US TSYS: Futures Slightly Weaker, No Cash Dealings With Japan Out

TYH6 is dealing weaker at 112-09+, -0-04+ from closing levels in today's Asia-Pac session, after subdued dealings.

- There has been no cash trading in the Asia session today, with Japan out on holiday.

- Gold is ~1% higher at $4367/oz in today’s Asia-Pac session, with geopolitical risks continuing to provide strong safe-haven demand, underpinning the precious metal.

- Nonetheless, US equity-index futures for the Nasdaq 100 Index advanced ~0.5%, the S&P 500 Index contracts up +0.25%.

- Cash US tsys reversed early support on Wednesday following the final weekly claims data for 2025, which came out lower than expected. Volume, however, was moderate ahead of the early close for New Year's Eve.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

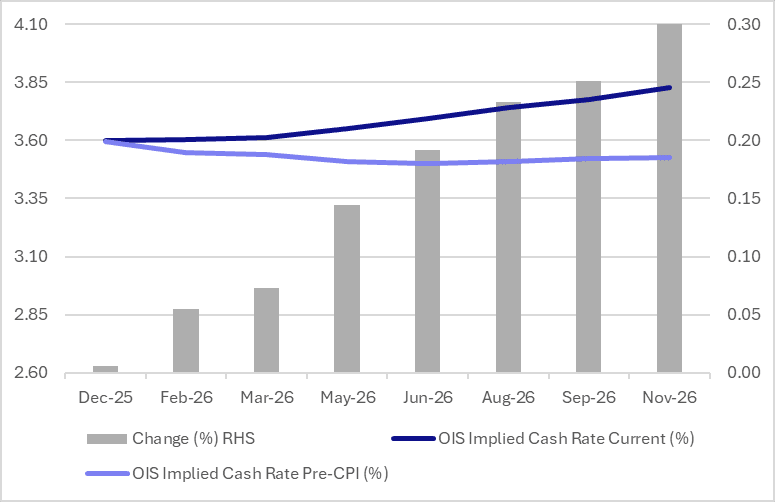

AUSSIE BONDS: Q3 Domestic Demand Drives Yields Higher, Hike Priced By Dec-26

ACGBs (YM -6.5 & XM -3.0) have bear-flattened after today’s Q3 GDP data. The market initially rallied on the data headlines but quickly reversed after details revealed underlying strength.

- Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details were a lot stronger than the headline, with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022.

- Cash US tsys are ~1bp richer in today’s Asia-Pac session.

- Cash ACGBs are 3-6bps cheaper with the AU-US 10-year yield differential at +56bps, the widest since mid-2022.

- The latest round of ACGB Dec-35 supply saw the weighted average yield print 0.30bp through prevailing mids. However, today’s cover ratio slumped to 2.3550x from 3.4875x.

- The bills strip has sharply steepened, with pricing -1 to -10.

- RBA-dated OIS pricing is 1-7bps firmer for meetings beyond May today. Pricing shows zero probability of a 25bp rate cut in December. More notably, the market has shifted to assign a 96% probability of a 25bp hike by December 2026.

- Tomorrow, the local calendar will see Trade Balance and Household Spending data.

- The AOFM plans to sell A$1000mn of the 2.75% 21 November 2028 bond on Friday.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

