MNI EUROPEAN OPEN: Japan FX Rhetoric Picks Up

EXECUTIVE SUMMARY

- BLS RECALLS STAFF TO READY SEPTEMBER CPI REPORT BY MONTH'S END - BBG

- GERMANY'S TOP ECONOMIST CHARTS PATH OUT OF EUROPE'S CRISIS - NYT

- JAPAN FINANCE MINISTER RAMPS UP WARNING AFTER FURTHER YEN FALL - BBG

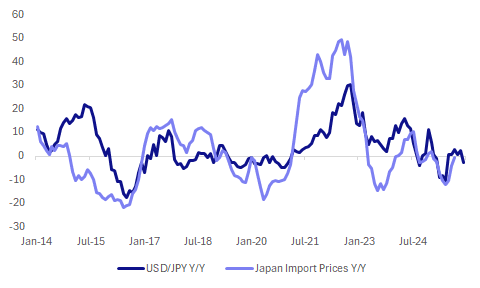

- JAPAN SEPT CGPI RISES 2.7% Y/Y; IMPORT PRICE DROPS - MNI BRIEF

- FORMER SENIOR RBA OFFICIAL SHARES CASH RATE OUTLOOK - MNI INTERVIEW

Fig 1: Japan Import Prices & USD/JPY Y/Y (Assuming Current Spot Levels Prevail To Yr End)

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

JOBS (BBG): "Employers scaled back hiring at the softest pace in a year in September, a poll conducted by the Recruitment & Employment Confederation and KPMG found. Other metrics including vacancies and the number of jobseekers showed signs of stabilizing. "

EU

GERMANY (NYT): "Joachim Nagel, the president of Germany’s central bank, warned against “complacency” in European capitals over tariffs, competition with China and attacks on institutions. Central bank chiefs are cautious by nature, mindful that their words can move markets and influence politics."

DEBT (MNI BRIEF): The European Commission told France Thursday that "substantial consolidation measures" would be needed in its 2026 budget if the country is to stick to the EU spending commitments it made in its medium-term fiscal plan.

FRANCE (BBG): “- The political power players aren’t the only ones jockeying to shape the shifting balance of power in a turbulent France.”

FINLAND (BBG): "The US and Finland agreed to a deal that would see Washington aquire as many as 11 icebreakers to kickstart the expansion of the American fleet as great-power rivalry is heating up in the Arctic."

US

FED (MNI): The Federal Reserve’s price stability goal faces significant risks and, given uncertainty about the economic outlook and the state of the Fed's labor market goal, a cautious approach to rate cuts will help the central bank balance risks to both sides of the dual mandate goals, Fed Governor Michael Barr said Thursday.

FED (MNI POLICY): The U.S. government data blackout will not prevent the Federal Reserve from continuing to lower interest rates as soon as this month and possibly again in December in response to signs of weakening in the labor market and inflation that is less acute than officials had feared.

INFLATION (BBG): "The Bureau of Labor Statistics has recalled staff to prepare a key inflation report that is necessary to calculate the size of next year’s Social Security checks, according to a Labor Department official with knowledge of the matter."

OTHER

JAPAN (MNI BRIEF): Japan’s corporate goods price index (CGPI) rose 2.7% y/y in September, unchanged from August’s unrevised pace, while import prices declined for an eighth consecutive month, Bank of Japan data showed Friday.

JAPAN (BBG): "Japan’s Finance Minister Katsunobu Kato stepped up his warnings over yen movements, after the currency hit a fresh eight-month low against the dollar early Friday, despite efforts by the ruling party’s new leader to calm market concerns."

AUSTRALIA (MNI INTERVIEW): A former senior RBA official shares his cash rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

CANADA (MNI INTERVIEW): Canadian truckers are selling their rigs and filing for bankruptcy as the U.S. trade war creates the worst market in four decades with damage spreading through the whole economy, the head of the industry's lobby group told MNI, suggesting one of the central bank's concerns about the downturn's scale is being realized.

