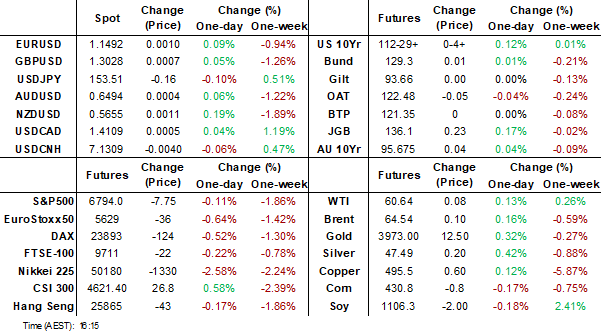

MNI EUROPEAN MARKETS ANALYSIS: Yen Crosses Up From Lows

- Risk off in the equity and crypto space dominated early, but we are comfortably up from worst levels. It was similar themes in the FX and rates space, with yen crosses under pressure before sentiment stabilized. Gold rose, while oil was little changed.

- New Zealand Q3 jobs growth was weaker than forecast, but wages and the unemployment rate were in line.

- Central bank decisions in Sweden, Poland and Brazil are due later, while US ISM services data are also scheduled.

MARKETS

US TSYS: TYZ5 Fails to Hold Above Key Tech Level

Bond futures took the overnight lead and rallied strongly in the morning session, but failed to hold above a key technical, falling back in the afternoon. TYZ5 is up +0.04 at 112-29+, after a high of 113-02+ earlier, just above the 20-day EMA of 113-01+ only to retreat in afternoon trade.

Cash has been strong also with yields 1-2bps lower across the curve.

- The 2-Yr fell -1.6bps to 3.561%

- The 5-Yr is down -1.7bps at 3.68%

- The 10-Yr is lower by -1.6bps at 4.072%

- The 30-Yr is down -1bps at 4.657%.

The bond market has been starved of data but will get some non-government led releases tonight in the ADP Employment Change (consensus 30k; prior -32k) S&P Global US Services PMI (forecast 55.2; prior 55.2) and ISM Services Index (forecast 50.8; prior 50.0).

For issuance, the focus tonight remains on bill issuance with a US$95bn 6-week bill auction ahead of the US Treasury Quarterly Funding announcement.

JGBS: Little Changed But Weaker After Tepid Demand At Today's 10Y Auction

JGB futures are stronger, +15 compared to settlement levels.

- Japanese bond futures trimmed earlier gains after a key measure of demand at today’s 10-year auction fell to its lowest since May, though they remain slightly higher amid a global bond rally.

- Demand at Japan’s 10-year government bond auction was subdued, as investors weighed the risk of a near-term BOJ rate hike despite the central bank’s cautious stance, while fiscal concerns also dampened sentiment. The average bid-to-cover ratio declined to 2.9734x from 3.3356x at the previous auction in October. Moreover, the low price failed to meet expectations at 100.34, according to the Bloomberg dealer poll. However, the tail shortened to 0.13 from 0.19.

- Cash JGBs are 1bp richer to 1bp cheaper, with a steepening bias. The benchmark 10-year yield is 0.2bp lower at 1.670% versus the cycle high of 1.705%.

- Swap rates are flat to 1bp lower.

- Tomorrow, the local calendar will see Cash Earnings, S&P Global Composite & Services PMIs and Tokyo Avg Office Vacancies data.

Source: Bloomberg Finance LP

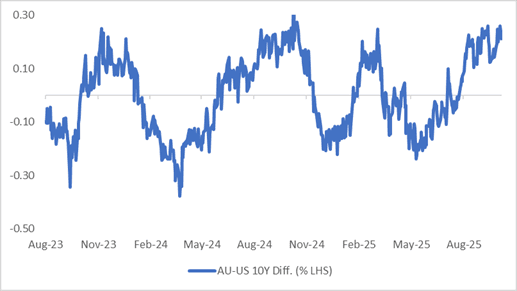

AUSSIE BONDS: Solid Rally But AU-US10Y Diff Sits Near Top Of Range

ACGBs (YM +5.5 & XM +3.5) are stronger but off session bests. Today’s move leaves futures 4bps stronger than yesterday’s pre-RBA levels despite RBA Governor Bullock’s hawkish tone.

- Global bonds are benefiting from a general risk-off tone across markets, although there has been a bounce off lows.

