MNI EUROPEAN OPEN: Next Fed Chair To Believe In Lower Rates

EXECUTIVE SUMMARY

- TRUMP SAYS NEXT FED CHAIR WILL BELIEVE IN LOWER RATES 'BY A LOT' - RTRS

- TRUMP PLANS MILITARY BONUS, HOUSING REOFRM TO EASE PRICE ANXIETY - BBG

- US APPROVES TAIWAN ARM SALES WORTH UP TO $11 BILLION - AP

- NZ Q3 GDP BEATS EXPECTATIONS, UP 1.1% Q/Q - MNI BRIEF

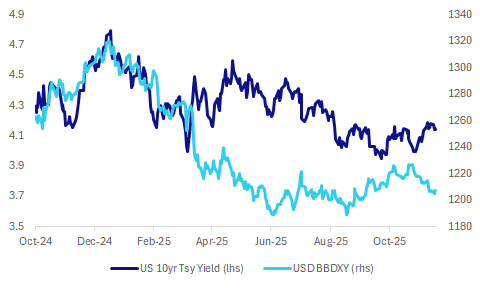

Fig 1: USD BBDXY & US 10yr Nominal Tsy Yield

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

CONSUMER CONFIDENCE (BBG): "UK Consumer Confidence Improves to -38 in December, BRC Says"

HOUSING (BBG): " Six wealthy areas in and around London are set for annual tax hikes in excess of 5% in the coming years, after the Labour government lifted a cap on council levies to make up for its efforts to shift funds to poorer communities."

EU

FRANCE (MNI): France's joint Senate and National Assembly Budget Committee will hold a key meeting on Friday to hammer out a compromise on the country's 2026 budget but sources close to the talks told MNI that the chances of success are no better than 50/50.

GERMANY (MNI INTERVIEW): Germany’s manufacturers are being beaten by China at home and abroad, a leading economist told MNI, calling for authorities to support future-oriented industries and boost productivity rather than attempting to reignite the economy through spending and tax cuts. (See MNI INTERVIEW: Germany Needs Solid China Strategy - Wambach)

ITALY (MNI): Italy will increase support measures for business by EUR3.5 billion in a late budget adjustment, with funds coming from reallocation and reprofiling of previously-assigned resources, sources close to the matter told MNI.

US

FED (MNI BRIEF): The Federal Reserve should continue cutting interest rates at a moderate pace with inflation cooling and effectively zero job growth and a "very soft" labor market, Fed Governor Chris Waller said Wednesday, adding rates are still 50 to 100 bps above neutral.

FED (RTRS): "U.S. President Donald Trump said on Wednesday the next chairman of the U.S. Federal Reserve will be someone who believes in lower interest rates "by a lot."

GOVERNMENT (BBG): "President Donald Trump looked to reassure Americans concerned about the rising cost of living by announcing plans to award a special holiday payment to military service members and roll out new housing reforms in the new year."

US/TAIWAN (AP): “The Trump administration has announced a massive package of arms sales to Taiwan valued at more than $10 billion, including medium-range missiles, howitzers and drones, a move that is sure to infuriate China.”

TECH (BBG): “OpenAI has held funding talks with investors to raise tens of billions of dollars at a valuation of $750 billion, according to a report in the Information. “

JAPAN

JAPAN/US (BBG): “A US-Japan consultation panel held its first meeting to consider initial projects for a $550 billion investment pledge that is a pillar of the two countries’ trade deal.”

OTHER

NEW ZEALAND (MNI BRIEF): “New Zealand’s economy grew 1.1% quarter on quarter in Q3, rebounding from Q2’s revised 1.0% contraction and exceeding the market forecast of a 0.9% increase, data released by Stats NZ on Thursday showed.”

AUSTRALIA (BBG): " Australia’s debt manager has cut its bond issuance plans for the fiscal year ending June 2026 more than expected, after the government forecasted stronger revenue from improved economic growth."

CANADA (MNI BRIEF): Mark Carney's first budget used up most of the fiscal room available after Justin Trudeau resigned, according to the parliamentary budget office, a view contrasting with the current prime minister's optimism about the affordability of "generational investments" to ease a U.S. trade war.

CHINA

FISCAL (YICAI): “Following the Central Economic Work Conference, experts interviewed by Yicai said they expect the fiscal deficit ratio to remain around 4% in 2026.”

