OIL: Benchmarks Edge Up But Bear Threat Remains

Oil benchmarks have drifted a little higher in the first part of Friday trading, with both WTI and Brent up close to 0.50%. For Brent, we were last around $61.15/bbl, with support still evident under $60 at this stage, as this region has marked lows on a number of occasions through 2025. Still we are under all key EMAs, with the 50-day, currently around $62.65/70, acting as an upside resistance point through Nov/Dec of last year.

- WTI was last around $57.70/bbl. For WTI techs, MA studies are in a bear-mode position, highlighting a dominant downtrend. A key support and the bear trigger at $56.11, the Oct 17 low, has recently been breached. The break highlights a continuation of the downtrend and opens $53.77, a Fibonacci projection. Key S/T resistance is $61.25, the Oct 24 high.

- Focus remains on longer term over supply as a headwind for prices, the International Energy Agency is still forecasting a meaningful glut this year (3.8 million barrels per day, via BBG). There is some support in the near term given geopolitical risks around Venezuela, whilst domestic protests in Iran recently have also been in focus. Via BBG: "President Donald Trump’s administration stepped up a campaign against Venezuela’s oil exports by sanctioning companies in Hong Kong and mainland China, along with vessels accused of evading curbs."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

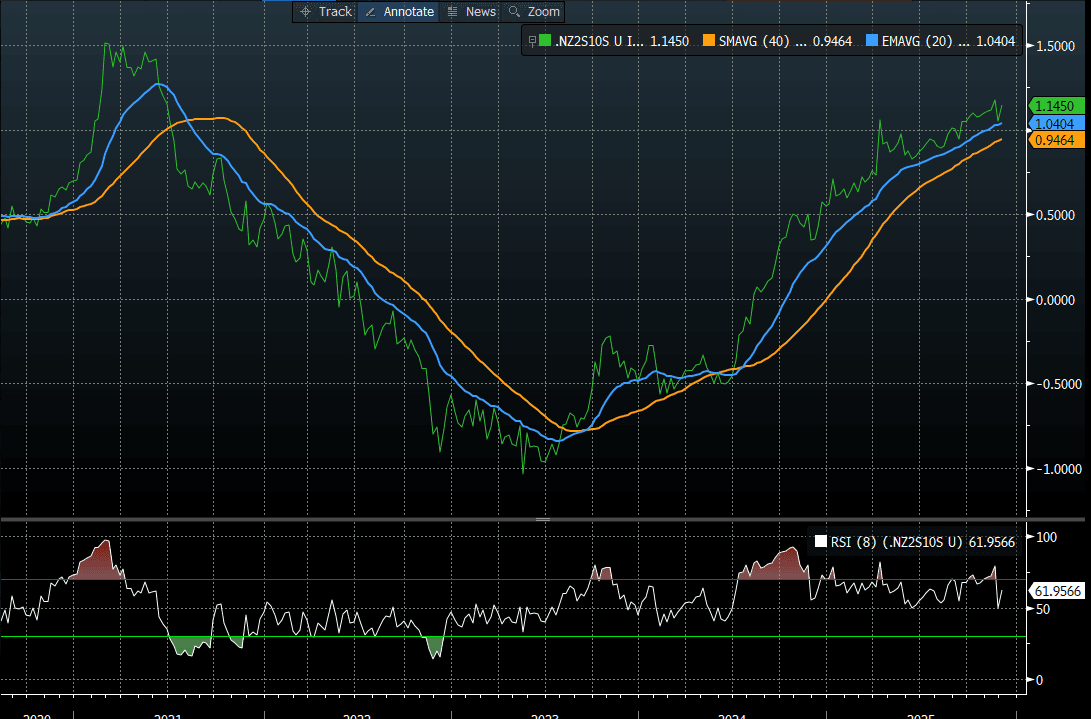

BONDS: NZGBS: Partial Unwind Of Post-RBNZ Sell-Off

NZGBs closed showing a bull-flattener, with benchmark yields 4-7bps lower. Nevertheless, yields remain 12-25bps higher than last week’s pre-RBNZ levels.

- On a relative basis versus its $-bloc counterparts, NZGBs also had a good day, with the NZ-US and NZ-AU 10-year yield differentials 6bps and 10bps lower, respectively.

- NZ commodity export prices fell 1.6% m/m in November versus -0.3% in October.

