BONDS: NZGBS: 2yr Swap Above 20-day EMA Post Aust CPI Spillover

NZGB yields are higher across the benchmarks, led by the back end, positive spill over has been evident from the ACGB yield surge post the higher than forecast Q3 CPI print (ACGB yields are 4-11.5bps firmer led by the front end). NZGB 2yr is back to close to 2.57%, while the 10yr is near 4.04%, both benchmarks tracking towards 20-day EMA resistance tests (2.61% for the 2yr, around 4.07% for the 10yr).

- The 2yr swap rate is already testing through the 20-day EMA resistance point, last near 2.41%, up 5bps for the session. The 50-day is at 2.53%. The AU-NZ 2yr swap rate differential continues to climb, up to 106bps.

- There hasn't been much of a shift in RBNZ pricing expectations. We are still close to 100% priced for a Nov 25bps cut.

- Earlier, RBNZ Director of Financial Markets Richardson spoke on the transmission of the 300bp of easing since August 2024. The MPC discussed this at the October meeting, implying they are concerned that the pass through of rate cuts to the economy has not been as efficient as expected. Richardson said today that global factors have increased NZ long-end yields, which have put upward pressure on domestic rates and thus financial conditions, the RBNZ could "adapt" policy to ease them again in order to achieve its 2%-mid-point inflation target.

- The NZGB 2/10s curve is holding elevated, last +147bps. In recent years we have struggled to maintain +150bps steepness. This may become more of a policy focus point if the NZ economy struggles for further positive traction in 2026.

- Note tomorrow we get the Oct ANZ activity outlook and business confidence prints.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NZD: Asia Wrap - NZD/USD Weakness Gets A Reprieve

The NZD/USD had a range of 0.5771 - 0.5786 in the Asia-Pac session, going into the London open trading around 0.5785, +0.25%. US stocks found some support and the USD’s bout of strength stalled as the data on Friday came in as expected. The NZD found some demand back towards the 0.5750 area and is trying to bounce, getting an added nudge this morning as the risk of a US government shutdown increases. The NZD broke through its pivotal 0.5800 support last week which should keep the pair under pressure heading into payrolls. The first sell zone would be back towards the 0.5850/0.5900 area.

- Bloomberg - “RBNZ Says Pandemic Inflation Taught It Lessons for Future Shocks. The Reserve Bank’s Monetary Policy Committee has gained valuable insights into how economic activity, price setting by businesses and inflation expectations evolve during periods of high inflation and economic volatility, Conway said Monday in Wellington after releasing a review of monetary policy in recent years.”

- “Guy LeBas, chief fixed-income strategist for Janney Montgomery Scott. “The next thing to get priced in is probably a government shutdown, which has historically been a bad thing for short-term economic growth and pulled US Treasury yields down,” LeBas said.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5785(NZD904m Sept 30), 0.5875(NZD372m Sept 30) - BBG