- Cash US tsys are 1-2bps richer in today’s Asia-Pac session after yesterday’s modest rally.

- Cash ACGBs are 4-5bps richer with the AU-US 10-year yield differential at +24bps. At this level, the spread remains near the upper end of the ±30bps range that has persisted since November 2022. (see chart)

- Today’s auction of the Mar-36 bond showed solid pricing for ACGBs, with the weighted average yield coming in 0.43bps below prevailing mid-yields, according to Yieldbroker. Moreover, the cover ratio nudged higher to 3.5167x from 3.4917x.

- The bills strip has bull-flattened across contracts, with pricing +1 to +6.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 15% probability, with a cumulative 11bps of easing priced by February 2026.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

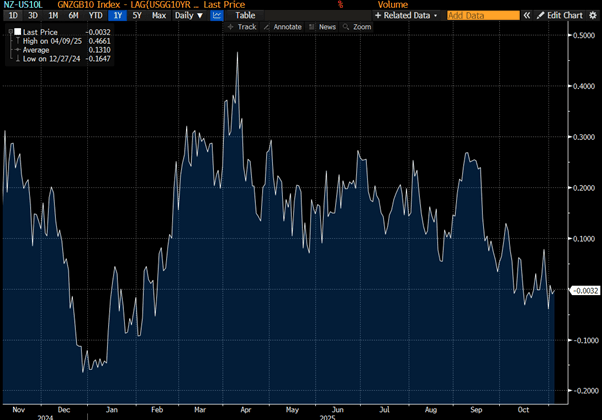

BONDS: NZGBS: Richer But NZ-US10Y Diff Wider

NZGBs closed 2-3bps richer, but with the NZ-US 10-year yield differential 2bps wider at +2bps. (see chart)

- NZ's jobless rate held steady at 5.3% in the third quarter, matching economist expectations. Employment was unchanged quarter-on-quarter, compared with a revised 0.2% fall in the previous quarter, while employment declined 0.6% year-on-year, a smaller drop than in the second quarter. The labour force participation rate was 70.3%.

- Average hourly earnings rose 0.7% from the previous quarter, and non-government wages increased 0.4% including overtime and 0.5% for ordinary time.

- Swap rates are 2-3bps lower, with the 2-year rate rejecting off the 20-day EMA.

- RBNZ dated OIS pricing is slightly softer across meetings. 26bps of easing is priced for November, with a cumulative 33bps by February 2026.

- Tomorrow, the local calendar will see the RBNZ at the Select Committee to discuss the FinStab Report, and the Government will release its 3-Month Financial Statements.

- Also tomorrow, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

FOREX: Asia-Pac FX: The USD Grinding Through Long-Term Resistance

The BBDXY has had a range today of 1225.29 - 1226.35 in the Asia-Pac session; it is currently trading around 1225, -0.05%. The USD continues to build on its recent gains eking out new highs every day, what stood out was with risk turning lower the USD gained some tailwinds as its status as a “safe haven” looks to have been reinstated. The 1230 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made and the dips remain very shallow pointing to a reduction in shorts. A sustained move back above 1230 would potentially signal a medium term low is in place and a deeper pullback is on the cards.

- EUR/USD - Asian range 1.1479 - 1.1498, Asia is currently trading 1.1490. The pair has broken back below1.1500, and I suspect rallies will now be sold into with the first resistance back toward 1.1550-1.1600. The next target is the 1.1350/1.1400 support; a break below this could signal a deeper correction toward the 1.1100/1.1200 area.