ARREARS (YICAI): “The government must focus on clearing arrears to improve the business environment, said Xiao Weiming, deputy secretary-general at the National Development and Reform Commission, at the China Economic Annual Conference.”

MNI: PBOC Net Injects CNY69.7 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY88.3 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The PBOC conducted another CNY100 billion via 14-day reverse repos. The operation led to a net injection of CNY69.7 billion after offsetting maturities of CNY118.6 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4053% at 09:36 am local time from the close of 1.4423% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Wednesday, compared with the close of 48 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.0583 Thurs; +3.59% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.0583 on Thursday, compared with 7.0573 set on Wednesday. The fixing was estimated at 7.0430 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND Q3 GDP Q/Q 1.1%; MEDIAN 0.9%; PRIOR -1.0%

NEW ZEALAND Q3 GDP Y/Y 1.3%; MEDIAN 1.3%; PRIOR -1.1%

AUSTRALIA DEC CONSUMER INFLATION EXPECTATION 4.7%; PRIOR 4.5%

CHINA NOV SWIFT GLOBAL PAYMENTS CNY 2.94%; PRIOR 2.47%

MARKETS

US TSYS: Yields Lower as Equities Struggle

US bond futures were all up marginally today, as equity markets continue to struggle across Asia today. The US 10-Yr is up +02+ at 112-18+, near to the topside resistance from the 20-day EMA of 112-19+.

Cash is strong with the curve lower by up to -1.7bps, with the front end outperforming.

- The 2-Yr is down -1.7bps to 3.468%

- The 5-Yr is down -1.6bps to 3.684%

- The 10-Yr is down -1.2bps to 4.143%

- The 30-Yr is down -0.8bps to 4.82%

Our compilation of sell-side analyst expectations for Thursday's CPI report uses a narrower range of previews - namely, those that included core CPI forecasts to two decimal places or more for the 2-month or Oct and Nov % M/M changes. Within a range of 0.18-0.29% for average core CPI % M/M over October and November, Barclays is at the high end of expectations while NatWest is at the low end. A few summaries below:

- Barclays: Core CPI to average 0.29% M/M across Oct-Nov (two-month cumulative increase of 0.58%), with headline averaging 0.26% M/M (two-month cumulative of 0.52% M/M). "We expect the uptick to be led mainly by core goods prices (led by used car prices rebounding). We estimate services inflation to have also gathered steam, partly led by a rebound in OER CPI following the downside surprise in September."

- Nomura: Core CPI to average 0.245% M/M across Oct-Nov (0.228% Oct, 0.263% Nov); headline 0.24%. "We expect core goods inflation remained strong due to tariff effects as well as higher used vehicle prices.

- Goldman Sachs: Core CPI to average 0.21% M/M across Oct-Nov (0.16% Nov, 0.25% Oct), headline CPI to average 0.20% M/M across Oct-Nov (0.27% Nov, 0.14% Oct). "we have penciled in upward pressure from tariffs on goods categories that are particularly exposed worth +0.08pp on core inflation on average across October and November"

- NatWest: Core CPI to average 0.18% M/M across Oct-Nov (cumulative 0.35%), headline CPI to average 0.20% M/M across Oct-Nov (cumulative 0.40%)."we suspect it will be extremely challenging to try to draw many firm conclusions on this release."

Tonight there is a US$80bn 4-week bill and the US$80bn 8-week bill.

JGBS: Futures Drift Higher, 10yr Yield Off Highs, BoJ & National CPI Tomorrow

JGB futures have maintained a positive bias post the lunchtime break, last 133.36, +.13 versus settlement levels. This has been the tone as well in US Tsy futures and Aussie bond futures as well. For JGB futures we still have a gap to close with highs from late last week just above 133.70. JGB yields sit off earlier highs.

- News flow has been light with just weekly investment flows data on tap today. Cabinet Secretary Kihara stated that monetary policy should be left to the BoJ (in line with other government officials), while noting that market moves, including long term rates, are being watched closely (via RTRS).

- The 10yr JGB yield is back closer to 1.97% (earlier cycle highs were close to 1.985%), while the 20 and 40yr tenors are back closer to flat. The 30yr is still holding up a bps, last 3.37%.

- Market pricing for tomorrow's BoJ meeting outcome has an implied rate of 0.72% (versus an effective rate of 0.478%), so close to fully priced. Another full 25bps hike is priced for Sep next year.

