MNI EUROPEAN OPEN: AUD & Local Yields Surge Post CPI Beat

EXECUTIVE SUMMARY

- TRUMP EXPECTS LOWER FENTANYL TARIFF, NVIDIA TALKS WITH XI - BBG

- BESSENT CALLS ON JAPAN TO GIVE BOJ SPACE TO FIGHT INFLATION - BBG

- ADP SEES TEPID JOBS RECOVERY IN NEW WEEKLY REPORT - MNI BRIEF

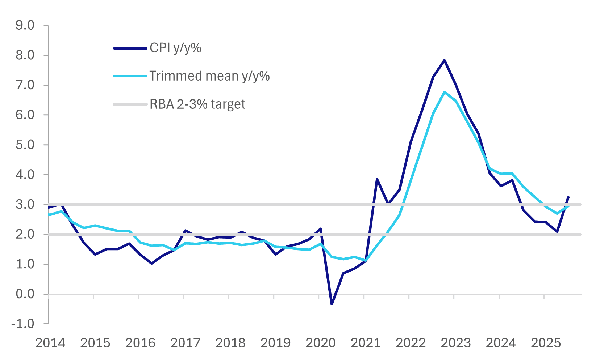

- AUSSIE Q3 CPI PRINTS HIGHER THAN EXPECTED - MNI BRIEF

Fig 1: Australian CPI Pressures Firmer In Q3

Source: MNI - Market News/LSEG

EU

EU (POLITICO): “The European Parliament’s four centrist groups are to demand Commission President Ursula von der Leyen make major changes to her plan for the EU’s next seven-year budget, according to the draft of a letter seen by POLITICO.”

NETHERLANDS (DUTCHNEWS): “the final two opinion polls suggest Geert Wilders’ far-right PVV is faltering while the progressive-liberal D66 has surged into the top three. The Verian poll by EenVandaag still puts the PVV in the lead but with 29 seats, down five in the last week and four ahead of GroenLinks-PvdA, who are unchanged on 25. D66 are in third place after rising eight seats to 24. The Christian Democrats (CDA) drop four seats to 19 while the right-wing liberal VVD are up one on 16.”

NETHERLANDS (POLITICO): “Undecided voters likely to play a decisive role. According to Ipsos I&O, about 13 percent of voters are undecided, but even those who indicated a preference are still highly uncommitted; only 26 percent of those interviewed were sure of their choices.”

US

US/CHINA (BBG): “Donald Trump said he expects to lower tariffs the US has imposed on Chinese goods over the fentanyl crisis and speak with China’s Xi Jinping about Nvidia Corp.’s flagship Blackwell artificial intelligence chip, as leaders of the world’s biggest economies seek to ease tensions in a meeting on Thursday.”

JOBS (MNI BRIEF): A preliminary estimate of U.S. private sector hiring from ADP points to a tepid recovery in October after a 32,000 net loss of jobs in September, ADP chief economist Nela Richardson said Tuesday as the payrolls services provider began releasing weekly labor market projections.

OTHER

GLOBAL (MNI INTERVIEW): Massive borrowing since the Covid pandemic is driving up the neutral level of interest rates while increasing the danger that tight monetary policy could amplify the effects of fiscal contraction, a former Bank of England economist and co-author with Larry Summers of the seminal work arguing that advanced economies were stuck in low-rate secular stagnation, told MNI.

JAPAN (BBG): “US Treasury Secretary Scott Bessent called on Japan’s new government to give the nation’s central bank the space to combat inflation — marking a stark contrast with his message at home for the Federal Reserve.”

JAPAN (MNI BRIEF): Japan’s consumer confidence index rose for the third consecutive month in October, increasing 0.5 points to 35.8 from 35.3 in September, prompting the government to upgrade its assessment from the previous month, data from the Cabinet Office showed Wednesday.

AUSTRALIA (MNI BRIEF): Australia’s Q3 headline inflation grew 3.2 % y/y – 20 basis points above expectations and up from Q2’s 2.1% – while trimmed-mean inflation rose to 3.0% from 2.7%, topping forecasts by 30bp, according to data from the Australian Bureau of Statistics released Wednesday.

MIDDLE EAST (BBG): “Prime Minister Benjamin Netanyahu ordered “forceful strikes” against Hamas in response to attacks on Israeli soldiers in Gaza, jeopardizing a US-brokered ceasefire that’s held for just over two weeks.”