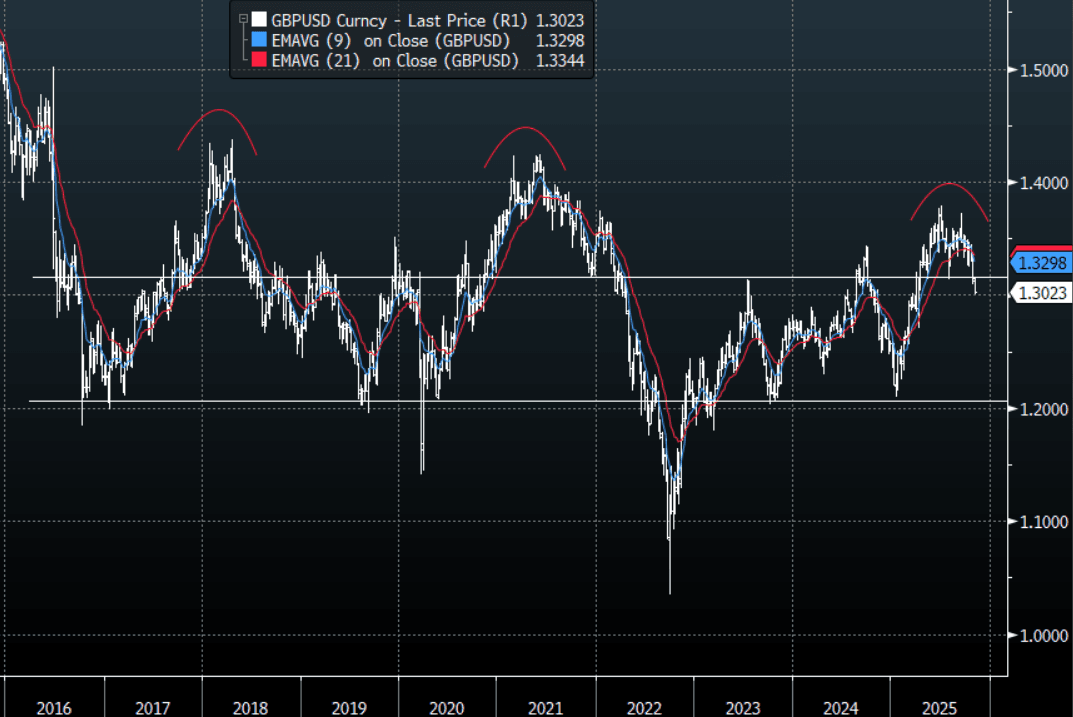

- GBP/USD - Asian range 1.3010 - 1.3028, Asia is currently dealing around 1.3020. The pair broke through its support around the 1.3150 area and extended lower overnight. I continue to favor fading rallies though as GBP looks like it has put in a medium term top. First sell zone back toward 1.3150 and then the 1.3300 area.

- Cross asset : SPX -0.15%, Gold $3960, US 10-Year 4.0680%, BBDXY 1225, Crude Oil $60.45

- Data/Events : Italy New Car Registrations/HCOB Italy PMI’s/Retail Sales, France Industrial Production/Manufacturing Production/HCOB France PMI’s, Spain HCOB Spain PMI’s, Germany Factory Orders/HCOB Germany PMI’s, EZ HCOB Eurozone PMI’s/PPI

