FOREX: USD Index Edges Lower, Higher Equities/Precious Metals Aid AUD, Yen Lags

After edging up in the final few trading days of 2025, the BBDXY index is down modestly in the first part of 2026 trade. The index is off a little under 0.10%, last near 1202.50/00. This leaves us above recent lows under 1200, but still in a downtrend that has persisted since late Nov last year. A clean break under 1200 is likely to see the low 1180 region targeted, which marked Sep lows last year for the index. In the G10 space, yen has lagged so far today, while the AUD has outperformed, up around 0.40%. Japan and China remain closed for the New Year break, which has no doubt curtailed liquidity and market interest to a degree.

- AUD/USD was last near 0.6700, up from late 2025 lows of 0.6660. Upside focus will rest on Dec highs of 0.6725/30. Beyond that level is 0.6800 and then 2024 highs around 0.6940/45.

- Cross asset sentiment is helping the AUD, with gold and silver posting solid gains so far today, while regional equity sentiment is positive (albeit led by the tech side). US equity futures are also higher, led by Nasdaq futures, but remain under 2025 highs.

- Data has been limited to final PMI reads for Dec. On the manufacturing side, Australia's print was revised down a touch but remained above 50. South Korea and Taiwan both moved back above 50.0, a positive sign for the global growth/trade backdrop.

- NZD/USD is little changed, last near 0.5760/65. NZ markets remain out for the New Year break. The AUD/NZD cross remains supported on dips. We were last near 1.1620, not far off 2025 highs (1.1635/40).

- USD/JPY has traded fairly narrow ranges, last 156.80/85, little changed for the session. Some underperformance may reflect the firmer equity start for regional markets and US futures.

- AUD/JPY is pushing back above 105.00, tracking towards late 2025 highs.

- EUR/USD has edged up, last 1.1760, with upside focus likely to rest around 1.1800, which marked late 2025 highs. GBP/USD is back to 1.34801, against late 2025 highs of 1.3530/35.

- Looking ahead, we have final PMI prints (for Dec) for the UK, EU and the US.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Regional Bourses Mixed; China Lags Tech Rally Again

Whilst US indexes finished modestly up overnight, it wasn't enough to spur regional investor appetite with a mixed day across the region for major bourses. With most key AI tech stocks providing gains, tech heavy bourses were up again today with the NIKKEI and KOSPI leading. BITCOIN has recovered all of Monday's losses following news that China is cracking down on crypto speculators and that helped feed into better risk sentiment in general. China's major regional bourses are down and continue to lag the tech led boom elsewhere, with some market commentators suggesting that Chinese AI / tech names remain undervalued relatively to SK and JN names.

- The NIKKEI is up +1.5% to break above the 50,000 level to be 4.5% below the October high whilst the KOSPI was up again, by 1.2% today to break above the 4,000 level and close in on the early November high of 4,221

- China's major bourses are all lagging, with the Hang Seng the worst performer, down -0.95%. With Shanghai Comp and the CSI 300 doing little but trending weaker, it was down to Shenzhen to follow lower, dropping -0.35%

- The TAIEX is up +0.60% with TSMC up over 1% as US President Trump signs bill to deepen US-Taiwan ties .

- Having closed at a new high of 26,215 on November 27, the NIFTY 50 has fallen moderately each day since and is down -0.4% today at the open ahead of this week's RBI decision and the currency under pressure again.

- Jakarta and KL are moving in opposite directions with the JCI up +0.25% whilst the FTSE Malay KLCI is down -0.44% taking out some of its gains to start December.