SOUTH KOREA (BBG): " President Donald Trump said the US has a “special bond” with South Korea as he addressed a meeting of corporate leaders at the Asia-Pacific Economic Cooperation summit on Wednesday in Gyeongju."

CHINA

YUAN (SECURITIES DAILY): “The yuan is expected to remain relatively strong against the U.S. dollar in the near term, but any appreciation may be limited given the dollar's resilience as the currency has already fallen sharply in the first half of the year and the market has partly priced in potential Fed rate cuts, Securities Daily reported citing Wang Qing, analyst with Golden Credit Rating.”

PBOC (SHANGHAI SECURITIES NEWS): “The People’s Bank of China will focus on deepening the reform of the modern central banking system and further improving the efficiency of monetary policy transmission in the next five years, Shanghai Securities News reported citing analysts following the release of the Proposal of the Party's Central Committee on the formulation of the 15th Five-Year Plan.”

MNI: PBOC Net Injects CNY419.5 Bln via OMO Wednesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY557.7 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY419.5 billion after offsetting maturities of CNY138.2 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4384% at 09:42 am local time from the close of 1.5580% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Tuesday, compared with the close of 48 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.0843 Weds; +0.13% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0843 on Wednesday, compared with 7.0856 set on Tuesday. The fixing was estimated at 7.0954 by Bloomberg survey today.

MARKET DATA

AUSTRALIA Q3 TRIMMED MEAN CPI +1.0% Q/Q; EST. +0.8%; Q2 +0.7%

AUSTRALIA Q3 TRIMMED MEAN CPI +3.0% Y/Y; EST. +2.7%; Q2 +2.7%

AUSTRALIA Q3 CONSUMER PRICES +1.3% Q/Q; EST. 1.1%; Q2 +0.7%

AUSTRALIA Q3 CONSUMER PRICES +3.5% Y/Y; EST. +3.1%; Q2 +3.0%

AUSTRALIA SEPT. TRIMMED MEAN CPI +2.8% Y/Y; AUG. +2.6%

AUSTRALIA SEPT. CONSUMER PRICES +3.5% Y/Y; EST. 3.1%; AUG. +3.0%

SOUTH KOREA OCT. NON-MANUFACTURERS' CONFIDENCE 89.5; SEP. 90.5

SOUTH KOREA OCT. MANUFACTURERS' CONFIDENCE 92.4; SEP. 93.4

SOUTH KOREA SEPT. RETAIL SALES +7.7% Y/Y; AUG. +3.7%

SOUTH KOREA SEPT. DISCOUNT STORE SALES -11.7% Y/Y; -15.6%

SOUTH KORE SEPT. DEPT STORE SALES +4.8%; AUG. +2.8%

MARKETS

US TSYS: Treasuries Fail to Feature, As Markets Await APEC / FOMC

The US bond futures saw little or no movement in price today with volumes in the region mostly below average. TYZ5 is where it started the day at 113-15+, having inched up to 113-16+ briefly.

Cash was subdued also, with little expectations ahead of the FOMC meeting. Yields drifted marginally higher by up half a basis point.

- The US 2-Yr is at 3.498% (+0.6bps)

- The US 5-Yr is at 3.615% (+0.3bp)

- The US 10-Yr is at 3.981% (+0.4bp)

- The US 30-Yr is at 4.543% (+0.1bp)

Tonight markets focus on auctions for US$44bn of 2-Yr FRNs and various bills and notes.

Key data focus prior to FOMC will be mortgage applications, pending home sales and wholesale inventories. With much priced in now for bonds, the key risks remain any hawkish rhetoric from Powell, bringing into question future rate cuts. The 10-Yr continues to consolidate below 4.00% but any sense of uncertainty for future rate cuts could see the 4.00-4.15% reestablished. With so much riding on this week's cut and futures, the risks now are for disappointment and could see a move higher quicker in yields.

JGBS: Cash Curve Flatter, BoJ Seen On Hold, Focus on Dec/Jan Hike Risks

JGB futures are holding weaker, last 136.12, -.10 versus settlement levels. Some negative spillover has been likely today from the lunge in Aussie bond futures (post the CPI beat), while US futures have been quite steady ahead of the Fed later. For JGBs, we haven't been able to test under 136.00 at this stage, while important resistance is still some distance away on the upside.