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

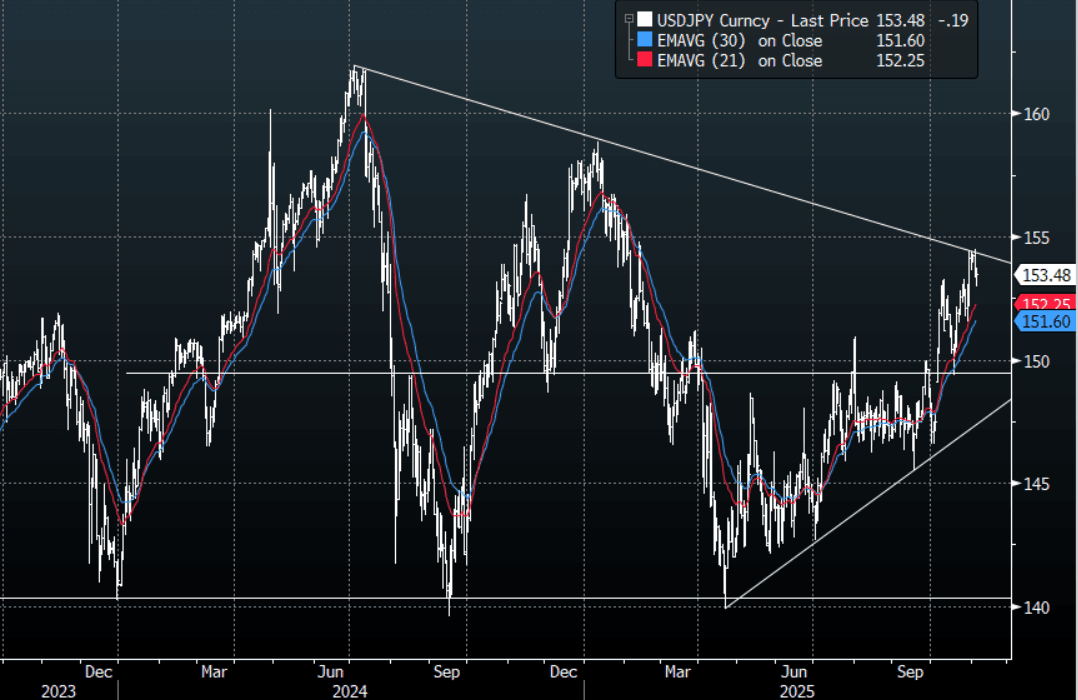

JPY: Asia-Pac: USD/JPY - Bounces Off 153.00 As Risk Pares Back Losses

The USD/JPY range today has been 152.96 - 153.75 in the Asia-Pac session, it is currently trading around 153.45, -0.15%. The pair has pulled back from the 154/155 area as the Yen gets bought heavily in the crosses on the back of the pullback in risk, the collapse in Asian stocks today added to its headwinds. While this backdrop plays out I suspect the resistance around the 154/155 area should continue to offer solid resistance. Look for dips to continue to be supported while above 149-150, first support is toward the 151.50/152.00 area and then the more important 149.00-150.00 level.

- MNI: BOJ Minutes: More Than Two Members Positive On Hike. One Bank of Japan board member, apart from the two who proposed raising the policy rate to 0.75%, said it was time to consider another increase as more than six months had passed since the last hike, minutes of the Sept 18-19 meeting showed Wednesday.

- However, the member noted that uncertainty remained over the pace of the U.S. economic slowdown and said it was appropriate for the Bank to maintain its current policy stance for the time being.

- Options : Close significant option expiries for NY cut, based on DTCC data: 150.65($450m). Upcoming Close Strikes : 155.00($1.81b Nov 6), 155.35($1.38b Nov 6) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