MIDDLE EAST (BBG): "Israel’s government approved a deal that will see Hamas release any remaining hostages held in Gaza in exchange for more than 2,000 prisoners, another major step toward fulfilling the terms of a peace agreement and ending the two sides’ bloody conflict."

CHINA

PRICE COMPETITION (SECURITIES TIMES): “Chinese authorities have proposed a series of targeted measures to curb disorderly price competition, including average cost investigations, stronger price supervision and standardised bidding practices, Securities Times reported, citing a joint announcement by the National Development and Reform Commission (NDRC) and the State Administration for Market Regulation (SAMR) on Thursday.”

CONSUMPTION (TAX ADMINISTRATION): “The average daily sales revenue of consumption sectors nationwide increased by 4.5% y/y during the Oct 1-8 Golden Week, among which goods and services sales rose by 3.9% and 7.6% y/y, China National Radio reported citing value-added tax invoice data by the State Administration of Taxation.”

CNH (SECURITIES DAILY): “The Hong Kong Monetary Authority (HKMA) has launched a Renminbi (RMB) Business Facility from Oct 9 to support banks in providing yuan loans to corporates, Securities Daily reported.”

MNI: PBOC Net Drains CNY191 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY409 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY191 billion after offsetting maturities of CNY600 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4323% at 09:48 am local time from the close of 1.5073% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 47 on Friday, compared with the close of 48 on Thursday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1048 Fri; -0.02% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1048 on Friday, compared with 7.1102 set on Thursday. The fixing was estimated at 7.1338 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND SEP BUSINESSNZ MANUFACTURING PMI 49.9; PRIOR 49.9

JAPAN SEP PPI Y/Y 2.7%; MEDIAN 2.5%; PRIOR 2.7%

JAPAN SEP BANK LENDING INCL TURST Y/Y 3.8%; PRIOR 3.5%

SOUTH KOREA SEP FX RESERVES $422.02BN; PRIOR $416.29BN

MARKETS

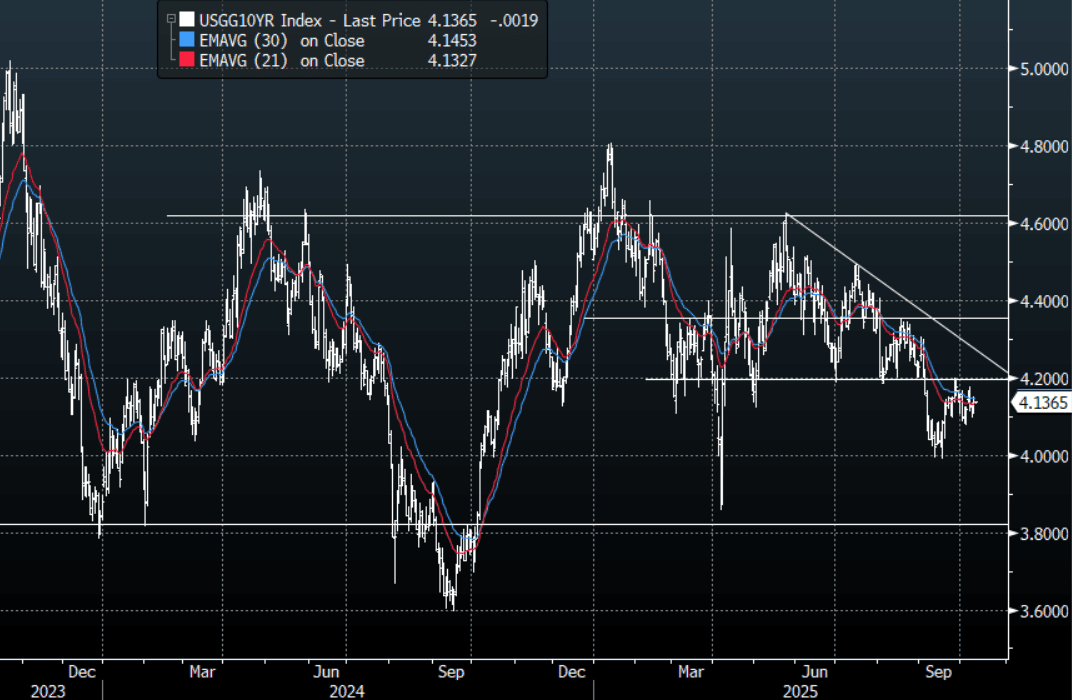

US TSYS: Asia-Pac: Front-End Yields Drift Slightly Lower

The TYZ5 range has been 112-16+ to 112-18+ during the Asia-Pacific session. It last changed hands at 112-18, up 0-02+ from the previous close.