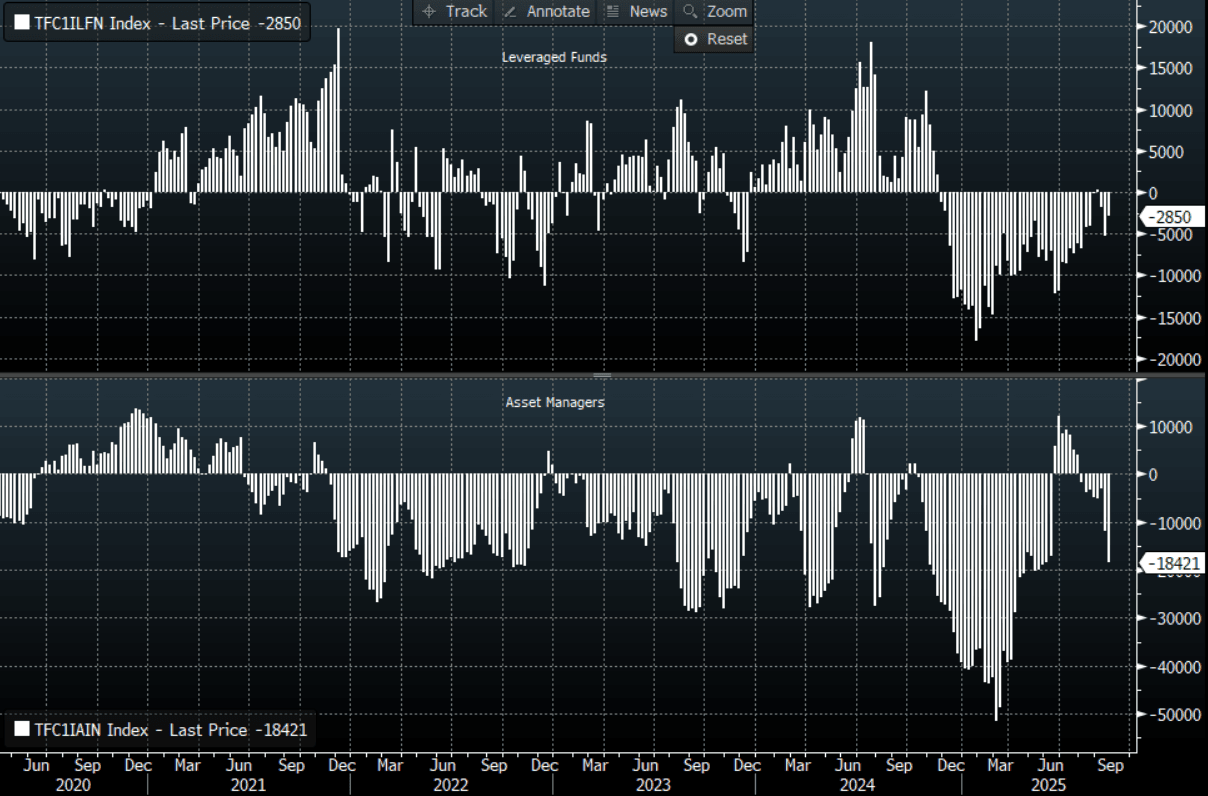

- CFTC Data of last week shows Asset Managers continuing to rebuild their short positions in the NZD, -18421(Last -11933). The Leveraged community don’t seem as convinced and reduced their own shorts, -2850(Last -5327).

- AUD/NZD range for the session has been 1.1328 - 1.1354, currently trading around 1.1350. The Cross has broken above the multiple highs around the 1.1200 area and is consolidating its extension above 1.1300, helped by the AU CPI print. Dips should now continue to be supported as the market turns its focus towards the 1.1400/1.1500 area.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Slips Back Below 149.00 As US Shutdown Looms

The USD/JPY range has been 148.89 - 149.52 in the Asia-Pac session, it is currently trading around 148.95, -0.35%. The USD’s bout of strength stalled as the data on Friday came in as expected. This saw USD/JPY fail toward 150.00 and the drift lower has extended this morning as the market begins to price in a US shutdown. Having closed back above 149.00 to end the week the JPY bears would be hoping that dips remain supported. Non-Farms this week if released could have a significant bearing on price, so the market will be setting up for this to start the week. First Support is around the 148.50/149.00 area, if this doesn't hold due to shutdown fears we will go into payrolls back in familiar ranges.

- “LDP contender Sanae Takaichi hinted at a review of Japan’s $550 billion investment fund that was part of its pact with the US.” - BBG

- "JAPAN TO CONVENE EXTRAORDINARY DIET SESSION MID-OCT: YOMIURI" - BBG

- (Reuters) - “The Bank of Japan will probably raise its benchmark interest rate at least four more times to 1.5% before Governor Kazuo Ueda's term ends in early 2028, former central bank board member Makoto Sakurai told Reuters. Sakurai, who retains close contact with incumbent policymakers, forecast another hike by year-end, two more increases in fiscal 2026, and one or two hikes in the year ending March 2028.”

- Bloomberg - “Dollar-Yen Risk Is Overlooked by Investors, Morgan Stanley Says. Morgan Stanley says markets are underpricing the risk that the dollar will push lower against the yen. It recommends buying options ahead of US jobs data, a potential US US government shutdown and the party leadership election in Japan.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 150.70($410m). Upcoming Close Strikes : 146.50($1.09b Oct 1) - BBG.