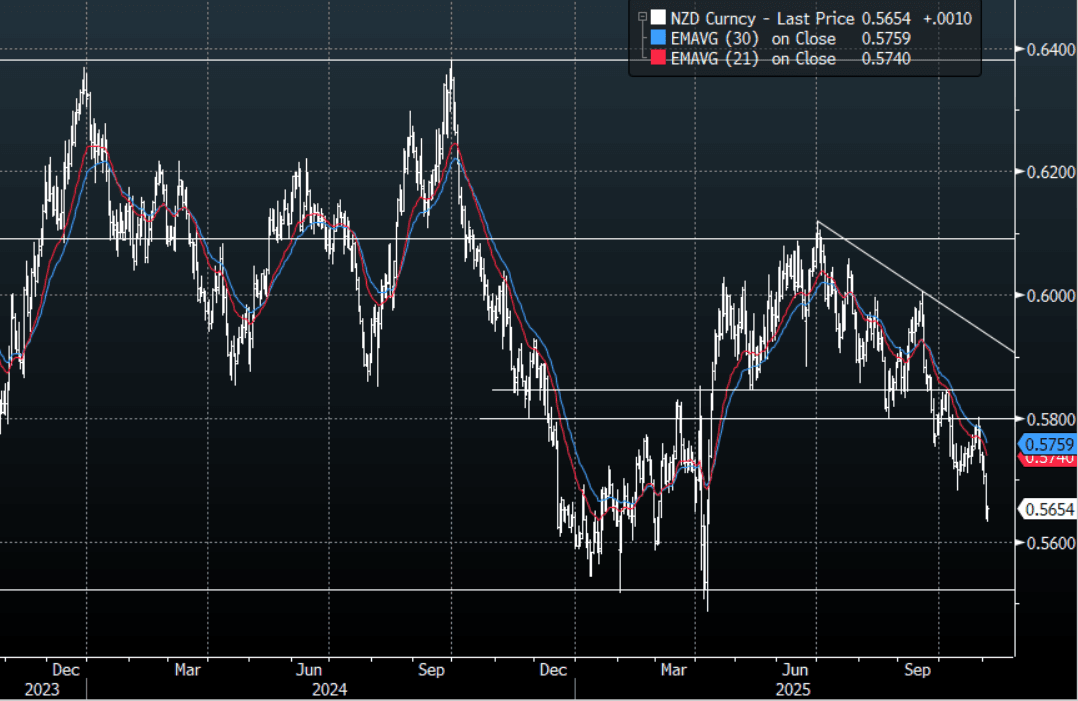

NZD: Asia-Pac: NZD/USD, Can't Extend Lower Even With Poor Unemployment Data

The NZD/USD had a range of 0.5631 - 0.5659 in the Asia-Pac session, going into the London open trading around 0.5655, +0.20%. The NZD has actually drifted higher in our session, this after a poor NZ Unemployment print and Asian stocks collapsing. This price action potentially points to the market already being positioned short, though some decent option expiries that are close could also be playing a part. The NZD stands out as a vehicle to short against a resurgent USD but it is worth noting that because of the size of the market it can very quickly become all positioned the same way. I think the USD will need to do the heavy lifting and break above its pivotal resistance for the NZD to test the 0.5500 lows. Should this correction in risk have more room to move lower then I suspect the NZD will remain a sell on rallies with the first resistance back toward the 0.5725-0.5750 area.

- MNI BRIEF: New Zealand Unemployment 5.3% In Q3. The underutilisation rate edged up to 12.9% from 12.8%, while the employment rate eased to 66.6% from 66.8%. The Reserve Bank of New Zealand expects unemployment to reach 5.2% by December.

- “RBNZ GOVERNOR HAWKESBY: HOUSE PRICES AND CREDIT GROWTH NOT RAISING RED FLAGS, SO CAN HAVE MORE BASELINE MORTGAGE LOAN-TO-VALUE RATIO SETTINGS" - RTRS

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5650(NZD1.1.4b Nov 5), 0.5675(NZD1.27b Nov 5), 0.5750(NZD604m Nov 5). Upcoming Close Strikes : 0.5730(NZD496m Nov 6), 0.5780(NZD305m Nov 6) - BBG

- Tomorrow, the local calendar will see the RBNZ at the Select Committee to discuss the FinStab Report, and the Government will release its 3-Month Financial Statements.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