- We get the National CPI print for Nov ahead of the BoJ tomorrow. The market expects headline at 2.9%y/y, while the core measures are seen at 3.0%.

AUSSIE BONDS: Yields Lower, AOFM Cuts Issuance Forecast, Inflation Exps Firm

Aussie bond futures have had a positive bias so far today, with the 3yr (YM) outperforming, last +4bps to 95.835. The 10yr was last up a touch to 95.20. The bias elsewhere in Asia Pac bond futures has mostly been positive, while US Tsy futures have also ticked up. The AOFM announced a A$25bn reduction in planned issuance for the 2025-26 financial year (which comes after the mid fiscal year update from the government). ACGB yields are lower led by the front end, off around 3.5bps. The 3yr last at 4.085%, while the 10yr is tracking just under 4.74%.

- The AOFM lowered its estimate for 2025-2026 bond issuance to A$125bn, from A$150bn (with this estimate made back in the middle of this year). Note CBA had stated markets expected around A$130bn in issuance (via BBG). While, via BBG, "Australia’s debt manager is likely to keep its A$2 billion weekly bond issuance run rate to meet its updated financing target, according to National Australia Bank."

- The 3yr yield remains close to the mid point of recent ranges, likewise for the 10yr. The 3/10s curve is at +65bps, slightly steeper, while the AU-US 10yr spread is a touch higher at +60bps.

- On the data front, the Melbourne Institute inflation gauge rose to 4.7% in Dec, from 4.5% prior. This below 2025 highs of 5.0%, but well up on the trough of 3.6%.

- Market pricing for a full hike at the Feb meeting remains a little over 30%.

- Tomorrow we get Nov private credit data.

BONDS: NZGB Yields Hold Weaker Bias, Despite Q3 GDP Beat, Recent Ranges Holding

NZGB yields are holding lower, despite the earlier Q3 NZ GDP beat. We are around 1-2.5bps lower across the benchmarks, led by the back end. The 2yr last near 2.71% (off a little over 1bps), while the 10yr is close to 4.42%, (off around 2.5bps). These moves leave us still within recent ranges, with Dec lows for the 2yr just under 2.70%, while the 10yr is comfortably above levels from the start of the month (near 4.25%). The lead for NZGB yields has been negative from softer US Tsy yields and lower Aussie bond yields as well so far today.

- Earlier we had Q3 GDP, which rose 1.1%q/q (against a market forecast of 0.9% and the RBNZ projection of 0.4%). Y/Y growth also improved to 1.3%, from a revised -1.1%y/y Q2 fall. The downside Q2 revisions, likely tempered the market reaction today, with the RBNZ still likely to be mindful of the low base growth is coming from. Q3 consumption also only rose modestly.

- The 2yr swap rate is holding 2bps lower, last just under 2.74%, but still largely range bound.

- Market pricing in terms of the RBNZ outlook, has little easing risks for the first part of next year, while a full hike is priced by the Oct meeting.

- Note tomorrow, we get Dec ANZ consumer confidence figures, Nov trade data, as well as ANZ business confidence figures.

FOREX: USD - BBDXY Tries To Bounce As Risk Turns Lower

The BBDXY has had a range today of 1206.93 - 1207.87 in the Asia-Pac session; it is currently trading around {BBDXY Index}. The USD has started to react to the risk off backdrop eventually and climbed back toward 1209 overnight before stalling again. On the day I still have very little conviction on direction, look for initial resistance again back towards the 1209-1210 area and above here the more important 1213-1216 area where sellers should remerge initially. Can this 1204 area continue to provide support if not a move below here would target 1198-1200.

- EUR/USD - Asian range 1.1735-1.1746, Asia is currently trading {EURUSD Curncy}. The pair found good demand back toward 1.1700 overnight and has largely shrugged off worries surrounding risk. On the day, support remains toward 1.1680-1700 initially, a break below here could potentially signal a deeper pullback.