- 10-Year yields continue to consolidate just above 4.10% but remain subdued below 4.20% as the market works through the US shutdown. I suspect buyers continue to be around the 4.20% area initially and look to fade any move higher for now.

- The US 10-year yield is trading around 4.137%.

- The US 2-year yield has edged lower trading 3.588%, down 0.01 from its close.

- “LABOR DEPT'S BLS AIMING TO RELEASE SEPT CPI DATA BY MONTH'S END” - BBG

With Labour data at a premium after NFP was delayed, “Neil Dutta, Head of Economics at @RenMacLLC, told the Schwab Network that there could be fewer construction workers employed, as homebuilders are "a little bit bloated in terms of their labor relative to what they're doing." He said the job losses can be substantial, adding that the slight drop in mortgage rates "hasn't really stoked" homebuyer activity.” - Schwab Network on X.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

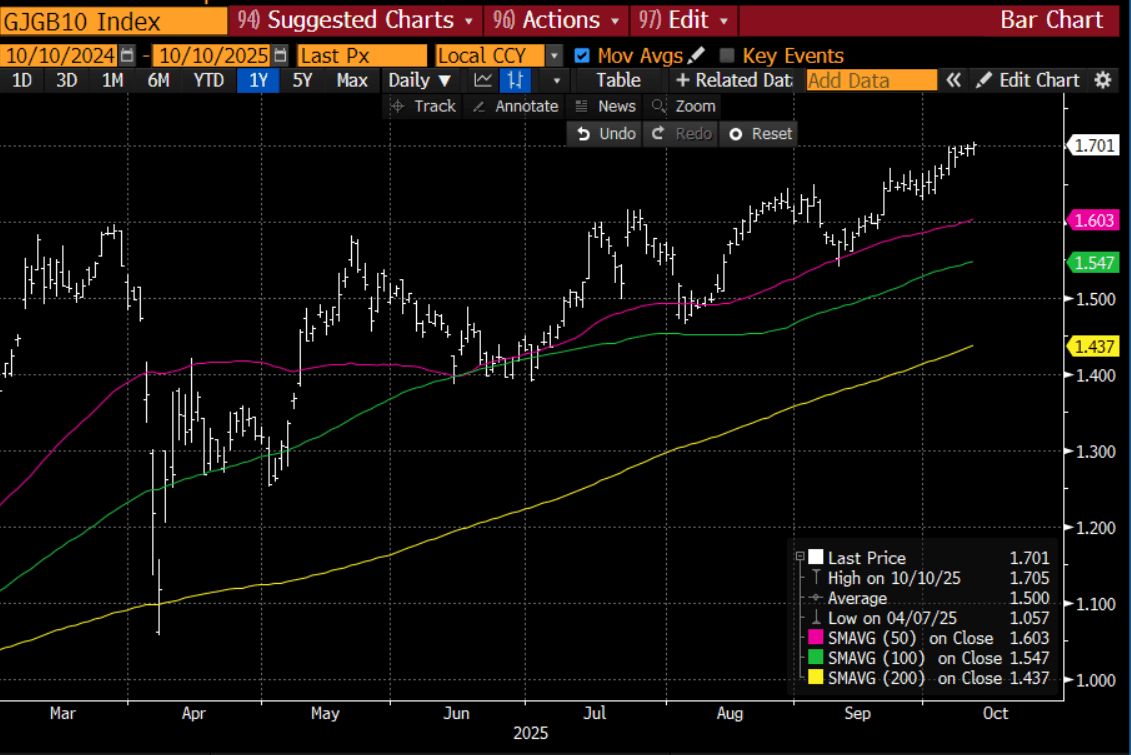

JGBS: Slightly Mixed But 10YY At Highest Since 2008

JGB futures are little changed, +1 compared to the settlement levels.

