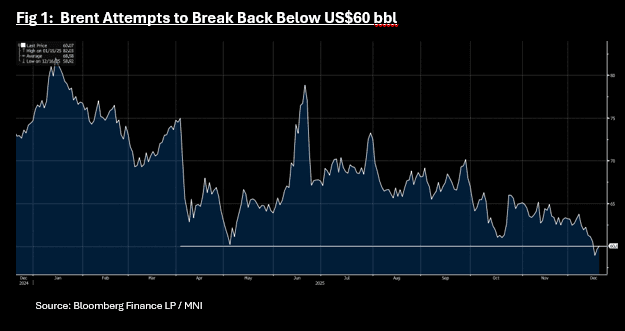

OIL: Oil Moderates with Limited New Venezuela Headlines

- After gains of over 2% yesterday, WTI has given some of those gains back in the Asia trading session. As US President Trump called a press conference from the White House, many expected new announcements on Venezuela and with them not forthcoming, WTI is down -0.28% at US$56.35 bbl.

- Brent is down -1.04% at US$60.06 bbl as it attempts to break back below US$60 bbl having closed below Tuesday.

- Yesterday US President Trump announced a blockade of Venezuela's sanctioned oil flows stating that "Venezuela is completely surrounded by the largest (US) armada ever assembled in the history of South America."

- The rise in prices may be a short term issue as the Venezuelan oil supply is tiny in the context of global oil supply and with supply factors driving prices lower, they will likely reassert themselves in coming days.

- There are also suggestions now that the US is considering targeting Russian President Putin's shadow fleet of oil tankers should the Kremlin not accept a peace deal to end the conflict in Ukraine. This comes as BBG reports a fleet of tankers laden with Russia's oil has expanded of China's east coast following the decline in purchases from India.

- EIA data released overnight shows that US crude inventories declined to 424 million barrels, the second consecutive week of nationwide declines. That drop in stockpiles was partly offset by 249,000 barrels injected into the Strategic Petroleum Reserve. Inventories at Cushing, Oklahoma, declined to 20.9 million barrels, the fifth draw on stocks at the hub in six weeks.(per BBG)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: All Major Markets Down, As Risk Off Grows, Tech Hit Hardest

All the major indices are down in Asia Pac so far today, with tech sensitive plays the worst hit. Japan markets off over 2%, likewise Taiwan, while the South Korean Kospi is down around 3%. Focus remains on the crypto space, where Bitcoin is under 90k, which is fresh lows back to April of this year. Markets will be mindful of deleveraging if we see further downside and spill over to broader risk trends. US equity futures are off, Eminis down close to 0.60%, while Nasdaq futures sit down over 0.750%. Eminis are at levels last seen in mid Oct. The next downside target may be the 100-day EMA near 6586 (we were last around 6654)

- Japan markets are off over 3%, with the NKY 225 testing under 49000. This is an important support area in light of the recent step uptrend. USD/JPY is back under 155.00 amid the risk off mood. Japan is also looking to mend ties with China - via BBG: "Foreign Minister Toshimitsu Motegi told lawmakers on Tuesday that Tokyo has been working on multiple fronts to clarify Takaichi’s remarks, including sending a senior diplomat to Beijing this week. “Our stance is being conveyed clearly at various levels,” Motegi said.

- We also have the meeting later at 3:30pm local time between PM Takaichi and BoJ Governor Ueda.

- In Hong Kong the HSI is off around 1.5%, while the CSI 300 is down a more modest 0.22% at the lunch time break (as is typical for risk off days).

- The Taiex is down over 2%, while the Kospi has fallen by over 3%, continuing its high beta/vol trend of late. This puts the index back under the 4000 level. The other focus point for chip/AI related markets is Nvidia results on Wednesday. Tech is seen as susceptible to further risk off though as this is where we have seen strong outperformance so far in 2025.

- In South East Asia markets are weaker, we are down, but losses are generally more modest, and less than 1% at this stage. In Australia the ASX 200 is down 2%.

AUSSIE BONDS: Risk-Off Drives Bond Rally Ahead Of WPI Tomorrow

ACGBs (YM +4.0 & XM +3.5) are richer and at session highs as risk turns down, led by Bitcoin.

- Cash US tsys are 2-3bps richer, with a steepening bias, in today's Asia-Pac session.

- Cash ACGBs are 4bps richer with the AU-US 10-year yield differential at +32bps.

- Today’s Jun-54 bond auction saw the weighted average yield print 0.18bps through prevailing mids. However, demand weakened dramatically, as reflected by a cover ratio of 2.8500x, down from 4.0533x from the previous auction.

- The AOFM plans to sell A$1000mn of the 2.75% 21 June 2035 bond tomorrow and A$700mn of the 1.25% 21 May 2032 bond on Friday.

- The November meeting minutes reiterated that the RBA's central scenario is "in balance" with risks to both the downside and upside. With core inflation above target and ongoing signs of a recovery in demand, policy is likely to be on hold in December and into early 2026, depending on the data.

- RBA-dated OIS pricing is softer today, showing a 25bp rate cut in December at a 5% probability, with a cumulative 15bps of easing priced by mid-2026.

- The bills strip has bull-flattened, with pricing +3 to +5.

- Tomorrow, the local calendar will see the Wage Price Index and the Westpac Leading Index.

Bloomberg Finance LP

OIL: Crude Unwinds Week’s Gains As Excess Supply Worries Outweigh Geopolitics

Oil has unwound Monday’s gains during today’s APAC session on weaker risk appetite. WTI is down 0.8% to $59.50/bbl, close to the intraday low, and has traded below $60 over the day. Brent is 0.7% lower at $63.74, the day’s trough. While crude has trended lower over November, geopolitical risks have pushed back against market surplus concerns keeping it in a narrow range.

- Conflict is impacting fuel output in Russia and Sudan, while Iran’s redirection of a tanker in the Gulf of Oman into its own waters increases the risk to the significant shipments travelling through the area.

- The grace period before the introduction of sanctions on Russia’s Rosneft and Lukoil ends in a few days and it remains unclear how they will impact the oil majors’ exports and overseas assets driving the discount on Russia’s Urals benchmark to its highest since June 2023, according to Bloomberg. Meanwhile, Ukraine continues to strike ports and refineries.

- With the oversupply situation firmly in focus, inventory data will continue to be important. US industry-based stocks are released later on Tuesday with the official EIA data on Wednesday.

- Both OPEC and non-OPEC have increased output this year and Bank of Montreal is reporting that Canadian oil sands production reached a record in June which is set to rise to 6mbd by 2030.

- China’s product exports were strong in October with gasoline up 11.8% y/y and diesel +55.7% y/y. However YTD they were down 10.3% y/y and 22.7% y/y.

- Later the Fed’s Barr & Barkin, BoE’s Pill & Dhingra, and ECB’s Buch, Elderson, Machado & Tuominen speak. Delayed US IP and final August orders are released as well as ADP weekly employment estimates, November NY Fed services and NAHB housing.