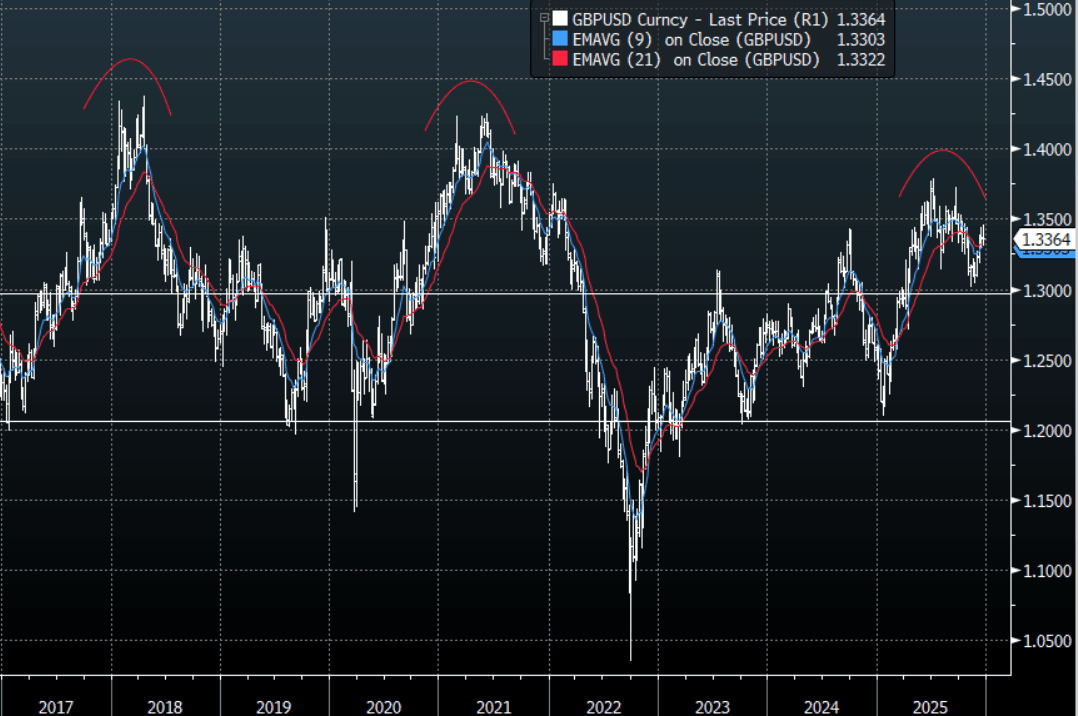

- GBP/USD - Asian range 1.3362-1.3381, Asia is currently dealing around {GBPUSD Curncy}. The pair has again rejected a move toward 1.3450 and is starting to show the first signs of exhaustion. On the day, continue to watch for selling pressure above 1.3400, if this area continues to hold, look for a pullback to the more important 1.3250/1.3300 area. I continue to watch for signs of GBP potentially topping out, are we seeing the first signs ?

- Cross asset : SPX +0.05%, Gold $4330, US 10-Year 4.14%, BBDXY 1207, Crude Oil $56.34

- Data/Events : EZ Construction Output/ECB Deposit Facility Rate, France Manufacturing Confidence

