US TSYS: Yields Lower as Equities Struggle

US bond futures were all up marginally today, as equity markets continue to struggle across Asia today. The US 10-Yr is up +02+ at 112-18+, near to the topside resistance from the 20-day EMA of 112-19+.

Cash is strong with the curve lower by up to -1.7bps, with the front end outperforming.

- The 2-Yr is down -1.7bps to 3.468%

- The 5-Yr is down -1.6bps to 3.684%

- The 10-Yr is down -1.2bps to 4.143%

- The 30-Yr is down -0.8bps to 4.82%

Our compilation of sell-side analyst expectations for Thursday's CPI report uses a narrower range of previews - namely, those that included core CPI forecasts to two decimal places or more for the 2-month or Oct and Nov % M/M changes. Within a range of 0.18-0.29% for average core CPI % M/M over October and November, Barclays is at the high end of expectations while NatWest is at the low end. A few summaries below:

- Barclays: Core CPI to average 0.29% M/M across Oct-Nov (two-month cumulative increase of 0.58%), with headline averaging 0.26% M/M (two-month cumulative of 0.52% M/M). "We expect the uptick to be led mainly by core goods prices (led by used car prices rebounding). We estimate services inflation to have also gathered steam, partly led by a rebound in OER CPI following the downside surprise in September."

- Nomura: Core CPI to average 0.245% M/M across Oct-Nov (0.228% Oct, 0.263% Nov); headline 0.24%. "We expect core goods inflation remained strong due to tariff effects as well as higher used vehicle prices.

- Goldman Sachs: Core CPI to average 0.21% M/M across Oct-Nov (0.16% Nov, 0.25% Oct), headline CPI to average 0.20% M/M across Oct-Nov (0.27% Nov, 0.14% Oct). "we have penciled in upward pressure from tariffs on goods categories that are particularly exposed worth +0.08pp on core inflation on average across October and November"

- NatWest: Core CPI to average 0.18% M/M across Oct-Nov (cumulative 0.35%), headline CPI to average 0.20% M/M across Oct-Nov (cumulative 0.40%)."we suspect it will be extremely challenging to try to draw many firm conclusions on this release."

Tonight there is a US$80bn 4-week bill and the US$80bn 8-week bill.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Twist-Steepener, 2/30 YC Back Near Highs, PM/BOJ Meeting Due

JGB futures have clawed back to unchanged versus settlement levels.

- With the local calendar light, the domestic market, out to the futures-linked 7-year, has benefited from general global risk-off sentiment.

- "Japanese Prime Minister Sanae Takaichi is set to meet with Bank of Japan Governor Kazuo Ueda on Tuesday as she mulls support for an economy that shrank over the summer. The two will meet at 3:30 p.m. in Tokyo, according to the prime minister's office. - BBG

- Cash US tsys are 2-3bps richer in today's Asia-Pac session.

- JGBs have twist-steepened in today's session, with cash JGBs 1bp richer to 7bps cheaper across benchmarks. The benchmark 20-year yield is 3.6bps higher at 2.786% after setting a fresh cycle high of 2.816% ahead of tomorrow's supply.

- "A "sell Japan" trend is likely to persist across equities, bonds and the yen unless Tokyo de-escalates its ongoing diplomatic spat with China, according to Tomo Kinoshita, global market strategist at Invesco." – BBG

