.6500(AUD1.11b Dec 5) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 37 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P