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

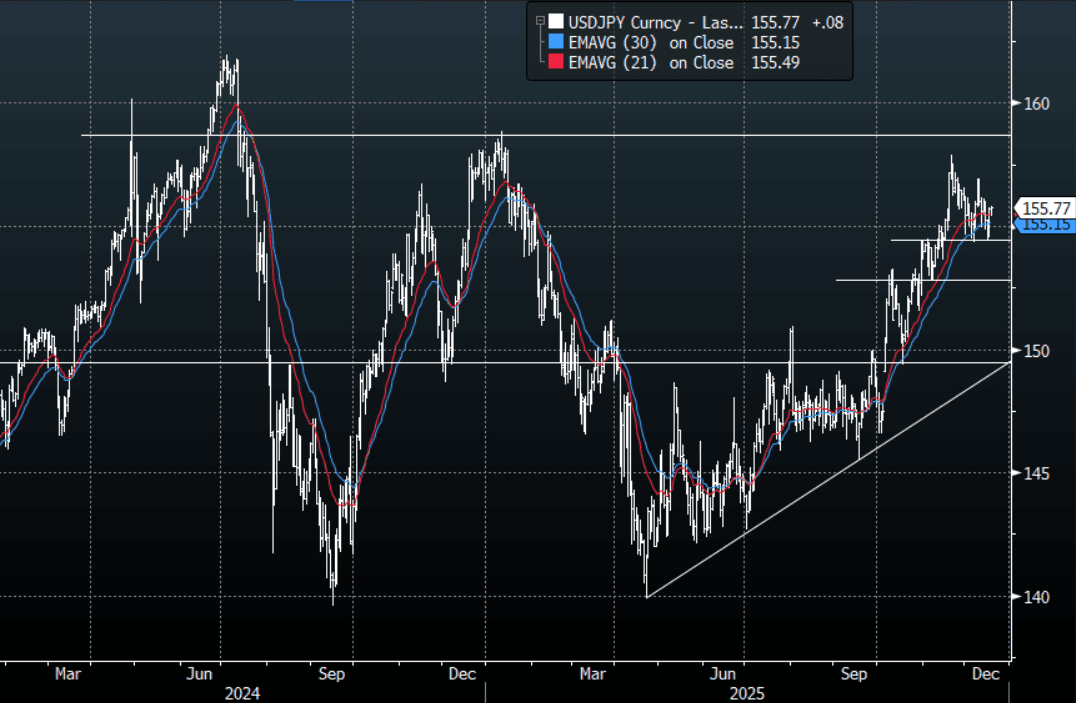

JPY: USD/JPY - Consolidates On A 155 Handle Ahead Of BOJ

The USD/JPY range today has been 155.43 - 155.81 in the Asia-Pac session, it is currently trading around {USDJPY Curncy}. The support around 154.50 proved to be rock solid again yesterday and price then bounced working through the resistance around 155.30 before extending higher aided by the move in oil. The way risk sentiment is quickly souring I am surprised the Yen is trading so weak, especially in the crosses. The market is pricing in a hike by the BOJ tomorrow, for the time being this is keeping the JPY contained and confined to a wider 154.00-157.00 range having capped its upward momentum. Technically USD/JPY is in an uptrend, the first big support is back toward the 152.50-154.50 area. On the day, look for resistance back toward the 156.00-156.30 area initially, support is seen back toward 155.15-45 where demand was seen initially in our session.

- Options : Close significant option expiries for NY cut, based on DTCC data: 157.00($4.15b), 158.00($4.98b). Upcoming Close Strikes : 153.00($2.83b Dec 19), 155.00($2.18b Dec 19), 158.00($1.85b Dec 19) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 105 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