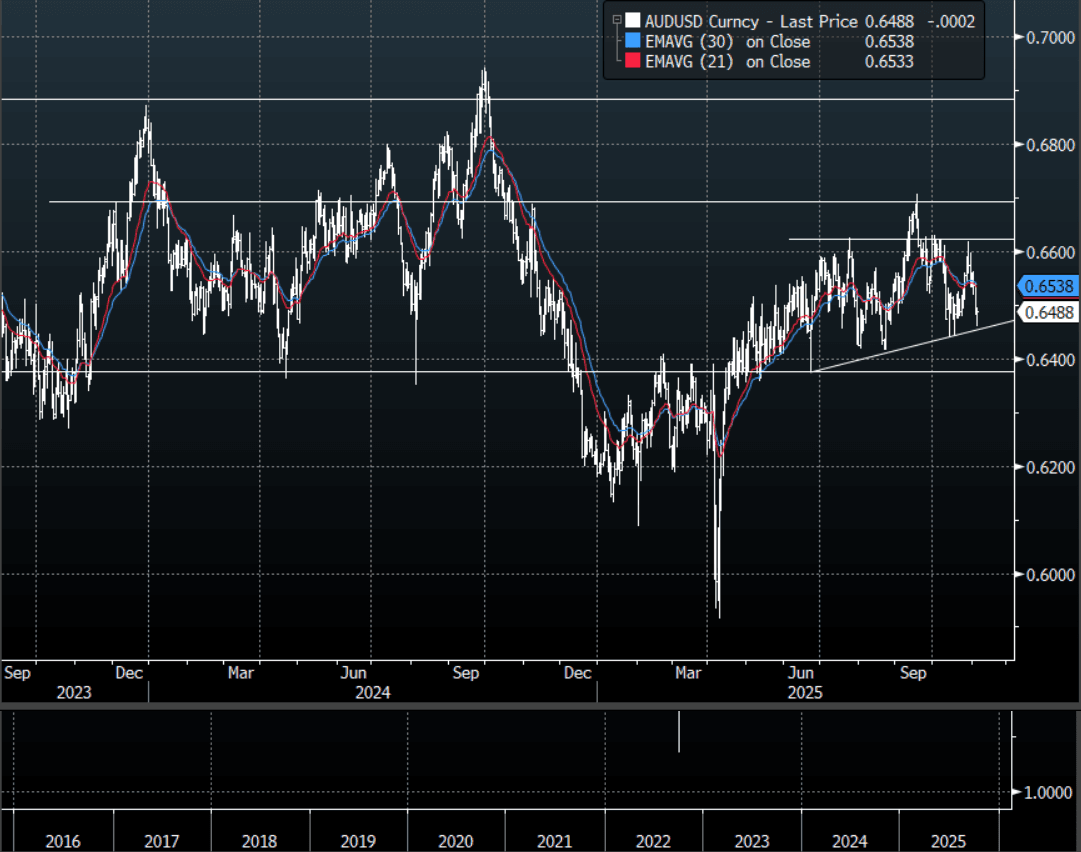

AUD: Asia-Pac: AUD/USD Tries Lower, Bounces Back With Risk

The AUD/USD has had a range today of 0.6459 - 0.6494 in the Asia- Pac session, it is currently trading around 0.6490, -0.02%. Asian stocks did not like how risk ended overnight and collapsed from the open keeping risk under pressure for most of our session. The AUD/USD fell away and the move gathered pace when it broke below the overnight lows, the panic has died down as we come into the afternoon session and some of these losses are being pared back. The AUD found some decent demand back toward its first support around 0.6450, though I suspect if this correction in risk has more to play out the AUD should now find sellers on a bounce back toward 0.6550 initially.

- The USD is starting to gain real momentum and the AUD has lagged this move helping it outperform in the crosses, should the support area around 0.6450 and then more importantly 0.6350 give way it could play catch up to the wider move.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6700(AUD 462m). Upcoming Close Strikes : 0.6500(AUD971m Nov 7), 0.6600(AUD560m Nov 6), 0.6600(AUD682m Nov 7) - BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Bloomberg Finance LP

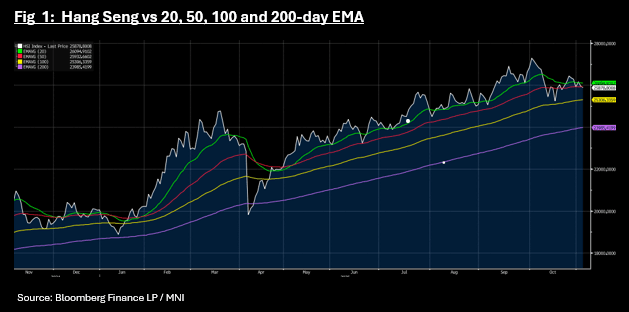

ASIA STOCKS: Tech Stocks Whacked, Dragging Bourses With Them

The correction in chip stocks that had been coming for some time appears to have turned up with key tech stocks down heavily, dragging regional bourses lower today. Key names like SK Hynix were down over 8% in the last two days, Samsung Tech over 9% and TSMC -2.5%. Key tech stocks in the region hit new all time highs Monday prior to the Korea Exchange taking the unusual step in issuing an investment warning about the excessive rally in SK Hynix. BBG estimates that their Asia tech index lost US$500bn in combined market capitalization in the fall.

- The Nikkei had been down over 4% earlier but staged a comeback after lunch to be 3% down.

- The KOSPI almost 6% on the prior day before a post lunch rally halved those losses, to be down by 3%.

- China's bourses were mixed with Shanghai and Shenzhen holding onto very modest gains, whist CSI 300 and Hang Seng are down modestly. The HSI is often more closely correlated to regional bourses. However it met a key resistance in its fall today, the 50-day EMA which possibly as a key resistance point, slowed its fall.

- The Jakarta Composite is bucking regional trends with a rally of +0.28% whilst the FTSE Malay KLCI fell -0.42%

- The NIFTY 50 continues to decline from its highs on Wednesday last week and has now fallen three of the four days since, opening today down -0.65%

OIL: Little Changed, Downside Pressure May Build If Risk Aversion Persists

Oil benchmarks sit little changed in the first part of Wednesday trade, somewhat on the sidelines, as broader risk trends in equities and crypto dominate. WTI was last near $60.50/bbl, with support still evident on moves sub $60.00/bbl at this stage. WTI futures remain in a corrective cycle for now though. Price recently traded through the 50-day EMA at $61.03, signaling scope for a stronger recovery, with sights on key resistance at $65.77, the Sep 26 high. Brent was close to $64.40/bbl in latest dealings. Since late Oct, support has been evident under the $64/bbl level.

- If the risk off move extends, oil may see more downside, as this may turn into broader global growth concerns. Inventory data already suggests near term oversupply is evident in the US.

- OPEC+ appears to be getting more mindful of further supply boosts post the weekend's modest increase for Q4 and pause into the first part of 2026.