- Cash JGBs have continued to largely look past today's price data, with yields 0.5bp higher to 1.5bp richer across benchmarks.

- Nevertheless, the 10-year has pushed to a fresh cycle high of 1.705%, its highest yield since 2008. (See chart)

- Earlier Japan PPI data was a touch above forecasts. Moreover, disinflation from the import side continues to dissipate, which will be a BoJ watch point, particularly given renewed yen weakness. It is arguably too soon, though, to push the central bank to tighten rates.

- The benchmark 30-year yield is down 0.8bps at 3.178%, after trading in a 3.15-3.35% range this week. Even if the BOJ refrains from further rate hikes this year - with only a small chance currently priced in - we doubt long-dated JGBs would rally meaningfully, as such a move would likely be seen as a delay in tightening rather than its abandonment.

- Swap rates are, however, 1-3bps richer, with tighter swap spreads.

- On Monday, the local market will be closed.

Bloomberg Finance LP

AUSSIE BONDS: Cheaper, AU-US 10Y Diff Back Near Wides, Issuance Light Next Week

ACGBs (YM -3.5 & XM -2.5) are weaker after trading in narrow ranges in today’s session.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at +24bps. At +24bps, the differential is near the top of the ±30bps range that has prevailed since November 2022.

- Going forward, a move toward the top of the range would likely prompt international investors and traders to initiate differential-narrowing trades. Such flows would tend to be self-reinforcing so long as it aligned with the direction of the AU–US 1Y3M spread.

- The bills strip is -3 to -4 across contacts.

- RBA-dated OIS pricing shows a 25bp rate cut in November as a 36% probability, with a cumulative 13bps of easing priced by year-end.

- Next week, the AOFM plans to sell A$400mn of the 3.25% 21 June 2039 bond on Tuesday, A$800mn of the 4.25% 21 December 2035 bond on Wednesday and A$800mn of the 1.00% 21 December 2030 bond on Friday.

- Issuance is below the typical size in fiscal 2026 of about A$2.2bn for a second straight week. This is consistent with the recently reported budget deficit for fiscal 2025 of A$10bn, less than its forecast of A$27.9bn earlier this year.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

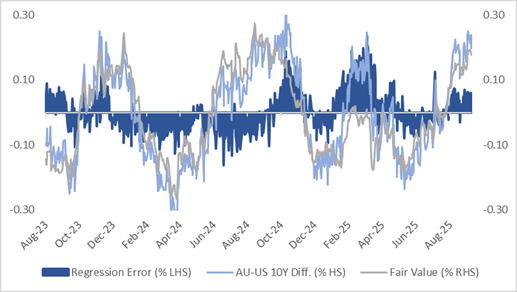

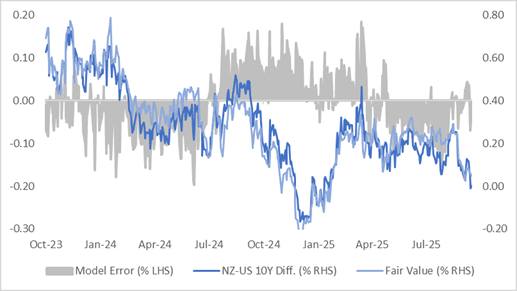

BONDS: Post-RBNZ Rally Stalls Ahead Of W/E

NZGBs closed 2-3bps cheaper, with the NZ-US 10-year differential 1bp wider at flat.

- At this level, the differential sits in the lower half of the -20bps to +40bps range observed year to date. For context, it was around +30bps in mid-September, prior to the release of much weaker-than-expected Q2 NZ GDP data.