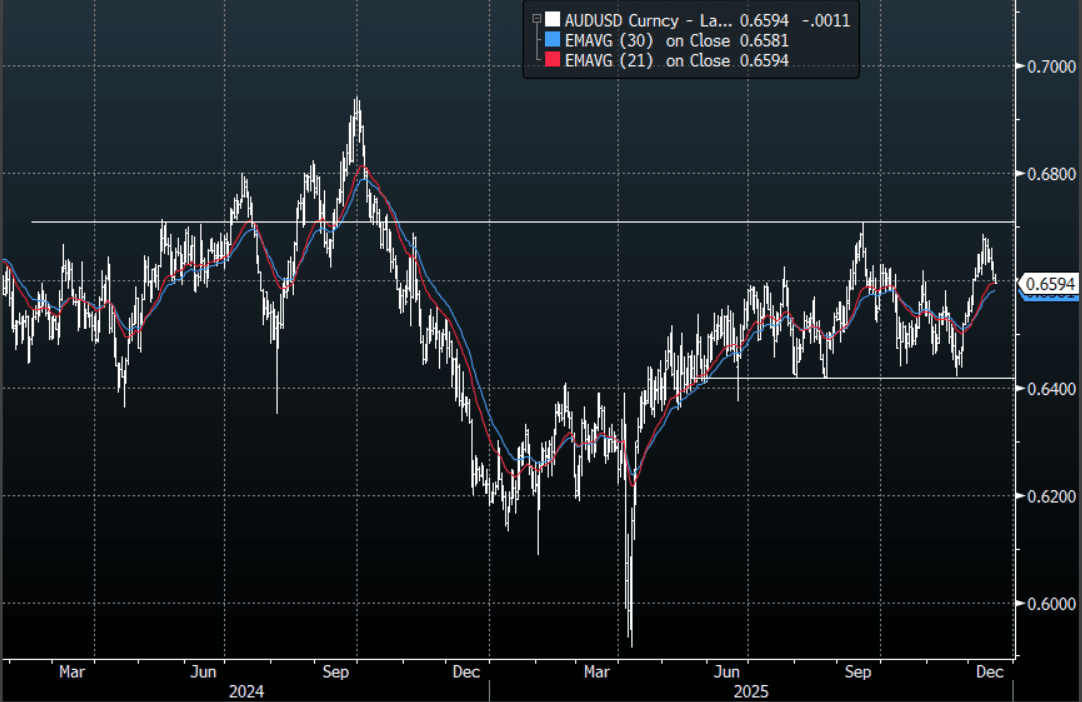

AUD/USD - Trades Heavy Around 0.6600 As Risk Wobbles

The AUD/USD has had a range today of 0.6593 - 0.6612 in the Asia- Pac session, it is currently trading around {AUDUSD Curncy}. The bounce in AI lasted 1 day and is lower again, the move is starting to turn ugly as sentiment is quickly changing. The NASDAQ and the S&P both look to potentially be putting in double tops and the likes of Nvidia is approaching some pivotal levels as well. This does not augur well for risk and creates significant headwinds for the AUD which trades with a high correlation to it. The AUD price action for the moment remains consolidative, but I do remain wary of what seems to be unfolding in US stocks. Technically while the AUD remains above 0.6500-0.6550 dips should continue to be supported. Watch to see if this 0.6600 area can continue to hold in the face of this souring in sentiment, if not we could see a deeper pullback towards the 0.6500-50 support. On the day I suspect sellers would be looking to fade a bounce back toward the 0.6625-0.6645 area initially looking to see if we can break back below 0.6590-0.6600.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD1.07b), 0.6625(AUD849m), 0.6675(AUD989m). Upcoming Close Strikes : 0.6675(AUD1.31b Dec 19), 0.6700(AUD1.57b Dec 19) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

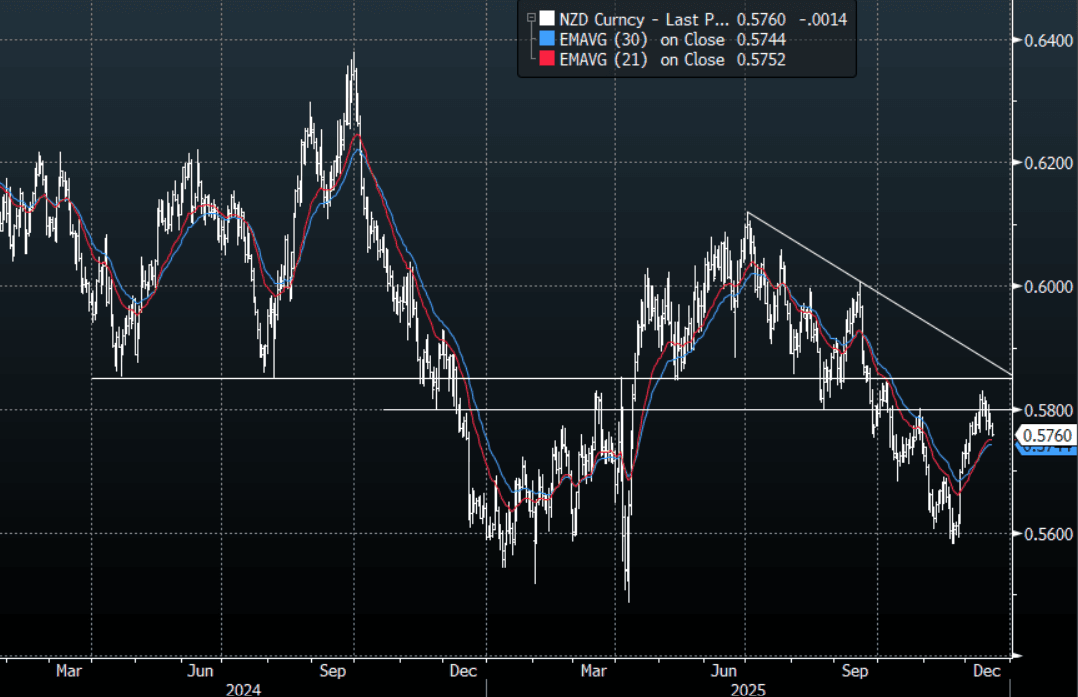

NZD/USD - Drifts Lower, Playing Catch Up To The Move In Risk

The NZD/USD had a range today of 0.5755-0.5778 in the Asia-Pac session, it is currently trading around {NZD Curncy}. The NZD traded a little lower in our session, unable to move higher on a better GDP print. The AI backdrop is starting to sour as sentiment is quickly changing. The NASDAQ and the S&P both look to potentially be putting in double tops and the likes of Nvidia is approaching some pivotal levels as well. This does not augur well for risk and creates significant headwinds for the AUD & NZD which trade with a high correlation to it. The NZD is consolidating its gains above 0.5700-0.5750 and for the most part has been left unscathed by the souring of sentiment. Can it continue to ignore it if the correction builds momentum? On the day, I will be watching the price to see if it can shrug this off, if so then the range will remain, support is back toward 0.5740-0.5760 and resistance is around 0.5810-30. A break through that support could signal the potential for a deeper pullback.