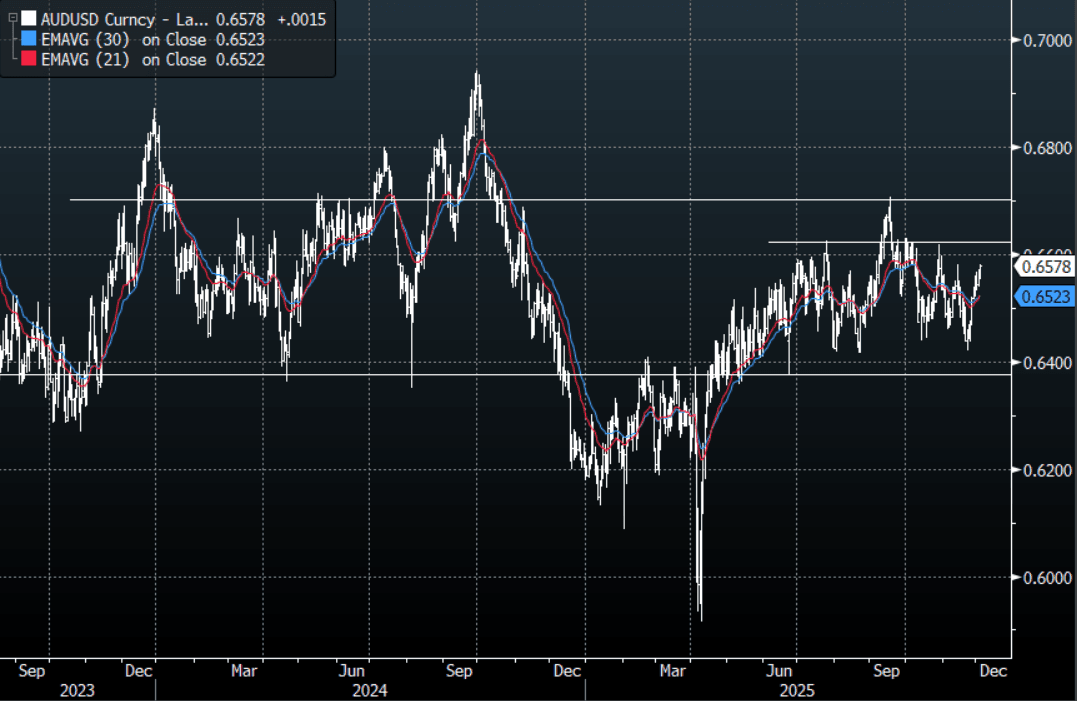

AUD: AUD/USD - GDP Data Not So Bad Sees AUD Bounce Back, Testing 0.6580

The AUD/USD has had a range today of 0.6553 - 0.6578 in the Asia- Pac session, it is currently trading around 0.6575, +0.20%. The AUD/USD had a brief look lower on the immediate GDP print back quickly recovered once the details showed underlying strength. The AUD has not backed off in all the noise and is pressing the pivot around 0.6580 within its wider 0.6350-0.6700 range. On the day, it feels like there is an air of inevitability around the AUD pushing above 0.6580 so I suspect dips back toward the 0.6535-0.6555 area could now be supported. A clear break above 0.6580 and the AUD could build some momentum looking to once again test the top end of its recent range, first target 0.6630 and then 0.6700.

- MNI AU - Strong Domestic Demand Growth To Keep RBA Cautious. Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details are a lot stronger than the headline with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022. The softer GDP print was due to a 0.5pp inventory detraction, largest since Q2 2023, which may reflect stronger demand driving a drawdown and which may be followed by a rebuild.

- MNI AU - RBA-dated OIS pricing is 1-7bps firmer for meetings beyond May today. Currently, pricing shows zero probability of a 25bp rate cut in December. More notable, the market has shifted to assign a 96% probability of a 25bp hike by December 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6475(AUD814m Dec 8), 0.6490(AUD710m Dec 4), 0.6500(AUD1.11b Dec 5) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 37 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

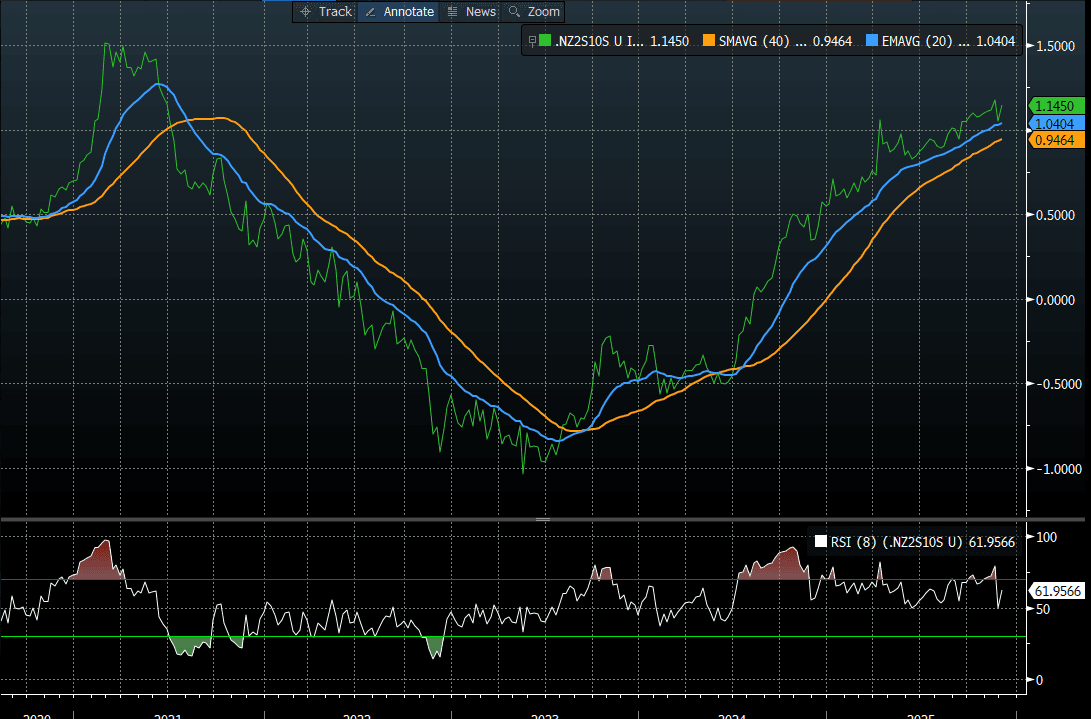

BONDS: NZGBS: Partial Unwind Of Post-RBNZ Sell-Off

NZGBs closed showing a bull-flattener, with benchmark yields 4-7bps lower. Nevertheless, yields remain 12-25bps higher than last week’s pre-RBNZ levels.

- On a relative basis versus its $-bloc counterparts, NZGBs also had a good day, with the NZ-US and NZ-AU 10-year yield differentials 6bps and 10bps lower, respectively.

- NZ commodity export prices fell 1.6% m/m in November versus -0.3% in October.

- Swap rates closed 2-7bps lower, with the 2s10s curve flatter. Nonetheless, the curve remains within striking distance of the 2021 peak (see chart).

- RBNZ-dated OIS pricing closed slightly softer across meetings. 2bps of easing is priced for February, while November 2026 assigns 31bps of tightening.

- Tomorrow, the local calendar will see Cotality Home Values and Volume of All Buildings data alongside NZ Government 4-Month Financial Statements.

- The NZ Treasury also plans to sell NZ$150mn of the 4.50% May-30 bond, NZ$225mn of the 4.50% May-35 bond and NZ$75mn of the 2.75% May-51 bond.

Bloomberg Finance LP