- A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the current differential is about 6bps below its estimated fair value of +8bps. (See chart)

- Swap rates closed 2-3bps higher. As noted previously, the 30bp decline in the 2-year rate since the release of Q2 GDP in late September appeared increasingly over-extended, with the rate approaching channel resistance. A period of consolidation, therefore, looks more likely unless another negative economic shock emerges.

- “NZ Finance Minister Nicola Willis expressed optimism about the country’s economy, saying she was confident it had returned to growth last quarter as interest-rate cuts help boost sentiment.”- BBG

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for November, with a cumulative 33bps by February 2026.

- On Monday, the local calendar will see Performance Services Index and Net Migration data.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

FOREX: Asia FX Wrap - USD: Can The Bounce Extend?

The BBDXY has had a range of 1214.52 - 1216.07 in the Asia-Pac session; it is currently trading around 1215, -0.10%. The USD has given back a little of its overnight gains in our session after the PBOC delivered a much stronger fix at 7.1048. The 1215-1225 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. The weaker hands may be folding but I suspect we would need to do some work before the market can call a low for the USD. Longer term accounts could potentially look to fade this squeeze as they increase hedging ratios.

- EUR/USD - Asian range 1.1556 - 1.1571, Asia is currently trading 1.1570. The pair extended its retracement after breaking below 1.1600 overnight. Price is probing its first support around the 1.1550 area; a break through here is needed to signal a deeper correction towards the more important 1.1200-1.1300 support.

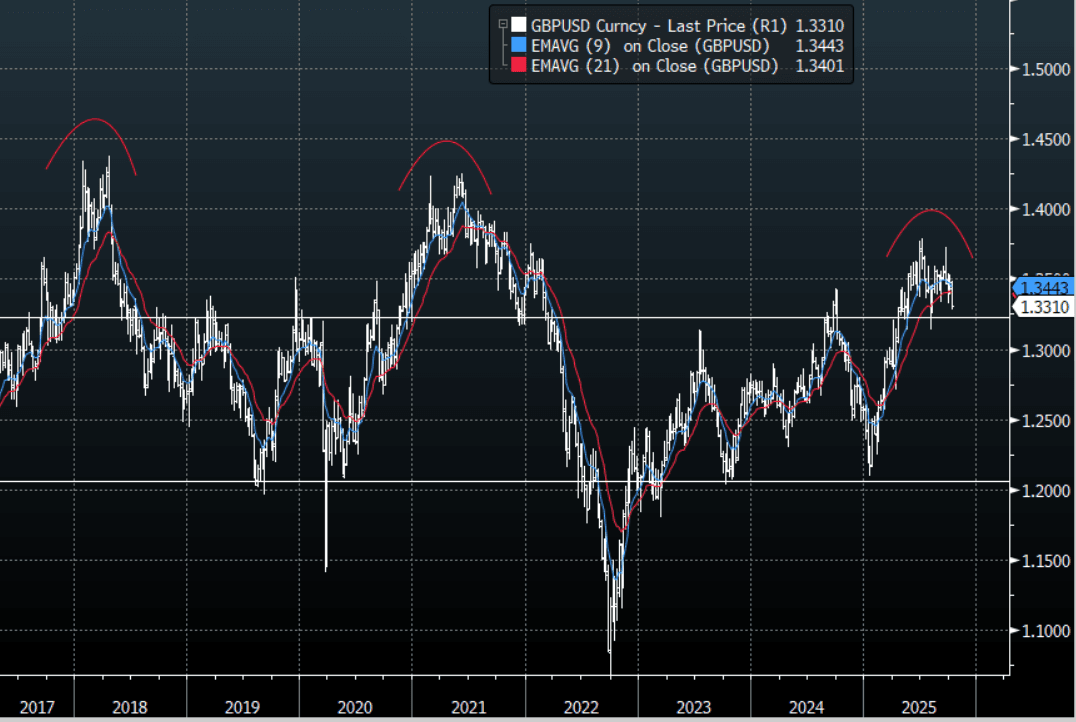

- GBP/USD - Asian range 1.3293 - 1.3309, Asia is currently dealing around 1.3300. The pair continues to be capped on any move back towards the 1.3500 area. Cable looks to be breaking its recent support this could potentially signal a deeper move lower. Should this support give way the next support is around 1.3150, below this support and it could signal a potential interim top in the pair. See Graph Below.