- Still, demand concerns may keep a cap on prices until risk sentiment stabilizes/improves in the equity space.

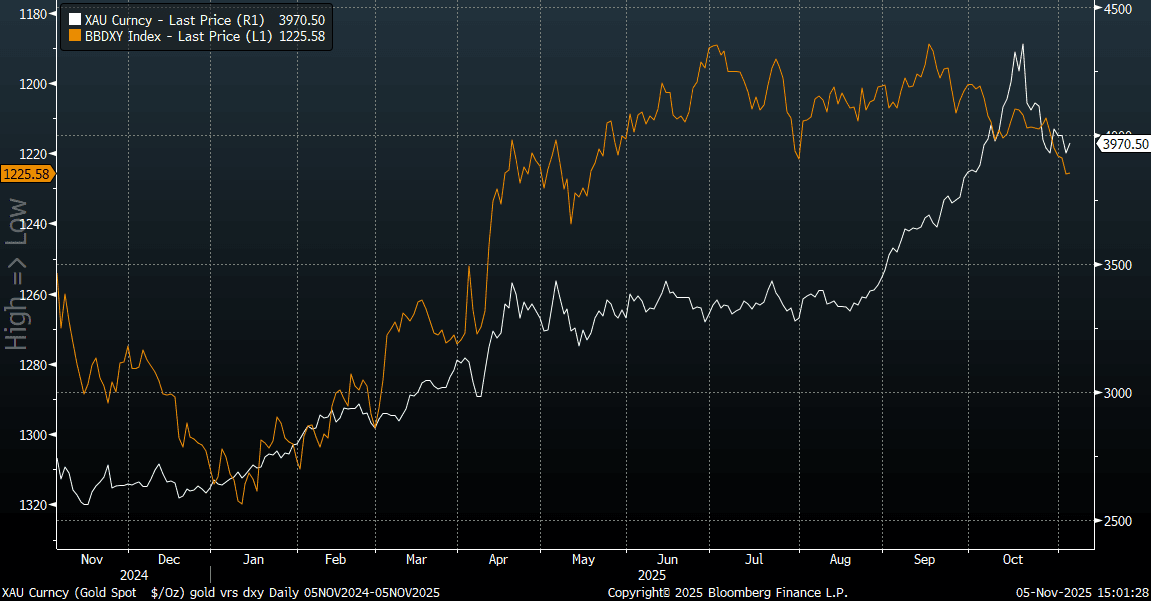

GOLD: Firms On Risk Aversion, Correlation With USD Eyed

Gold is tracking higher in latest dealings, last near $3970, up around 1% from end Tuesday levels. Focus from a technical standpoint, the retracement since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3864.7. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

- Gold support is likely emerging from the risk off tone in markets, although sentiment has stabilized as the session has progressed. US equity futures and bitcoin are comfortably up from earlier lows.

- The USD is also off earlier highs, the BBDXY last near 1225.6, after getting to 1226.35 earlier. This has also likely lent some support to gold as well.

- To the extent the market is still maintaining core long gold positions, this may limit the extent of gold upside, particularly if we see broader USD gains. The recent move lower in gold has coincided with some dollar stability, see the chart below. Note the BBDXY index is inverted on the chart.

Fig 1: Gold & USD BBDXY Index (Inverted) Trends

Source: Bloomberg Finance L.P./MNI

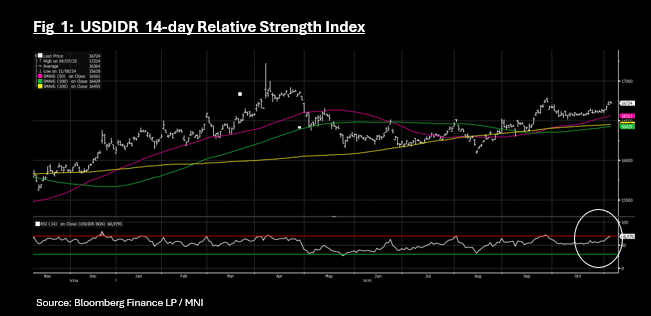

INDONESIA: 3Q GDP Beats Forecasts - Could Be the Boost Currency Needs

- Indonesia's 3Q GDP was ahead of expectations at 5.04% YoY (est 5.00%) and marginally down on 2Q result of 5.12%

- The 3Q QoQ result also topped expectations at 1.43%; though materially down on last quarter's result of 4.04%.

