US TSYS: Treasuries Fail to Feature, As Markets Await APEC / FOMC

The US bond futures saw little or no movement in price today with volumes in the region mostly below average. TYZ5 is where it started the day at 113-15+, having inched up to 113-16+ briefly.

Cash was subdued also, with little expectations ahead of the FOMC meeting. Yields drifted marginally higher by up half a basis point.

- The US 2-Yr is at 3.498% (+0.6bps)

- The US 5-Yr is at 3.615% (+0.3bp)

- The US 10-Yr is at 3.981% (+0.4bp)

- The US 30-Yr is at 4.543% (+0.1bp)

Tonight markets focus on auctions for US$44bn of 2-Yr FRNs and various bills and notes.

Key data focus prior to FOMC will be mortgage applications, pending home sales and wholesale inventories. With much priced in now for bonds, the key risks remain any hawkish rhetoric from Powell, bringing into question future rate cuts. The 10-Yr continues to consolidate below 4.00% but any sense of uncertainty for future rate cuts could see the 4.00-4.15% reestablished. With so much riding on this week's cut and futures, the risks now are for disappointment and could see a move higher quicker in yields.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: BONDS NZGBS: Strong Start to the Week for Bonds

- NZGBs ended Monday with bond yields 2-2.5bps lower across the yield curve.

- A good start to the week for NZGBS as bonds rallied across the curve. Best performance came in the 2-5 Yr which fell over 2bps whilst the 10-Yr was down 2bps also

- Swap rates closed up to 3bps lower in the front end with the 10-Yr lower by 1bps

- Limited key economic data out today with August Filled Jobs SA MoM in line with July at +0.2%.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for October, with a cumulative 57bps by November 2025.

- Issuance tomorrow will be $100m 105-day bills, $100m 161-day bills and $50m 357-day bills.

OIL: Crude Lower As Excess Supply Worries Come Back Into Focus

Oil prices have unwound Friday’s moderate gains during Monday’s APAC trading as excess supply concerns dominate with flows from Iraqi Kurdistan restarting on the weekend and OPEC due to meet on 5 October. WTI is down 0.6% to $65.36/bbl, close to the intraday high, while Brent is 0.6% lower at $69.73/bbl after reaching $69.84. The USD index is down 0.2%.

- The focus this week will be on Friday’s September US payroll data, which could be delayed if there isn’t an agreement to lift the US debt ceiling, and Sunday’s OPEC meeting to determine November’s production target. Currently, it is expected to lift it by more than October’s +137kbd but capacity within the group is becoming an issue. The IEA is forecasting a record oil surplus for 2026.

- Iraq has revised up its export forecast to 3.65mbd after the resumption of shipments from Iraqi Kurdistan through the Kirkuk-Ceyhan pipeline on the weekend after a deal was finally reached with Turkey. Flows were halted in March 2023.

- Later the Fed’s Waller, Musalem and Bostic speak as well as Cleveland’s Hammack with ECB’s Lane & BoE’s Ramsden. The ECB’s Cipollone, Schnabel and Machado also appear. In terms of data, there is US Dallas Fed September manufacturing, preliminary September Spanish CPI, September European Commission survey.

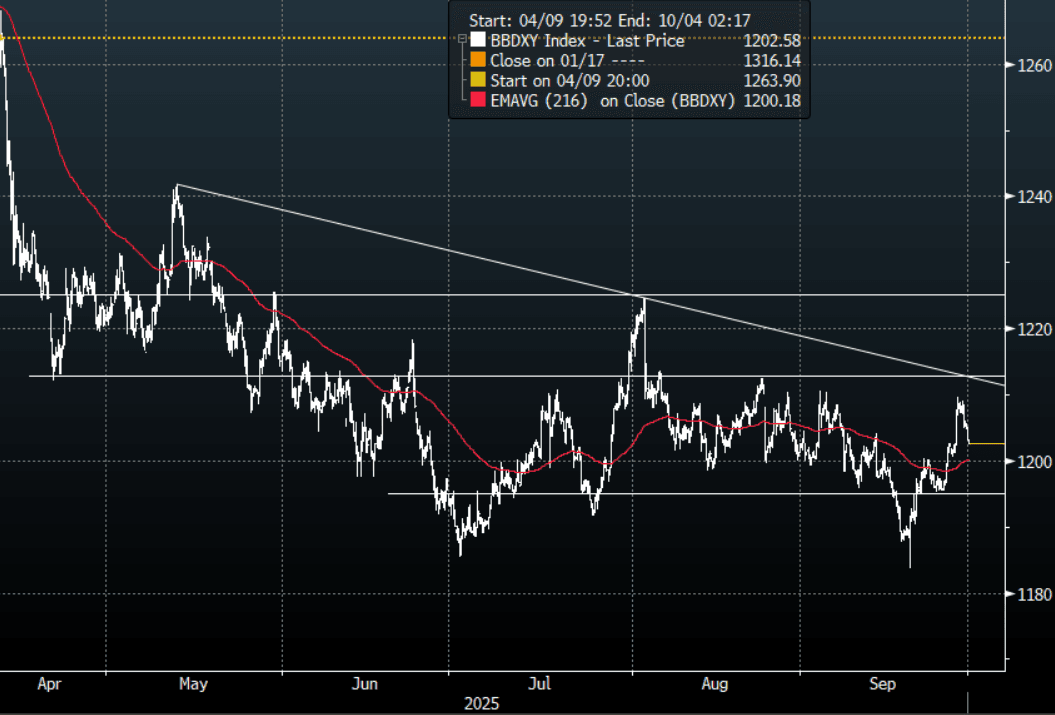

FOREX: Asia FX Wrap - The USD Slips Lower As Shutdown Looms

The BBDXY has had a range of 1202.41 - 1205.07 in the Asia-Pac session; it is currently trading around 1202, -0.25%. The USD topped out towards 1210 again on Friday and has drifted lower very easily, the follow through this morning being aided by US shutdown fears. I can’t see any big directional moves this week until the market sees the Payroll number. Next resistance is back towards the 1215-1225 area where I would expect sellers to remerge initially. The big question is at what level do the global asset managers return to selling for hedging purposes. First support back towards the 1200 area and then 1195. Quarter-end for Asset managers likely to see some USD selling to rebalance portfolios.

- EUR/USD - Asian range 1.1702 - 1.1729, Asia is currently trading 1.1730. The pair has drifted back above 1.1700, I suspect sellers could reemerge above 1.1750 initially. The deeper correction looks to have been put on hold for now as the focus turns toward the payroll number.

- GBP/USD - Asian range 1.3394 - 1.3434, Asia is currently dealing around 1.3435. The pair could not break through its support around the 1.3300 area, price has bounced back into the range. The market should be looking for bounces to fade, first sell zone back towards the 1.3500 area.

- USD/CNH - Asian range 7.1199 - 7.1432, the USD/CNY fix printed 7.1089, Asia is currently dealing around 7.1230. The pair stalled toward 7.1500 and collapsed lower again very easily. The area just below 7.1000 has proved to be well supported recently lets see if that continues.

- Cross asset : SPX +0.35%, Gold $3798, US 10-Year 4.158%, BBDXY 1202, Crude Oil $65.31

- Data/Events : Spain CPI/Retail Sales, EZ Consumer Confidence

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P