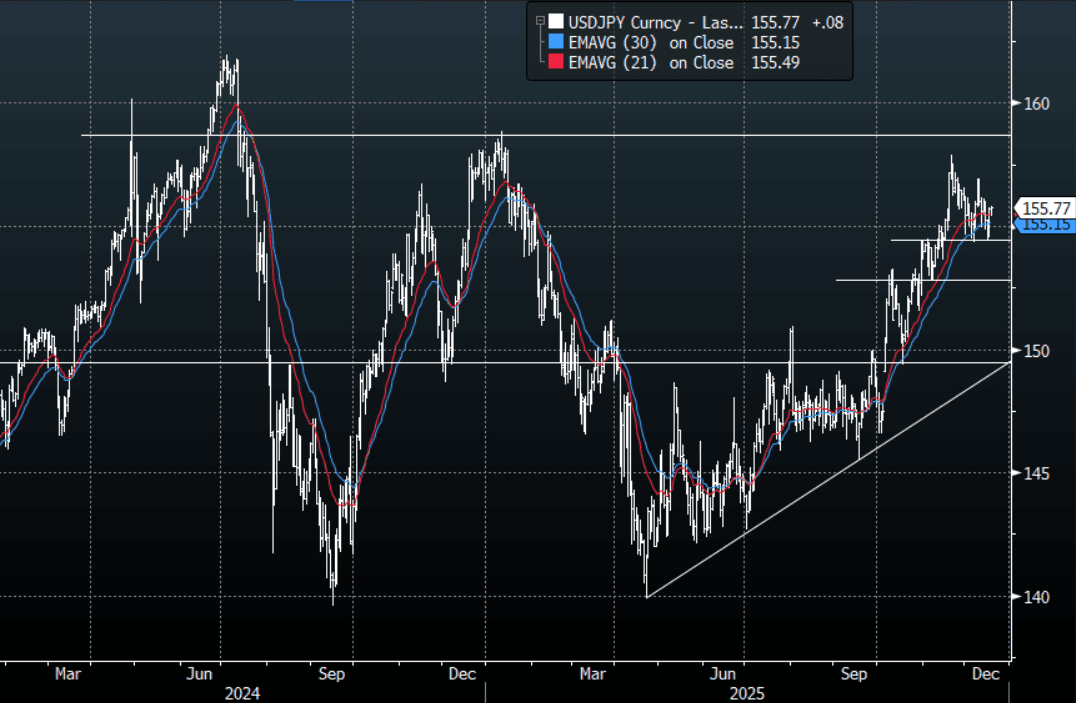

JPY: USD/JPY - Consolidates On A 155 Handle Ahead Of BOJ

The USD/JPY range today has been 155.43 - 155.81 in the Asia-Pac session, it is currently trading around {USDJPY Curncy}. The support around 154.50 proved to be rock solid again yesterday and price then bounced working through the resistance around 155.30 before extending higher aided by the move in oil. The way risk sentiment is quickly souring I am surprised the Yen is trading so weak, especially in the crosses. The market is pricing in a hike by the BOJ tomorrow, for the time being this is keeping the JPY contained and confined to a wider 154.00-157.00 range having capped its upward momentum. Technically USD/JPY is in an uptrend, the first big support is back toward the 152.50-154.50 area. On the day, look for resistance back toward the 156.00-156.30 area initially, support is seen back toward 155.15-45 where demand was seen initially in our session.