- USD/CNH - Asian range 7.1288 - 7.1392, the USD/CNY fix printed lower at 7.1055, Asia is currently dealing around 7.1310. The area around 7.1500/1600 has proved to be solid resistance and with the PBOC managing the fix lower, it looks likely we could consolidate 7.09-7.16 for the moment.

- Cross asset : SPX +0.15%, Gold $3985, US 10-Year 4.137%, BBDXY 1215, Crude Oil $61.59

- Data/Events : Italy Industrial Production. Asia FX Wrap - USD Can The Bounce Extend

Fig 1: GBP/USD Spot Weekly Chart

Source: Bloomberg Finance L.P./MNI

JPY: Asia-Pac: USD/JPY Momentum Higher Stalls, FinMin Fx Jawboning Firms

The USD/JPY range has been 152.64 - 153.27 in the Asia-Pac session, it is currently trading around 152.75, -0.20%. The pair dipped overnight on Takaichi pushing back on a weaker JPY being part of her platform; it was very short-lived though. The market is doing some work around the 153.00 area. Having come a long way very quickly we could have some pullbacks but I suspect dips will now be supported as we begin a new leg higher, with the focus ultimately back toward the 155-160 area.

- Intervention risks remain a focus. FinMin Kato stated today they were seeing one-sided, rapid moves in FX market. Such remarks weren't used on Tuesday (focus was on closely watching excessive moves, key for FX to moves with fundamentals when Kato spoke then). Still, we haven't seen remarks like deeply concerned about FX moves, or we will take appropriate action if FX moves excessively, which could signal greater interventon risks.

- MNI Policy believes the Yen Fall is Unlikely To Drive Swift Japanese Action. The yen’s slide to an eight-month low against the dollar is unlikely to prompt a rate hike or Japanese authorities to intervene in FX markets immediately, as the weaker currency helps mitigate impacts of U.S. trade policy on exporters – a key driver of the economy, MNI understands.

- MNI on Japan Data - PPI Above Forecast, But Suggests Steady CPI Trend : It rose 0.3%m/m (0.1% was expected and -0.2% was prior), while in y/y terms we rose 2.7%, (2.5% was forecast). This leaves the y/y outcome unchanged on the August outcome. At face value, it is consistent with a steady, albeit still elevated inflation backdrop.

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 150.00($986m Oct 15), 151.50($905m Oct 15) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: Bloomberg Finance L.P./MNI

AUD: Asia-Pac - AUD Drifts Higher, 0.6625 Resistance Holding

The AUD/USD has had a range of 0.6552 - 0.6570 in the Asia- Pac session, it is currently trading around 0.6565, +0.20%. The USD has drifted lower in our session after the PBOC delivered a much stronger fix at 7.1048. The AUD could not break above the 0.6625 resistance overnight and fell away pretty easily from there as the USD built on its recent gains. While AUD/USD remains below 0.6625/50 I suspect the risk remains skewed to the down side and sellers will fade bounces initially. First support is back toward 0.6500 but a break below here would signal a deeper correction lower and could see the move accelerate.

- The USD move is beginning to challenge a market that is short but we are approaching some pivotal levels and suspect longer-term investors might see this bounce as an opportunity to fade as weaker hands are forced out.

- Bloomberg reported that Governor Michele Bullock said “Australia’s economy is in a “pretty good spot” with inflation inside the central bank’s 2%-3% target band and the labor market still tight.” speaking in Canberra today.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6545(AUD657m). Upcoming Close Strikes : 0.6500(AUD1.01b Oct 14), 0.6600(AUD943m Oct 14), 0.6650(AUD880m Oct 14) - BBG

- AUD/JPY - Asia-Pac range 100.23 - 100.50, Asia is trading around 100.45. The pair has surged higher for good reason on the election outcome. It has extended its move higher and is looking to build on its break above 100. Dips should now be supported as the focus now turns toward 102.50 and then the 105.00 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

