ASIA STOCKS: Focus on US Tech Earnings as Regional Bourses Strong Again

The coming days will see key US tech stocks Microsoft Corp., Alphabet Inc., Meta Platforms Inc., Amazon.com Inc. and Apple Inc report earnings with key regional tech stocks looking to add to recent gains. Tech stocks like Samsung, SK Hynix Inc and TSMC have reached new highs in recent days as ongoing tech optimism is a key driver for Asia's major bourses. Investors will focus on new from the APEC Summit with hopes resting on the cooling of relations between the US and China, coupled with the announcement of various trade deals with Asian trading partners.

- The NIKKEI was again the star today up almost 2.00% with tech stocks leading with the US President's visit to Japan interpreted as positive for the tech stocks as their potential to become important in US supply chains.

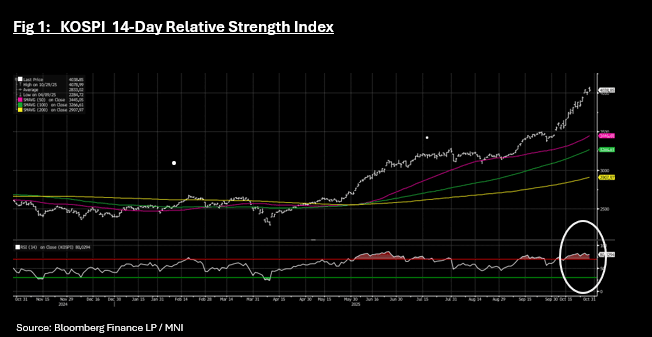

- The KOSPI bounced back from a rare down day yesterday to be up +0.71% today, and maintain its position above all major moving averages and for a second consecutive week maintain its position in overbought territory according to the 14-day RSI.

- China's major bourses saw an onshore offshore divide again with the HSI down -0.33% whilst the CSI 300 rose +0.48%, Shanghai up +0.37% and Shenzhen up +0.56%. The Hang Seng continues to lag its onshore counterparts down almost 2% over the last month whilst the CSI 300 is up over 2%.

- The Jakarta Composite is having it's worst run in some time, putting together four successive days of falls, after hitting recent new high of 8.274%. Today's modest losses sees the JCI maintain its position below the 20-day EMA.

- The hopes for a trade deal for India sees the NIFTY 50 reaching yet another new all time high of 25,993 and tips it into overbought area. P/E's on historical basis now are looking stretched and with a lot priced in in terms of optimism, any shortfall in trade deal could see a material retracement.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Good Start to the Week for JGBs

- JGBs are up to 2.5bs tighter in yield today as the whole curve rallied.

- Best performance came from the 20-Yr and 30-Yr which are -2.5bp lower.

- Futures are higher in price with the 10-Yr up +0.24 to 136.03 yet remains below all major moving averages. The 20-day EMA is at 136.36.

- The Japan Final July Coincident Index came in at 114.1, from 115.9 in June and the Leading index was 106.1 from 105.

- This week sees a 2-Yr and 10-Yr JGB auction.

EURUSD TECHS: Monitoring Support Around The 50- Day EMA

- RES 4: 1.2063 2.236 proj of the Feb 28 - Mar 18 - 247 price swing

- RES 3: 1.2000 Round number resistance

- RES 2: 1.1919/23 High Sep 17 / 2.0 proj of Feb 28 - Mar 18-27 swing

- RES 1: 1.1754/1820 High Sep 25 / 23

- PRICE: 1.1731 @ 06:04 BST Sep 29

- SUP 1: 1.1646 Low Sep 25

- SUP 2: 1.1574 Low Aug 27

- SUP 3: 1.1528 Low Aug 5

- SUP 4: 1.1392 Low Aug 1 and bear trigger.

The trend theme in EURUSD is unchanged, it remains bullish and recent weakness is considered corrective. However, support at 1.1681. the 50-day EMA, has been breached. A clear break of this average would signal scope for a deeper retracement and expose 1.1574 initially, the Aug 27 low. For bulls, a resumption of gains would refocus attention on 1.1923, a Fibonacci projection. Initial firm resistance to watch is 1.1820, the Sep 23 high.

AUSTRALIA: Decent Rally Ahead of RBA

- ACGBs have staged a decent rally today ahead of tomorrow's RBA decision and on headlines that the budget deficit has narrowed.

- Market consensus remains for no change from all of the estimates on BBG currently, with rates set to remain at 3.60%.

- A rally across the yield curve sees lower yields by 3.5-4.5bps with the 10-Yr and 15-Yr the best performers.

- Australia's 10-Yr bond future is up +0.04 to 95.61, below all major moving averages with the 20-day EMA at 95.66.

- The 3-Yr bond future is up +0.04 at 96.42 and is also below all major moving averages.

- This week sees Australia sell A$1.2bn of 2034 bonds on Oct 1, A$1bn 133-day bills and A$1bn 70-day bills on October 2 and A$1bn of 2032 bills on October 3rd.

- There remains only 6bps of cuts priced in over the next month with 16bps over the next three.