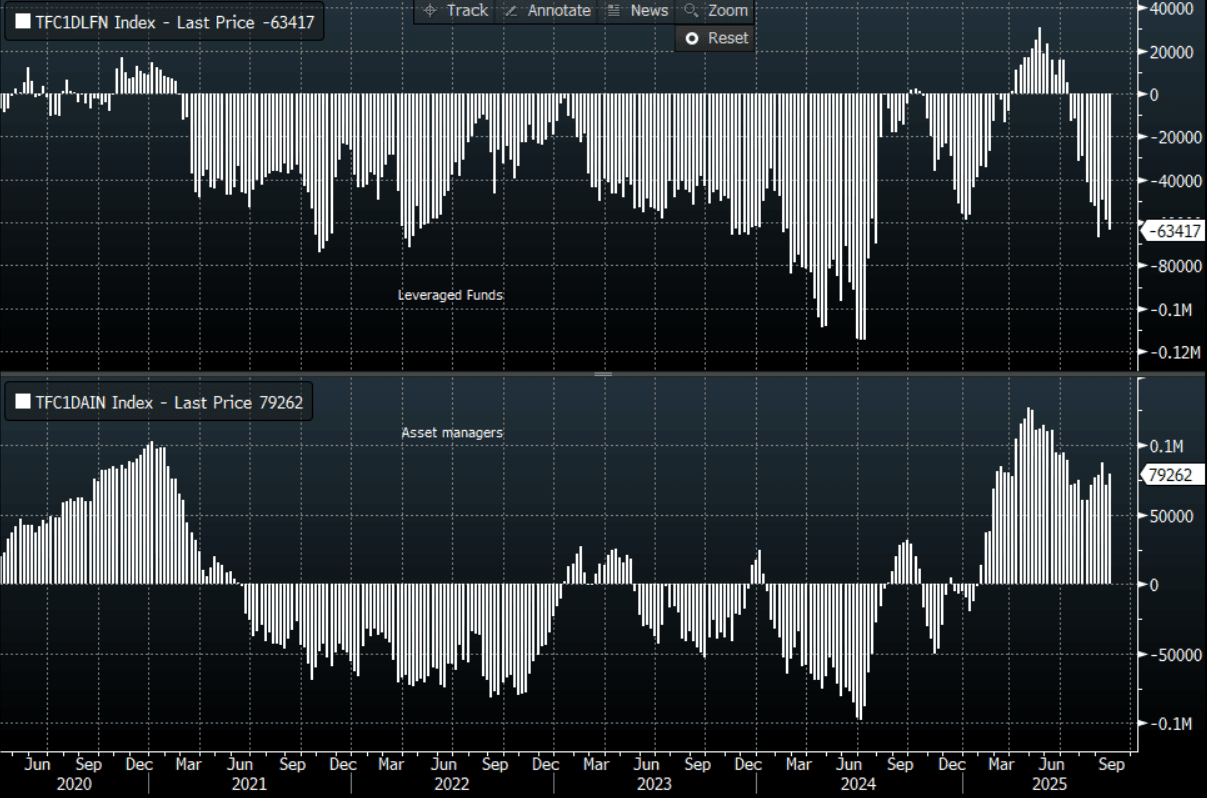

- CFTC data shows last week asset managers increased their JPY longs slightly +79262( Last +71162), leveraged funds though again used the dip to add to their short position as the support held, -634171(Last -58811). The diverging views amongst investors continue to build.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Bounces As USD Gets Hit On Shutdown Fears

The AUD/USD has had a range of 0.6547 - 0.6567 in the Asia- Pac session, it is currently trading around 0.6565, +0.35%. US stocks found some support and the USD’s bout of strength stalled as the data on Friday came in as expected. The AUD found some demand back towards the 0.6500 area and is trying to bounce, getting an added nudge this morning as the risk of a US government shutdown increases. Price is back in the range and the market will be turning its attention towards the Fridays Payroll number. RBA is tomorrow.