- Options : Close significant option expiries for NY cut, based on DTCC data: 157.00($4.15b), 158.00($4.98b). Upcoming Close Strikes : 153.00($2.83b Dec 19), 155.00($2.18b Dec 19), 158.00($1.85b Dec 19) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 105 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

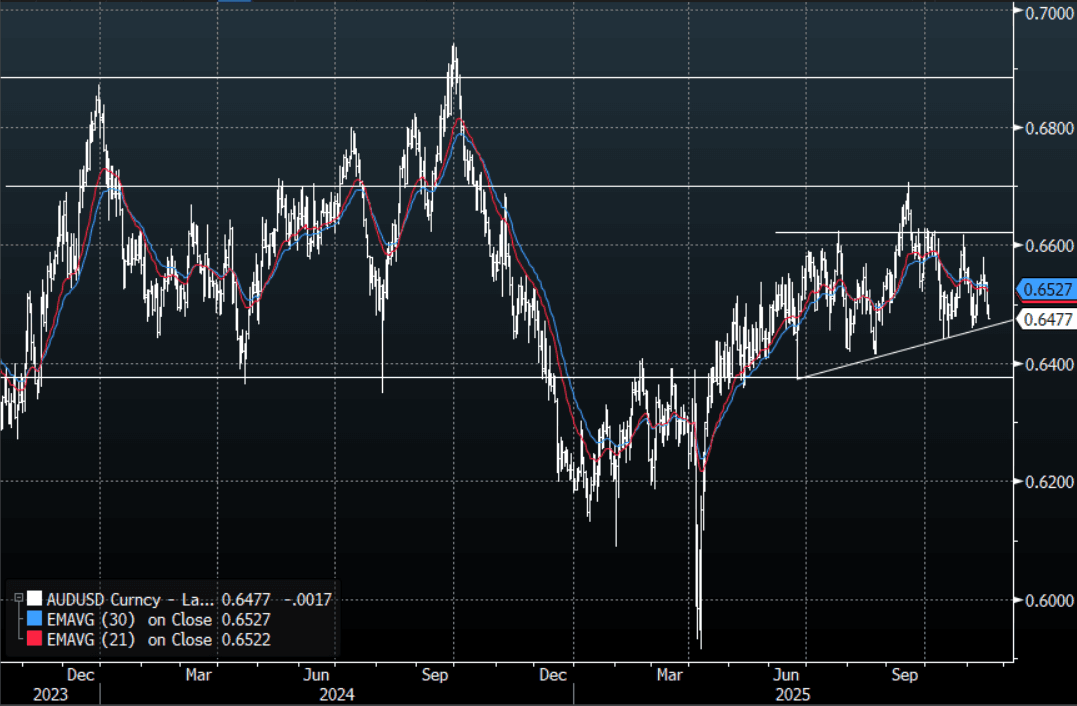

AUD: Asia-Pac: AUD/USD Drifts Lower As Risk-Off Sentiment Grows

The AUD/USD has had a range today of 0.6477 - 0.6499 in the Asia- Pac session, it is currently trading around 0.6480, -0.25%. The AUD/USD has drifted lower in our session being led by the move lower in risk, driven predominantly by the collapse in Crypto. Bitcoin and Crypto continue to lead this leg lower as leverage is being squeezed, Bitcoin below the pivotal $90k area could add to the current market headwinds. The AUD/USD is testing below 0.6500 this morning, some good support back toward 0.6440-0.6460 which has been pretty solid the last couple of months, then 0.6350 below that. It would need this move lower in risk to accelerate and become something more significant to challenge down there I would think.

- MNI AU - RBA: 2-Way Risks, How They Develop Likely To Determine If Hold Prolonged. The November meeting minutes reiterated that the RBA’s central scenario is “in balance” with risks to both the downside and upside. How these risks will develop is likely to determine whether monetary policy stays on hold or rates are cut further and while it is “not yet possible to be confident” about which scenario will materialise, the Board will “remain cautious and data dependent”. With core inflation above target and ongoing signs of a recovery in demand, policy is likely to be on hold in December and into early 2026, depending on the data.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD913m), 0.6600 (AUD729m). Upcoming Close Strikes : 0.6550(AUD2.28b Nov 21) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 47 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