- MNI BRIEF: NZ Q3 GDP Beats Expectations, Up 1.1% Q/Q. New Zealand’s economy grew 1.1% quarter on quarter in Q3, rebounding from Q2’s revised 1.0% contraction and exceeding the market forecast of a 0.9% increase. The outcome was also stronger than the Reserve Bank of New Zealand’s most recent forecast, which had expected GDP to rise 0.4%.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5650(NZD410m), 0.5690(NZD531m), 0.5860(NZD471m). Upcoming Close Strikes : 0.5530(NZD475m Dec 23), 0.5630(NZD594m Dec 19), 0.5750(NZD459m Dec 19) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Overnight Tech Falls Drag Asian Bourses Lower

Falls in US tech stocks overnight spilled over into Asia today with key AI tech names falling, dragging down key indexes. Japanese stocks had the dual pressure of an expected interest rate hike tomorrow from the BOJ and downward pressure from tech stocks, with key tech stock Softbank Group down -3.3%. The tech weakness spilled over into Korea with Samsung down -1.3% and SK Hynix down -5%. AI remains a major long-term structural theme for Asian tech manufacturers and is a key driver of performance, especially in the semiconductor sector but given the run up in stocks year to date, a correction was increasingly likely. Asia's equity markets and capital flows are impacted by US monetary policy and as such, eyes will be on the CPI release for November tonight.

- The NIKKEI is down -0.85% today and down over 3% for the week, whilst the KOSPI is down -1.3% and nearly 3% for the week as tech stocks struggle.

- China's bourses are mixed with the Hang Seng down -0.44%, CSI 300 down -056%, Shenzhen down -0.17% whilst the Shanghai Comp is up +0.16% as tech firms buck regional trends with modest gains.

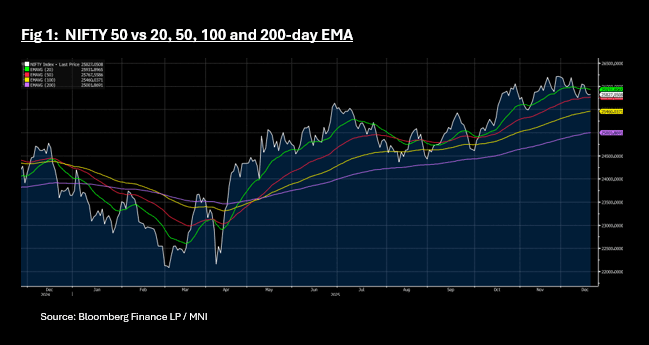

- The NIFTY 50 is up modestly, though down for the week as foreign institutional investors continue to sell as valuations near 5-year peaks. The NIFTY 50 at 25,832 is near the 50-day EMA of 25,767 as downside resistance, with topside resistance from the 20-day EMA at 25,932.

- SE Asia's bourse seemingly have their focus on the US data release with Jakarta and KL near flat, whilst the SE Thai is down -0.20%.

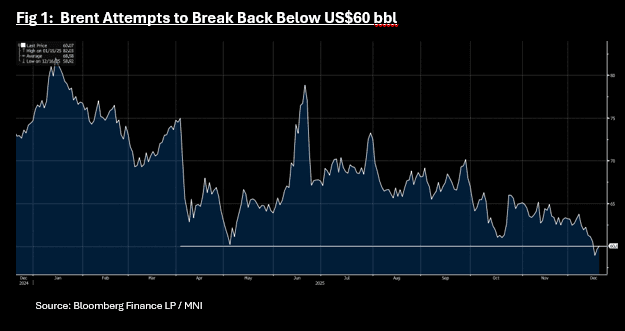

Oil Moderates with Limited New Venezuela Headlines

- After gains of over 2% yesterday, WTI has given some of those gains back in the Asia trading session. As US President Trump called a press conference from the White House, many expected new announcements on Venezuela and with them not forthcoming, WTI is down -0.28% at US$56.35 bbl.