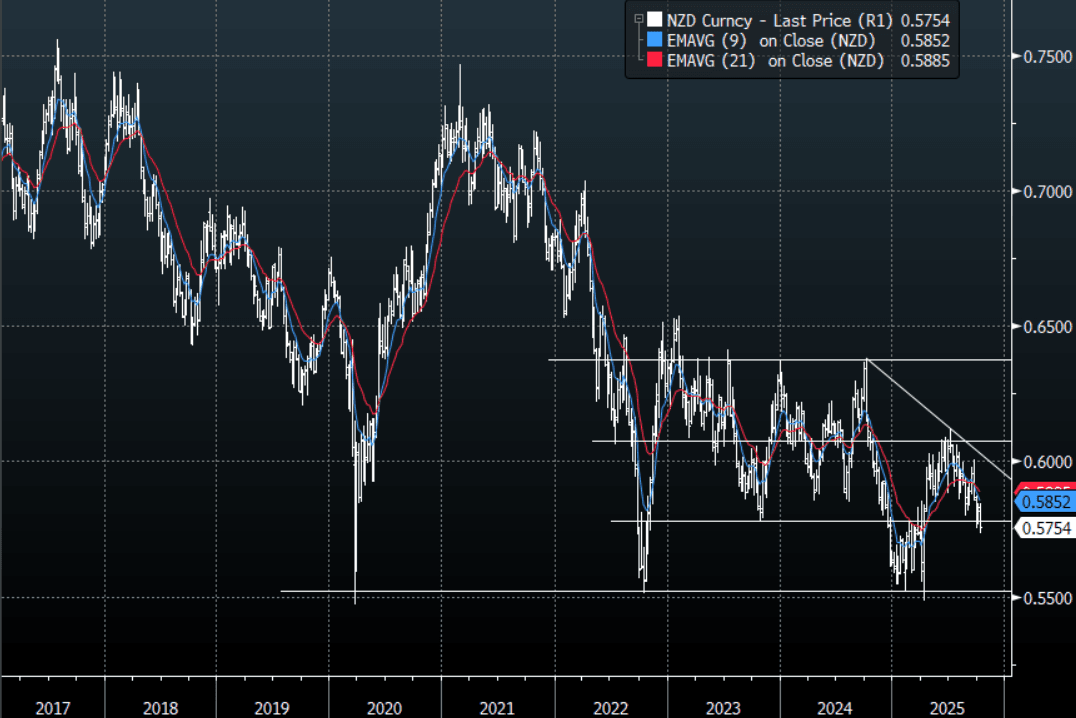

NZD: Asia-Pac: NZD/USD Drifts Higher Helped By Strong CNY Fix

The NZD/USD had a range of 0.5742 - 0.5757 in the Asia-Pac session, going into the London open trading around 0.5755, +0.15%. of 0.6552 - 0.6570 in the Asia- Pac session, it is currently trading around 0.6565, +0.20%. The USD has drifted lower in our session after the PBOC delivered a much stronger fix at 7.1048. The NZD ran into solid supply back toward 0.5800 overnight and when the USD began to build on its gains the NZD fell away very quickly challenging the RBNZ lows. The NZD remains one of the stand out vehicles to express a short, you just have to decide what against. Rallies should now be faded while below 0.5800/0.5850, the market will be looking for a potential move back towards the 0.5500/0.5600 area.

- "NZ'S WILLIS: FORECASTS REMAIN THAT ECONOMY WILL RECOVER IN 3Q, BUDGET SURPLUS IN 2028 REMAINS A ‘FISCAL GOAL’, CONFIDENT NZ’S ECONOMIC GROWTH WILL ACCELERATE IN Q4" - BBG

- "NZ'S WILLIS: NOT PLANNING ANY MAJOR ASSET SALES, WILL LOOK TO USE BALANCE SHEET TO FUND PROJECTS" - BBG

- "NZ'S WILLIS: ECONOMY DOESN'T NEED A FISCAL STIMULUS, ECONOMIC STIMULUS IS COMING FROM MONETARY POLICY" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5850(NZD300m Oct 14) - BBG