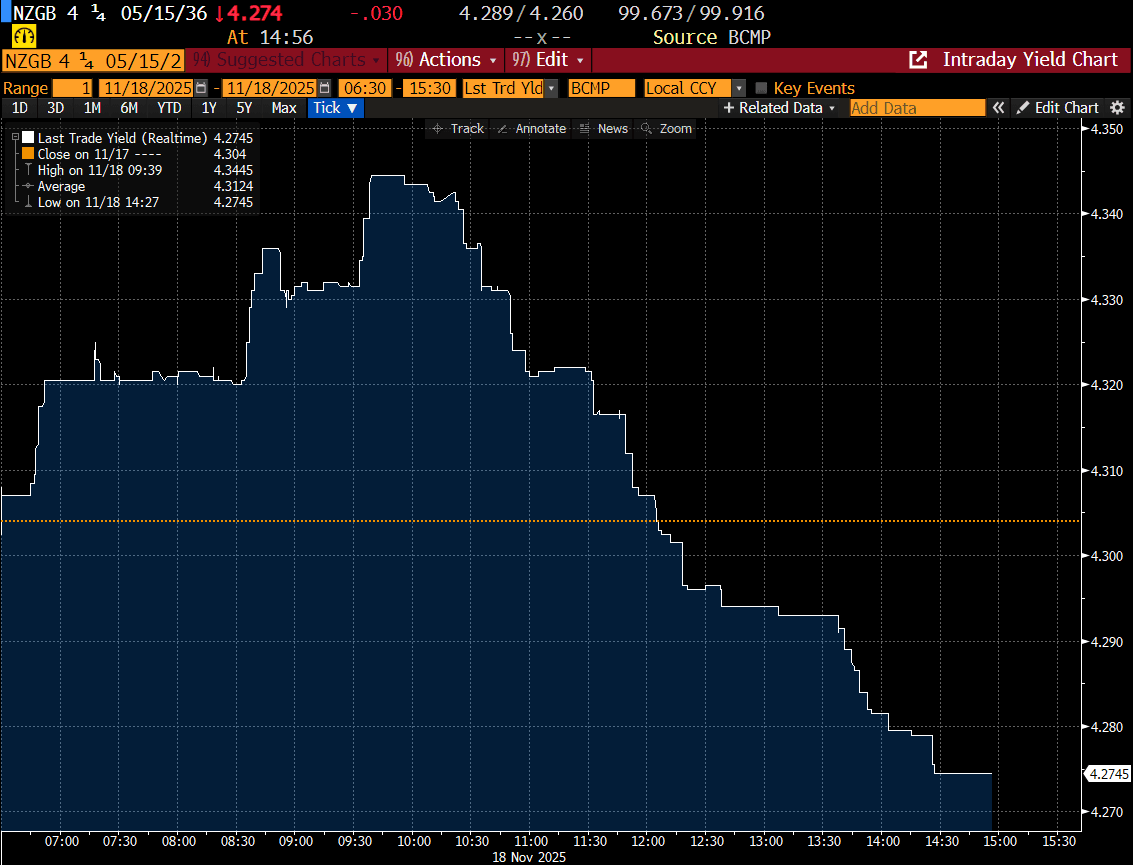

BONDS: NZGBS: May-36 Yield Finishes At Low After Tap

NZGBs closed showing a twist-flattener, with benchmark yields 1bp higher to 3bps lower.

- NZGBs held by international investors increased to 60.3% in October from 59.6% in September.

- RBNZ Business Expectations Survey for Q4 showed the weighted mean 1-year ahead inflation expectation falling to 2.42% from 2.53% in Q4. 2-year declines to 2.39% from 2.64% - BBG

- NZ Treasury issued NZ$6bn of May 2036 nominal NZGB after a syndicated tap. The issue was capped at NZ$6bn, with a total book size at final price guidance at NZ$24.8bn. It was priced at 12bps over the May 2035 nominal bond to yield 4.34%. JLM: ANZ Bank New Zealand, JPMorgan Securities Australia, UBS AG, Australia Branch and Westpac.

- Inflation-adjusted New Zealand existing home sales average price NSA fell 4.2% in October from the same period last year, according to Bloomberg calculations using official data.

- Swap rates closed little changed.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for November, with a cumulative 33bps by February 2026.

- Tomorrow, the local calendar will see PPI data.