- We also saw some modest downside pressure following earlier US Tsy Secretary remarks. Via X he said: "The Government’s willingness to allow the Bank of Japan policy space will be key to anchoring inflation expectations and avoiding excess exchange rate volatility."

- This comes ahead of tomorrow's policy meeting outcome, where little hike risks are seen by the economic consensus or market pricing. Focus will be on Dec/Jan hike risks and whether we see further dissenters who are in favour of a rate hike. We had 2 at the Sep board meeting, a shift to 3 would likely raise Dec hike risks.

- In the cash JGB space, the bias remains for flatter curves, the 2/30s down to +211bps. The 30-yr JGB yield looking to close under its 100-day EMA support (around 3.07% and we currently trade at 3.05%). The 10yr yield is relatively steady at 1.65%.

AUSSIE BONDS: Q3 CPI Beat Curbs 2025 Easing Pricing, 3yr Yield Eyeing 3.6% Test

Aussie bond futures have slumped, led by the front end, post the stronger than forecast Q3 CPI outcome. RBA easing expectations have been curbed dramatically. The end year implied rate is close to 3.54% (versus the current policy rate of 3.60%), with little easing risk seen in Nov. At the end of last week, the implied end year rate was around 3.37%. A full easing is not priced until the May meeting next year.

- ACGB yields have surged, led by the front with the 3yr up 12bps. This puts us at 3.57%, with focus on whether we can test above the policy rate of 3.60%. The 10yr is up 5bps to 4.22%.

- In the futures space, 3yr (YM) is off 12.5bps to 96.415, which is not too far away from late Sep/Early Oct lows sub 96.40. The 10yr (XM) is down 5.5bps to 95.76, piercing 20-day EMA support.

- For the cash 3yr bond, we made see buying interest emerge on a test of the 3.60% region, given risks of RBA easing into 2026. Focus will be on the next jobs report due on Nov 13th for Oct. A turn back lower in the unemployment rate is likely to push out easing expectations further, while a further rise could bring Q1 rate cut risks back into view.

- The AU 3/10s curve has flattened further to +65bps, down 7bps. The AU-US 10yr spread is up to +25bps, eyeing a fresh test around the +30bps level.

- Tomorrow on the data front we have Q3 trade prices.

BONDS: NZGBS: 2yr Swap Above 20-day EMA Post Aust CPI Spillover

NZGB yields are higher across the benchmarks, led by the back end, positive spill over has been evident from the ACGB yield surge post the higher than forecast Q3 CPI print (ACGB yields are 4-11.5bps firmer led by the front end). NZGB 2yr is back to close to 2.57%, while the 10yr is near 4.04%, both benchmarks tracking towards 20-day EMA resistance tests (2.61% for the 2yr, around 4.07% for the 10yr).

- The 2yr swap rate is already testing through the 20-day EMA resistance point, last near 2.41%, up 5bps for the session. The 50-day is at 2.53%. The AU-NZ 2yr swap rate differential continues to climb, up to 106bps.

- There hasn't been much of a shift in RBNZ pricing expectations. We are still close to 100% priced for a Nov 25bps cut.

- Earlier, RBNZ Director of Financial Markets Richardson spoke on the transmission of the 300bp of easing since August 2024. The MPC discussed this at the October meeting, implying they are concerned that the pass through of rate cuts to the economy has not been as efficient as expected. Richardson said today that global factors have increased NZ long-end yields, which have put upward pressure on domestic rates and thus financial conditions, the RBNZ could "adapt" policy to ease them again in order to achieve its 2%-mid-point inflation target.

- The NZGB 2/10s curve is holding elevated, last +147bps. In recent years we have struggled to maintain +150bps steepness. This may become more of a policy focus point if the NZ economy struggles for further positive traction in 2026.

- Note tomorrow we get the Oct ANZ activity outlook and business confidence prints.

FOREX: Weaker USD Not Sustained, A$ Outperforms Post, AUD/JPY Eyes 101.00

Softer USD sentiment from earlier proved to be short lived. The USD BBDXY index was last back around 1211.6, up from earlier lows near 1209. USD/JPY has rebounded nearly 100pips from earlier lows. Yen rallied earlier in the first part of trade as US Tsy Bessent encouraged the Japan government to let the BoJ deal with higher inflation. USD/CNH is up from fresh lows as well. AUD/USD is trying to break above 0.6600 post the stronger Q3 CPI prints, which sent local yields surging. The AUD/NZD is higher, holding above 1.1400 post the Q3 Australian CPI beat.