- AUD/NZD range for the session has been 1.1401 - 1.1417, currently trading around 1.1415. The Cross surged back above 1.1400 on the surprise 50bps cut. I continue to feel the cross should do some work in the 1.1400/1.1500 area. A clear sustained break above 1.15/1.16 resistance and the market will begin to think about levels back towards 1.2000 and above. Dips back toward 1.1200 should be a good place to start buying again if seen.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Tech Weighed By China Curbs, HSTECH Back Close To 20-day EMA

Most Asia Pac markets are lower, with tech headwinds weighing. This reflects broader global moves (with major indices down in cash trade on Thursday) but also concerns around China export controls in the tech space. Given how bullish sentiment has been recently, markets may be needing fresh catalysts to continue the recent rally at its heady pace. US futures sit touch higher, with Eminis last around 6789, just off record highs above 6812.

- The CSI 300 index is off around 1.1% as we approach the lunchtime break. Recent cycle highs have been above 4726, while we last tracked near 4659. The 20-day EMA support point is back around 4547, with dips to this zone supported since early July.

- BBG notes: "Batteries and some materials-related stocks lead declines after China said it would impose export controls on some lithium batteries, critical materials, and related technology and equipment" These announcements followed yesterday's earlier rare earth export controls. Valuation concerns also linger.

- The HSI is off around 1% as well, while the HSTECH is down over 2.3%, tracking lower for the fifth straight session. We are no back close to the 20-day EMA (6294 versus 6311 current levels). The RSI (14) has corrected from overbought conditions, back to 54.

- Japan markets are weaker. The Topix down 1.7%, the MKY 225 off 1%. The uptrend in USD/JPY has stalled somewhat (back under 153.00), verbal rhetoric from the FinMin picked up a touch. Again, these markets are correcting from overbought levels from a technical standpoint.

- South Korea is bucking these trends, up 1.25% for the Kospi, as onshore markets return after the recent break. Chip/AI related firms like Samsung surged at the open.

- In South East Asia, most markets are down but only modestly. The exception is Thailand, which is off 1.9% and putting the SET back under 1300. BBG notes: "Delta Electronics shares slide after the stock exchange imposes market surveillance measures following their record-breaking rally.".

COMMODITIES: Gold Softer But Bull Cycle Intact, Oil Range Bound

Gold is softer, but above Thursday lows at this stage, as sentiment turns a little more cautious post the recent surge through $4000. We are still up +2% for the week, tracking higher for the 10th straight week (spot bullion was last near $3964). Oil benchmarks are little changed, last at $65/bbl for Brent and $61.40/bbl for WTI. We are tracking close to 1% firmer for the week, but this followed last week's near 8% fall. Some support for oil has been evident following a more cautious OPEC November output increase and US product drawdowns.

- For gold, the recent correction from highs of $4059.3, looks to be profit taking/technical correction. Such flows may have been encouraged by the recent Israel/Hama ceasefire as well (lowering geopolitical tensions).

- Via DJ, the debasement theme remains key one though: "The gold rally this year signals increasing distrust in the existing fiscal and monetary order, says Ajay Rajadhyaksha, Barclays global chairman of research, in a note. "

- Even with a softer USD backdrop so far today, gold is still tracking lower, which also points to positioning/momentum driving price shifts in the near term.

- Gold is still well above its 20-day EMA (last around $3831), while a fresh test above $4000 may see sights set on $4074.54, a Fibonacci projection.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 10/10/2025 | 0600/0800 | *** | CPI Norway | |

| 10/10/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/10/2025 | 0900/1100 | * | Industrial Production | |

| 10/10/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 10/10/2025 | 1230/0830 | *** | Labour Force Survey | |

| 10/10/2025 | 1230/0830 | *** | Labour Force Survey | |

| 10/10/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 10/10/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 10/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/10/2025 | 1700/1300 | St Louis Fed's Alberto Musalem | ||

| 10/10/2025 | 1800/1400 | ** | Treasury Budget |