- This continues the run of improving data and provides the Central Bank with greater flexibility.

- The key issues for the economy remains the currency, which is weaker by 2.00% over the last 3 months, despite the BI surprising markets with a hold at their last meeting.

- Today's GDP when added to Monday's marginally higher October CPI (+2.86% vs est of 2.64% and prior of 2.65%) could see the BI on hold at their meeting on November 19.

- USDIDR hasn't reacted positively though, losing ground by -0.096% to 16,724 as the local equity markets are bucking regional trends with a rise of +0.30% and bond yields modestly higher.

- USDIDR remains north of all moving averages, and is now nearing oversold territory on the 14-day Relative Strength Index

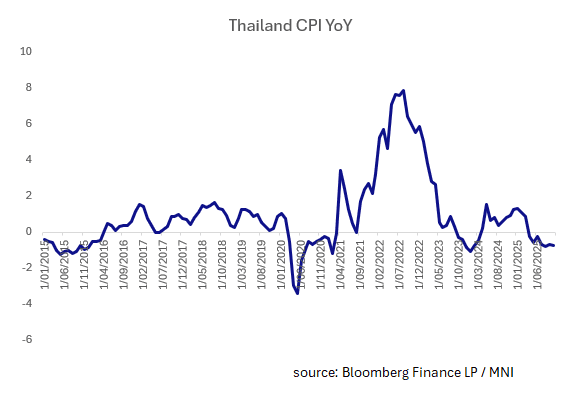

THAILAND: October CPI Turns Further Negative, Challenging BOT

- In worrying signs for the Thai economy, October's CPI printed more negative than the month prior.

- The October result of -0.76% YoY was the worst post- COVID result.

- CPI MoM was negative -0.11% MoM, from a prior month of -0.03%

- Core CPI rose +0.61% YoY from +0.65% YoY the month prior.

- The main driver for the decline has been the decline in the oil price with government subsidies driving prices lower too.

- The Bank of Thailand rate is currently at 1.50%, down from the post COVID high of 2.50%. The BOT would seem unlikely to want to cut rates further from here, particularly given the Baht has performed relatively well against regional peers over the last six months. However if the deflation becomes entrenched, the next meeting in December could be a live one for a rates decision.

MNI Preview: BNM On Hold As Easing Cycle Ends

Download Preview Here:

Summary Points

- Growth in Malaysia remains underpinned by resilient domestic demand, strong employment and wage growth

- Exports rebounded strongly in the September data, and have been surprisingly resilient for much of 2025 supported by the electronics upcycle.

- Malaysia has seen moderating inflation for most of this year, causing the Central Bank to reduce inflation forecast ranges. The CPI for September result of +1.5% is the first time CPI YoY has printed in line with the bottom end of the new range since the beginning of the year.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 05/11/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/11/2025 | 0745/0845 | * | Industrial Production | |

| 05/11/2025 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0830/0930 | *** | Riksbank Interest Rate Decison | |

| 05/11/2025 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0900/1000 | * | Retail Sales | |

| 05/11/2025 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 05/11/2025 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 05/11/2025 | 1000/1100 | ** | EZ PPI | |

| 05/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 05/11/2025 | 1315/0815 | *** | ADP Employment Report | |

| 05/11/2025 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 05/11/2025 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 05/11/2025 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 05/11/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 05/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 05/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 05/11/2025 | 1610/1610 | BOE Breeden At SALT Blockchain Event | ||

| 06/11/2025 | 2330/0830 | ** | average wages (p) | |

| 06/11/2025 | - | NorgesBank Meeting | ||

| 06/11/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 06/11/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 06/11/2025 | 0030/1130 | ** | Trade Balance | |

| 06/11/2025 | 0700/0800 | ** | Industrial Production | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0800/0900 | ** | Industrial Production | |

| 06/11/2025 | 0800/0900 | ** | Unemployment | |

| 06/11/2025 | 0810/0910 | ECB Schnabel At ECB Money Market Conference | ||

| 06/11/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/11/2025 | 0830/0930 | ECB De Guindos On Natixis Webinar | ||

| 06/11/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 06/11/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/11/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1230/1230 | BOE Press Conference | ||

| 06/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 06/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 06/11/2025 | 1330/0830 | ** | Preliminary Non-Farm Productivity |