- USD/JPY got lows of 151.54, (which was still above the 20-day EMA) but last tracks near 152.50/55 (the bull trigger at 153.27 remains intact). US Tsy Bessent's earlier remarks aided the yen, as he stated the Japan government should give the BoJ the policy space it needs to keep inflation anchored and excessive FX volatility curbed. We have rebounded as US equity futures tick higher, as Trump said he will discuss Nvidia chips with China President Xi. US Tsy yields are little changed ahead of the FOMC later.

- AUD/JPY demand could also be a factor, the pair above 100.60, eyeing a test near 101.00. The A$ has outperformed in the G10 space post the Q3 CPI beat. Easing risks priced by the market for year end are very modest. AUD/USD is eyeing a test around 0.6630, which marked earlier Oct highs. AU-US yield differentials are firmer, the ACGB 3yr yield up 12bps today. NZD/USD is little changed, holding close to 0.5780.

- USD/CNH has recovered some ground, with the market arguably looking for a lower USD/CNY fix today (relative to mkt forecasts) to aid fresh downside. The pair was last back near 7.0980, with onshore spot also steady around 7.1000, another limit on CNH gains.

- US President Trump expressed confidence in a US-China deal, with potentially lower tariff rate tied to fentanyl. Headlines also crossed of China making some soybean purchases from the US in this past week.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.

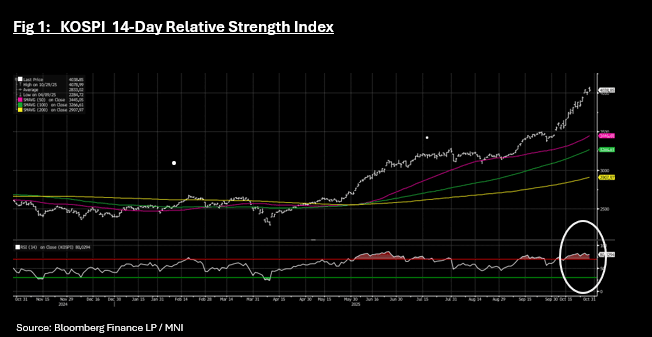

ASIA STOCKS: Focus on US Tech Earnings as Regional Bourses Strong Again

The coming days will see key US tech stocks Microsoft Corp., Alphabet Inc., Meta Platforms Inc., Amazon.com Inc. and Apple Inc report earnings with key regional tech stocks looking to add to recent gains. Tech stocks like Samsung, SK Hynix Inc and TSMC have reached new highs in recent days as ongoing tech optimism is a key driver for Asia's major bourses. Investors will focus on new from the APEC Summit with hopes resting on the cooling of relations between the US and China, coupled with the announcement of various trade deals with Asian trading partners.

- The NIKKEI was again the star today up almost 2.00% with tech stocks leading with the US President's visit to Japan interpreted as positive for the tech stocks as their potential to become important in US supply chains.

- The KOSPI bounced back from a rare down day yesterday to be up +0.71% today, and maintain its position above all major moving averages and for a second consecutive week maintain its position in overbought territory according to the 14-day RSI.

- China's major bourses saw an onshore offshore divide again with the HSI down -0.33% whilst the CSI 300 rose +0.48%, Shanghai up +0.37% and Shenzhen up +0.56%. The Hang Seng continues to lag its onshore counterparts down almost 2% over the last month whilst the CSI 300 is up over 2%.

- The Jakarta Composite is having it's worst run in some time, putting together four successive days of falls, after hitting recent new high of 8.274%. Today's modest losses sees the JCI maintain its position below the 20-day EMA.

- The hopes for a trade deal for India sees the NIFTY 50 reaching yet another new all time high of 25,993 and tips it into overbought area. P/E's on historical basis now are looking stretched and with a lot priced in in terms of optimism, any shortfall in trade deal could see a material retracement.

OIL: Crude Heading For Another Monthly Fall; Fed, EIA, US-CH & OPEC Key Events

Crude benchmarks are little changed today ahead of the Fed decision later and the release of EIA US oil market data. Prices have been supported by industry data showing a large US crude inventory drawdown. Brent is down 0.1% to $64.33/bbl after a high of $64.70 early in the APAC session before falling to $64.23. WTI is also 0.1% lower at $60.09/bbl after reaching $60.41. It fell to $59.95 but breaks below $60 have been short-lived. The USD index is up 0.1%.