- Swap rates closed 2-7bps lower, with the 2s10s curve flatter. Nonetheless, the curve remains within striking distance of the 2021 peak (see chart).

- RBNZ-dated OIS pricing closed slightly softer across meetings. 2bps of easing is priced for February, while November 2026 assigns 31bps of tightening.

- Tomorrow, the local calendar will see Cotality Home Values and Volume of All Buildings data alongside NZ Government 4-Month Financial Statements.

- The NZ Treasury also plans to sell NZ$150mn of the 4.50% May-30 bond, NZ$225mn of the 4.50% May-35 bond and NZ$75mn of the 2.75% May-51 bond.

Bloomberg Finance LP

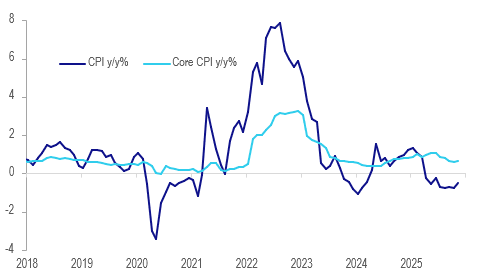

THAILAND: Price Pressures Remain Subdued, THB Stays Strong

Thai November CPI inflation improved slightly from prolonged very low rates and was marginally better than consensus expected. Headline printed at -0.5% y/y after -0.8% in October while core rose to +0.7% y/y from +0.6%. Both are holding below the Bank of Thailand’s 1-3% band and the Commerce Ministry is forecasting inflation to remain below target in 2026 at 0%-1%, which could drive further BoT easing.

Thailand CPI y/y%

Source: MNI - Market News/LSEG

- BoT expects headline inflation to rise to 0.5% in 2026 and return to the band early in 2027.

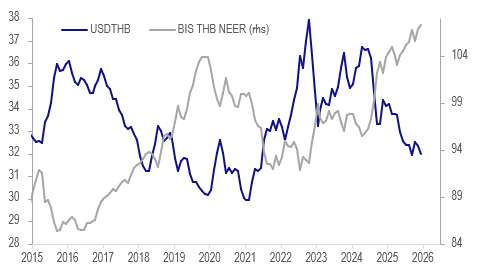

- In December to date, USDTHB is down 6.3% y/y and the BIS THB NEER up 3.2% y/y, which is adding to disinflationary pressures from soft domestic demand. The NEER has only fallen in 3 months in 2025. BoT is monitoring baht strength.

Thailand THB

- The next rate decision is 17 December and in late November the governor said that there is room to ease policy further as he wants a weaker currency, as it is not reflecting economic fundamentals. With rates at 1.5%, limited policy space has concerned some MPC members.

- November headline inflation was negative for the eighth consecutive month but the least negative since June. Government subsidies have put downward pressure on the series.

- Core only rose to 1% or above briefly in four months this year but BoT doesn’t believe that it will go negative and will gradually return to the bottom of its band.

- Recent severe weather events may cause some data volatility as they are likely to reduce demand but may also impact supply.

- Food inflation rose to +0.5% y/y in November from -0.2% driven by fresh food but rice & flour fell 1.8% y/y after +0.2%.

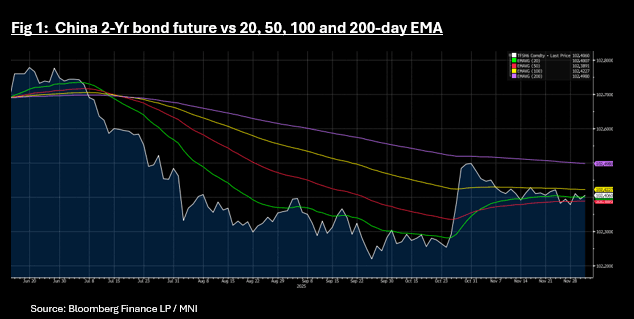

CHINA: Bond Futures Higher; 2-Yr Atop Key Tech Level

- China's bond futures are higher today, after yesterday's losses.

- The 10-YR is up +0.01 at 107.985, remaining below all major moving averages. The nearest above is the 50-day EMA of 108.045

- The 2-Yr is up +.01 at 102.404 and on its downside is near to the 20-day EMA of 102.40, with topside resistance at 102.422 via the 100-day EMA.

- Cash is steady with the 10-Yr -0.7bps lower at 1.83% and the 2-Yr at 1.416%