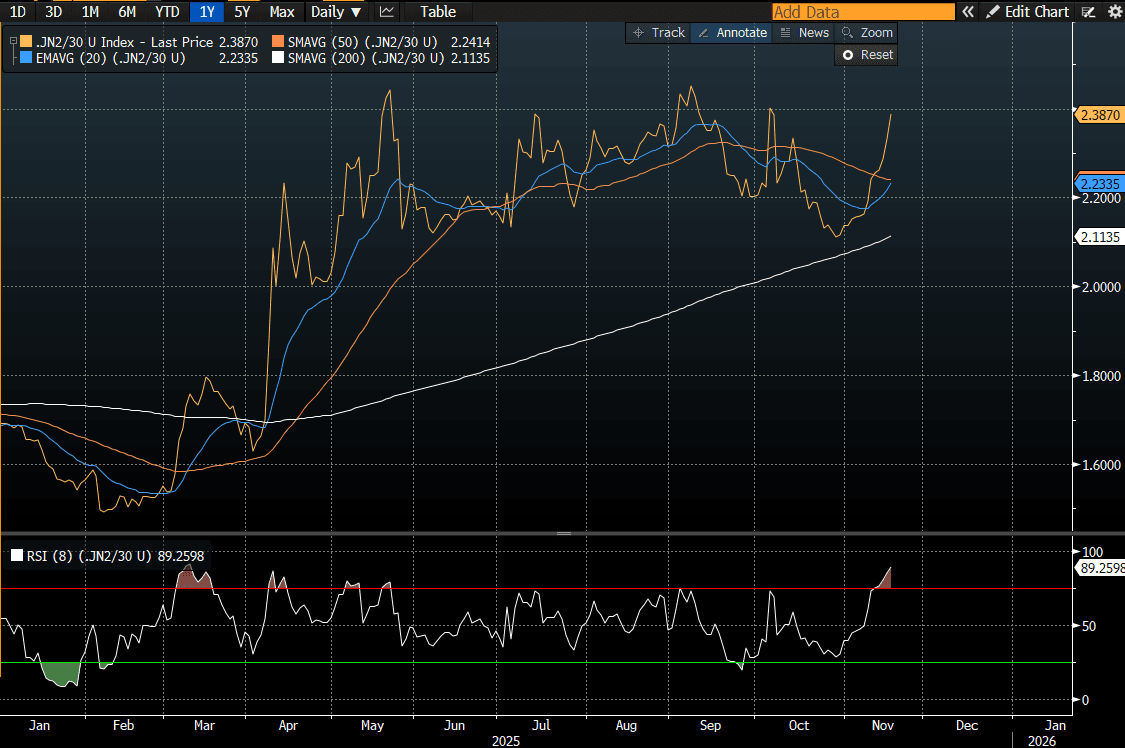

- Today’s move also places the 2/30 curve within striking distance of its recent high. (see chart)

- Swaps have twist-steepened, with rates 1bp lower to 4bps higher.

- Tomorrow, the local calendar will see Trade Balance and Core Machine Orders data.

Source: Bloomberg Finance LP

GOLD: Weaker, Eyeing Sub $4000, Risk Off Doesn't Aid Sentiment

Gold is back close to $4010, off a further 0.90% so far today. the risk off evident in the crypto space and in equity markets has done little to aid gold safe haven related demand. Some offset is coming from a higher USD (albeit with mixed trends today, higher against higher beta plays, but safe havens, JPY and CHF are rising), as Fed easing expectations remain uncertain. A break under $4000 could bring the 50-day EMA support point into play, which comes in at $3927.5. Initial resistance is at $4264.7.

- FOMC members appear split between believing further easing is needed to restart the labour market and holding as inflation remains above target. The Fed’s Waller noted earlier today that the focus should be on jobs data and not inflation and that the fiscal position is not sustainable.

- US real 10yr yields remain elevated compared to recent history, last at 1.85% (recent lows were under 1.70%).

- Structural support for gold still appears evident from an asset allocation standpoint. Via BBG: "China added an estimated 15 tons of gold to its forex reserves in September as central banks accelerated their purchases of bullion after a seasonal summer lull, according to Goldman Sachs Group."

US TSYS: Risk-Off Pushes Yields Lower

TYZ5 is dealing at 112-26, -0-05+ from closing levels in today's Asia-Pac session, as risk turns down, led by Bitcoin.

- Stocks have extended Monday's weakness in today’s Asia-Pac session. Chip makers led declines yesterday, followed by financials. Investors all of a sudden appear wary of lofty tech valuations, ahead of Nvidia Corp.’s earnings and a key US jobs report later this week.

- Cash US tsys are 2-3bps richer, with a steepening bias, in today's Asia-Pac session.

- However, JGBs have bear-steepened in today's session. "A “sell Japan” trend is likely to persist across equities, bonds and the yen unless Tokyo de-escalates its ongoing diplomatic spat with China, according to Tomo Kinoshita, global market strategist at Invesco." - BBG

- Tuesday's data schedule is light, with markets gearing up for the now-much-delayed September NFP print due this Thursday.