- Bloomberg reported that US oil inventories fell a larger than expected 4mn barrels last week, after declining the previous week, according to people familiar with the API data. Gasoline and distillate were both lower down 6.3mn and 4.4mn respectively.

- With the focus on excess supply, a soft EIA report is likely to drive oil prices lower. They are down over 2.5% in October, which would be the third consecutive monthly decline.

- After today’s events, the market will be watching Sunday’s OPEC decision and the impact of the latest sanctions against Russia, as they cloud the outlook. Indian Oil said it wouldn’t discontinue its Russian crude purchases as long as they complied with sanctions. With restrictions focussed on the large Rosneft and Lukoil, both China and India refiners are looking to buy from smaller producers, according to Bloomberg.

- Presidents Trump and Xi meet Thursday and at this stage are expected to sign a trade deal.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.

Gold & Silver Higher Ahead Of Expected Fed Rate Cut

Gold has rallied during today’s APAC session ahead of the Fed decision later. While a 25bp rate cut is widely expected, monetary easing is positive for non-interest bearing bullion. It will be watching the tone of Chair Powell’s comments and is likely to strengthen if they come across as dovish but he’s unlikely to give much away. The market has almost another 25bp priced in for the December decision.

- Gold is up 0.3% to $3964.5/oz today following a high of $3982.33, remaining below $4000, despite a 0.1% rise in the USD BBDXY and stable US yields. Initial resistance is at $4161.4, 22 October high. With the metal remaining in overbought territory, it could correct further.

- Silver is also higher up 0.8% to $47.45 after reaching $47.610, but still below initial resistance at $49.456, 23 October high.

- Presidents Trump and Xi meet Thursday and at this stage are expected to sign a trade deal.

- Equities are mixed with the S&P e-mini up 0.2%, CSI 300 +0.5% but the Straits Times down 0.3%. Oil prices are slightly lower with WTI -0.1% to $60.10/bbl. Copper is down 0.1%.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 29/10/2025 | 0700/0800 | Flash Quarterly GDP Indicator | ||

| 29/10/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 29/10/2025 | 0800/0900 | *** | GDP (p) | |

| 29/10/2025 | 0930/0930 | ** | BOE Lending to Individuals | |

| 29/10/2025 | 0930/0930 | ** | BOE M4 | |

| 29/10/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 29/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 29/10/2025 | 1100/1200 | ** | PPI | |

| 29/10/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/10/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 29/10/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 29/10/2025 | 1430/1030 | BOC press conference | ||

| 29/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 29/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 29/10/2025 | 1800/1400 | *** | FOMC Statement | |

| 30/10/2025 | - | European Central Bank Meeting | ||

| 30/10/2025 | 0030/1130 | ** | Trade price indexes | |

| 30/10/2025 | 0300/1200 | *** | BOJ Policy Rate Announcement | |

| 30/10/2025 | 0630/0730 | *** | GDP (p) | |

| 30/10/2025 | 0630/0730 | ** | Consumer Spending | |

| 30/10/2025 | 0700/0800 | ** | Retail Sales | |

| 30/10/2025 | 0800/0900 | *** | HICP (p) | |

| 30/10/2025 | 0800/0900 | ** | KOF Economic Barometer | |

| 30/10/2025 | 0800/0900 | ** | Economic Tendency Indicator | |

| 30/10/2025 | 0855/0955 | ** | Unemployment | |

| 30/10/2025 | 0900/1000 | *** | GDP (p) | |

| 30/10/2025 | 0900/1000 | *** | GDP (p) | |

| 30/10/2025 | 0900/1000 | *** | Bavaria CPI | |

| 30/10/2025 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 30/10/2025 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 30/10/2025 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 30/10/2025 | 1000/1100 | ** | EZ Unemployment | |

| 30/10/2025 | 1000/1100 | *** | EZ GDP 1st (Prelim Flash) | |

| 30/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 30/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 30/10/2025 | 1230/0830 | * | Payroll employment | |

| 30/10/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/10/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/10/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 30/10/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 30/10/2025 | 1315/1415 | *** | ECB Deposit Rate | |

| 30/10/2025 | 1315/1415 | *** | ECB Main Refi Rate | |

| 30/10/2025 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 30/10/2025 | 1345/1445 | ECB Press Conference | ||

| 30/10/2025 | 1355/0955 | Fed's Michelle Bowman |