Bloomberg Finance LP

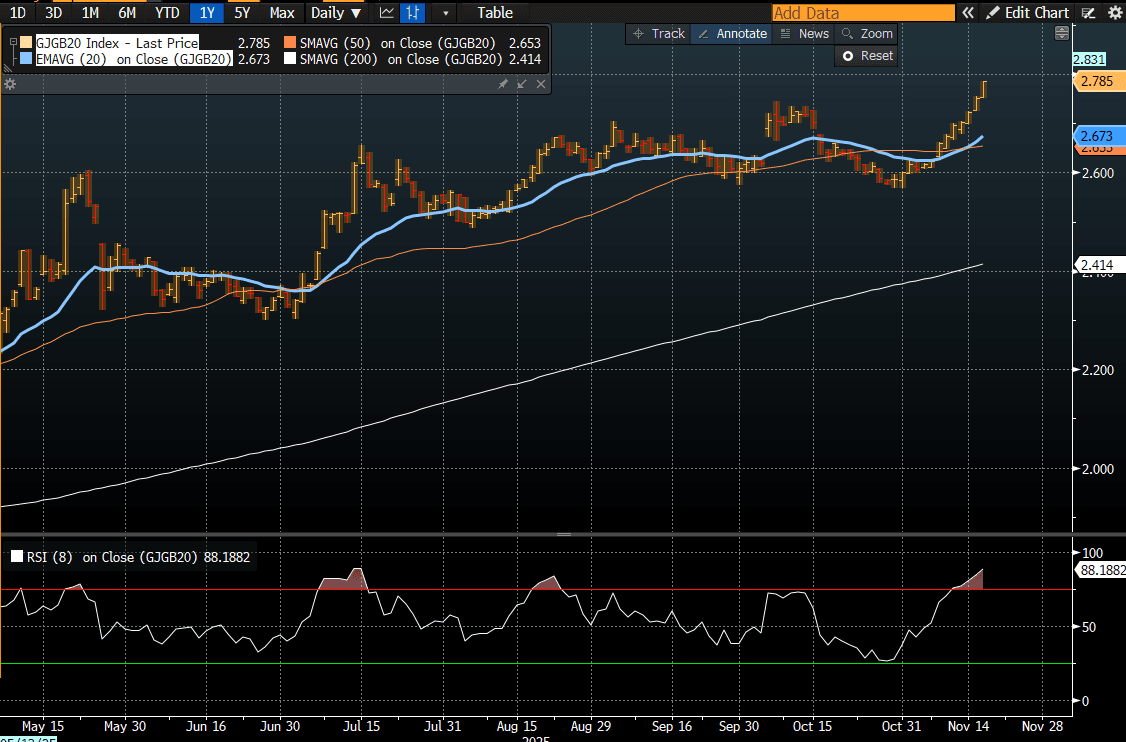

JGBS: Long-End Remains Pressured At Lunch Ahead Of PM/BOJ Meeting

At the Tokyo lunch break, JGB futures are weaker, -9 compared to settlement levels.

- "Japanese Prime Minister Sanae Takaichi is set to meet with Bank of Japan Governor Kazuo Ueda on Tuesday as she mulls support for an economy that shrank over the summer. The two will meet at 3:30 p.m. in Tokyo, according to the prime minister's office. The meeting comes after a report showed the Japanese economy contracted in the three months through September on a US tariff-linked slump in exports and a sharp drop in property buying." - BBG

- Cash US tsys are 1-2bps richer, with a steepening bias, in today's Asia-Pac session.

- Cash JGBs are 1bp richer to 5bps cheaper across benchmarks, with a steeper curve. The benchmark 20-year yield is 3.4bps higher at 2.785%, a fresh cycle high, ahead of tomorrow's supply. (see chart)

- The 20-year JGB is at a similar valuation to last month in terms of the 10/20/30 butterfly.

- Swaps have twist-steepened, with rates 1bp lower to 5bps higher.

Source: Bloomberg Finance LP