- MNI AU - RBA Widely Expected To Hold On 30 September. The focus of the week will be Tuesday’s RBA decision followed by Governor Bullock’s press conference. As it is widely expected to keep rates at 3.6% and there won’t be an updated set of forecasts, the tone of the statement and Bullock’s comments will be scrutinised after disinflation appears to have stalled in Q3 and the Governor said to a parliamentary committee last week that "domestic data have been broadly in line with our expectations or if anything slightly stronger". The Board is likely to remain highly data dependent.

- “Australia’s fiscal 2025 budget deficit is set to be just under A$10 billion ($6.56 billion) compared with the government’s forecast of A$27.9 billion.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD405m), 0.6625(AUD1.29b), 0.6725(AUD1.19b). Upcoming Close Strikes : 0.6600(AUD943m Oct 1), 0.6600(AUD1.57b Oct 2), 0.6700(AUD1.64b Oct 1) - BBG

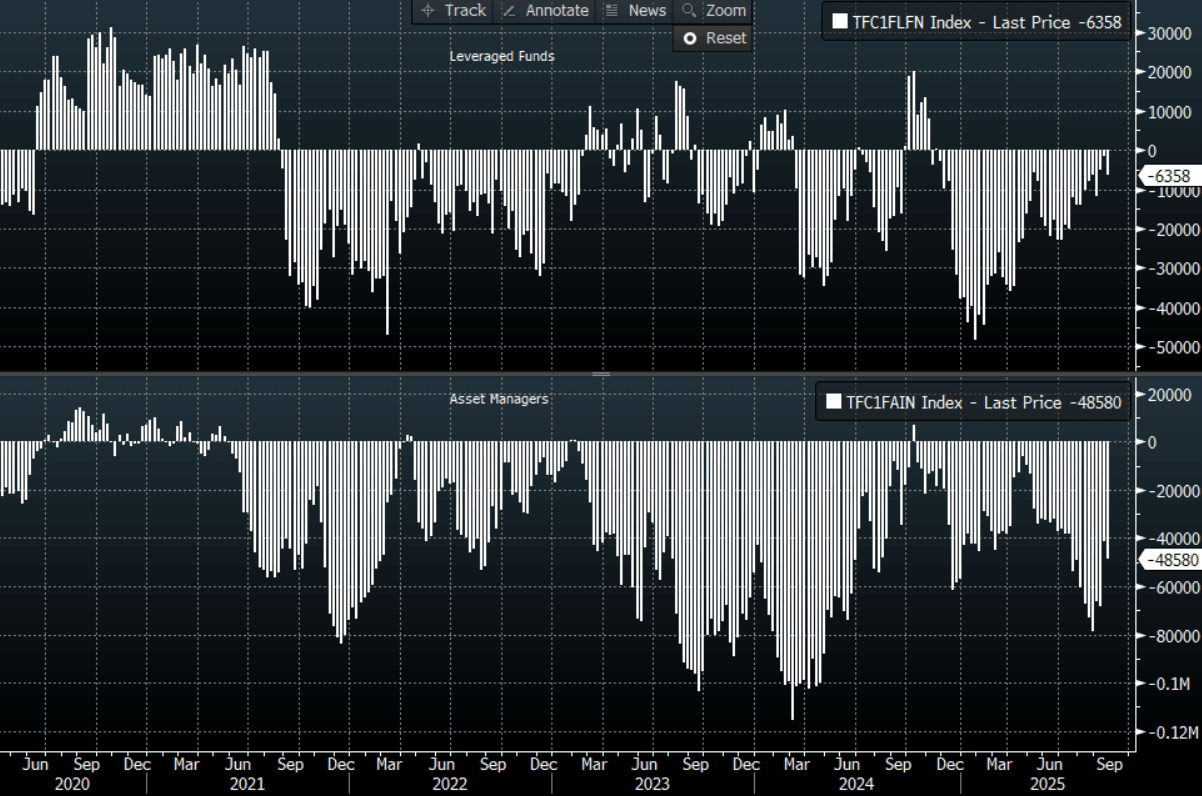

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

- AUD/JPY - Asia-Pac range 97.67 - 97.99, Asia is trading around 97.70. The pair found solid demand back towards 97.00 and bounced last week with the help of the AU CPI print. While above 97.00 the focus will remain on September’s highs toward 98.50.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P