- Brent is down -1.04% at US$60.06 bbl as it attempts to break back below US$60 bbl having closed below Tuesday.

- Yesterday US President Trump announced a blockade of Venezuela's sanctioned oil flows stating that "Venezuela is completely surrounded by the largest (US) armada ever assembled in the history of South America."

- The rise in prices may be a short term issue as the Venezuelan oil supply is tiny in the context of global oil supply and with supply factors driving prices lower, they will likely reassert themselves in coming days.

- There are also suggestions now that the US is considering targeting Russian President Putin's shadow fleet of oil tankers should the Kremlin not accept a peace deal to end the conflict in Ukraine. This comes as BBG reports a fleet of tankers laden with Russia's oil has expanded of China's east coast following the decline in purchases from India.

- EIA data released overnight shows that US crude inventories declined to 424 million barrels, the second consecutive week of nationwide declines. That drop in stockpiles was partly offset by 249,000 barrels injected into the Strategic Petroleum Reserve. Inventories at Cushing, Oklahoma, declined to 20.9 million barrels, the fifth draw on stocks at the hub in six weeks.(per BBG)

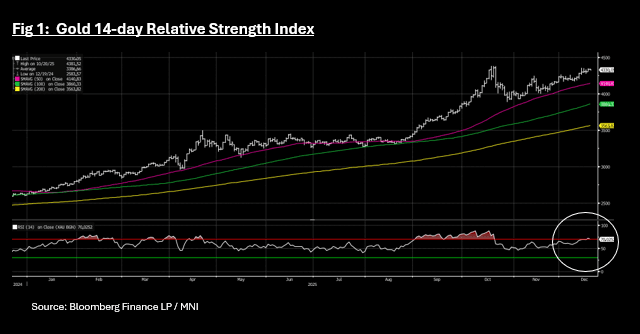

Gold Moderates Despite Equity Weakness, Remains Overbought

- Gold is down moderately today, despite equities remaining under pressure across Asia.

- As markets position ahead of the US CPI Thursday, gold is down -0.19% at US$4,330.17.

- Gold remains above 70 on the 14-day relative strength index, indicating that it is overbought.

- Gold has gained +2.3% in December month to date as equities weaken and Central Banks continue to add to their gold reserves.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 18/12/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 18/12/2025 | 0830/0930 | *** | Riksbank Interest Rate Decison | |

| 18/12/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 18/12/2025 | 1000/1100 | ** | EZ Construction Output | |

| 18/12/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 18/12/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Deposit Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Main Refi Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 18/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 18/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 18/12/2025 | 1330/0830 | * | Payroll employment | |

| 18/12/2025 | 1330/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1345/1445 | ECB Press Conference | ||

| 18/12/2025 | 1445/1545 | ECB Staff Macroeconomic Projections | ||

| 18/12/2025 | 1515/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 18/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 18/12/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 18/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/12/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 18/12/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 18/12/2025 | 2100/1600 | ** | TICS | |

| 19/12/2025 | 2330/0830 | *** | CPI | |

| 19/12/2025 | 0001/0001 | ** | Gfk Monthly Consumer Confidence | |

| 19/12/2025 | 0300/1200 | *** | BOJ Policy Rate Announcement | |

| 19/12/2025 | 0700/0700 | *** | Public Sector Finances | |

| 19/12/2025 | 0700/0800 | ** | PPI | |

| 19/12/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 19/12/2025 | 0700/0800 | ** | Retail Sales | |

| 19/12/2025 | 0700/0700 | *** | Retail Sales | |

| 19/12/2025 | 0745/0845 | ** | PPI | |

| 19/12/2025 | 0800/0900 | ** | Economic Tendency Indicator | |

| 19/12/2025 | 0830/0930 | ECB Wage Tracker | ||

| 19/12/2025 | 0900/1000 | ** | EZ Current Account | |

| 19/12/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 19/12/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 19/12/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 19/12/2025 | 1200/1300 | ECB Cipollone Remarks, Roundtable at Aspen Institute | ||

| 19/12/2025 | 1200/1200 | BOE Market Participants Survey | ||

| 19/12/2025 | 1330/0830 | ** | Retail Trade |