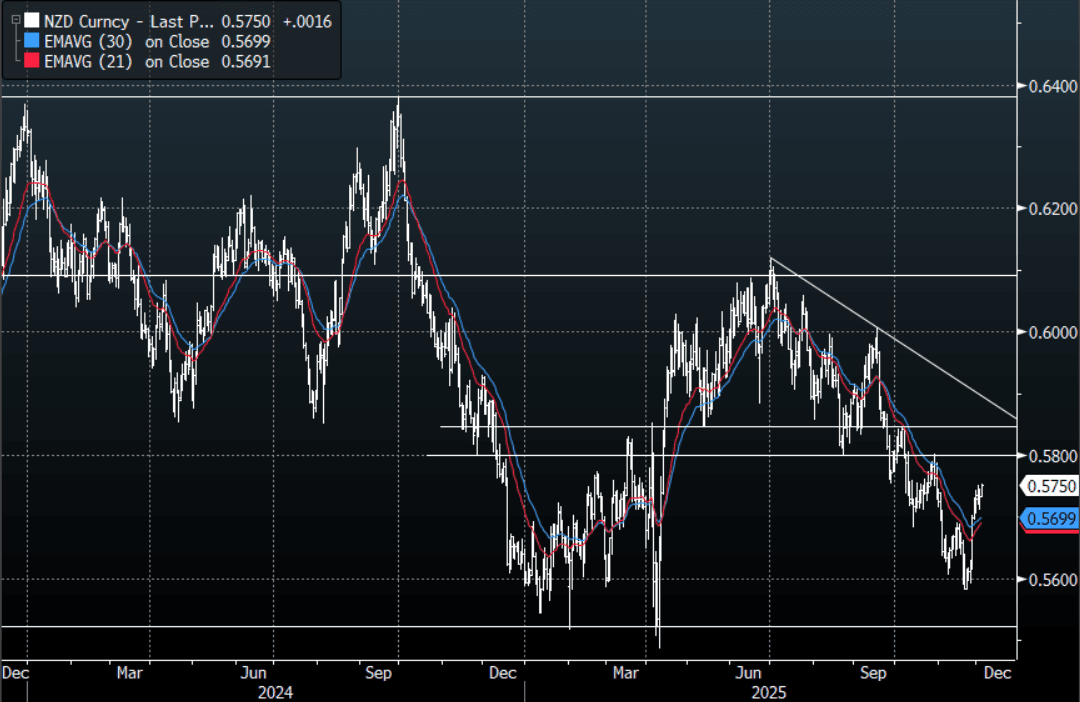

NZD: NZD/USD - Drifts Higher Back Testing 0.5760

The NZD/USD had a range today of 0.5732 - 0.5753 in the Asia-Pac session, going into the London open trading around 0.5750, +0.30%. The NZD/USD has drifted higher in the Asian session as the USD trades soft. Positioning could still be an issue in the short term. On the day it looks as though the NZD could remain well supported on dips, a sustained push back above 0.5760-70 should then potentially see the focus turn back toward the more important 0.5800-50 resistance. On the day support looks to be back toward the 0.5690-0.5710 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5575(NZD547m), 0.5730(NZD621m). Upcoming Close Strikes : 0.5670(NZD382m Dec 8), 0.5700(NZD332m Dec 5), 0.5730(NZD692m Dec 8 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 38 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

PRECIOUS METALS: Dovish Fed Outlook Driving Prices Up, Silver Reaches Record

Silver has reached another record high during Wednesday’s APAC trading continuing to be driven by expectations of a Fed December rate cut, a dovish new Fed Chair in 2026 and a tight physical market. The rally has encouraged speculators into the market and it is now flashing overbought. The metal is up 0.6% to $58.84/oz after reaching $58.947, above resistance at $59.563. Attention is focussed on resistance at $60.00.

- Gold is also higher today rising 0.4% to $4221.1 off the intraday peak of $4228.85.

- Bloomberg is reporting a 200t inflow into silver ETFs on Tuesday to their highest since 2022.

- There is growing conjecture that President Trump will choose his National Economic Council Director Bessent as the next Fed Chair, as he is expected to be more dovish. This is adding support to non-yield bearing assets, such as precious metals.

- The US dollar is softer (BBDXY -0.1%) and yields slightly lower. Equities are mixed with the S&P e-mini up 0.2% and Nikkei +1.5% but Hang Seng down 1.0% and CSI flat. Oil prices are little changed with WTI at $58.66/bbl. Copper is 0.7% higher.

- Later US November ADP employment, delayed September trade prices/IP and November services ISM/PMI print. European November services/composite PMIs and euro area October PPI are out. The ECB President Lagarde speaks before the European parliament and ECB’s Lane and BoE’s Mann also make appearances.