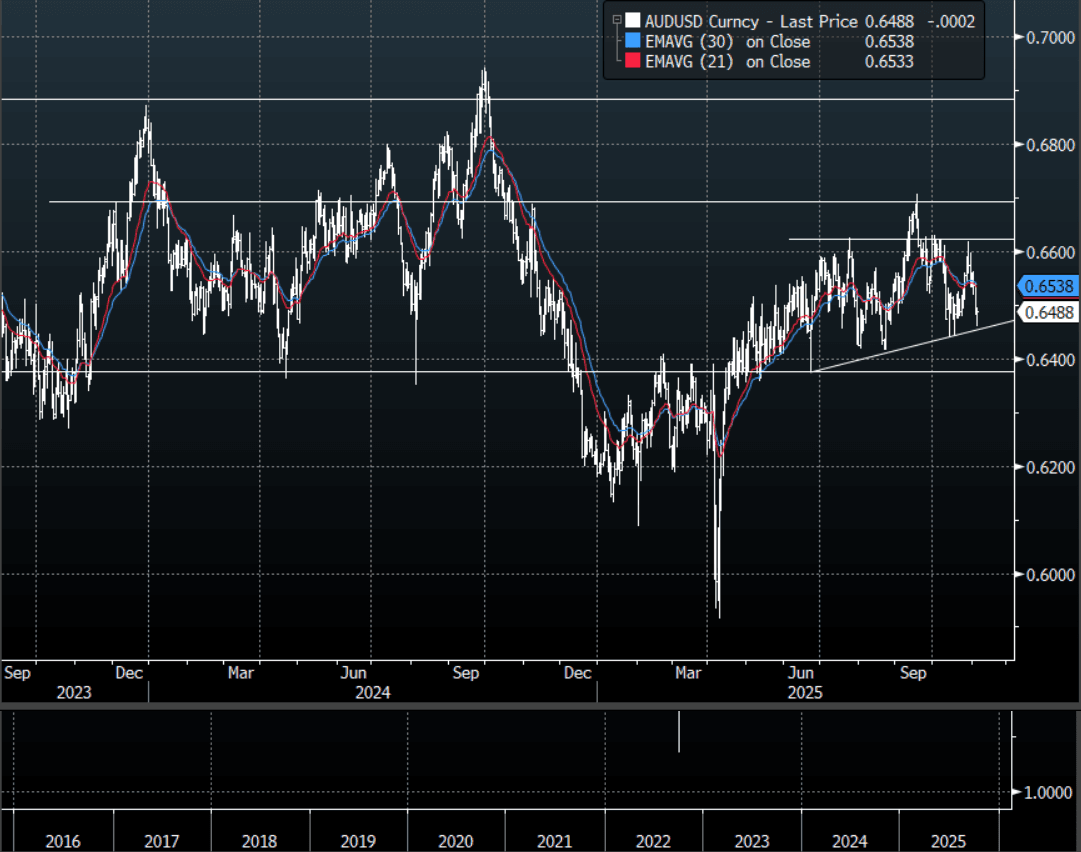

AUD: Asia-Pac: AUD/USD Tries Lower, Bounces Back With Risk

The AUD/USD has had a range today of 0.6459 - 0.6494 in the Asia- Pac session, it is currently trading around 0.6490, -0.02%. Asian stocks did not like how risk ended overnight and collapsed from the open keeping risk under pressure for most of our session. The AUD/USD fell away and the move gathered pace when it broke below the overnight lows, the panic has died down as we come into the afternoon session and some of these losses are being pared back. The AUD found some decent demand back toward its first support around 0.6450, though I suspect if this correction in risk has more to play out the AUD should now find sellers on a bounce back toward 0.6550 initially.

- The USD is starting to gain real momentum and the AUD has lagged this move helping it outperform in the crosses, should the support area around 0.6450 and then more importantly 0.6350 give way it could play catch up to the wider move.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6700(AUD 462m). Upcoming Close Strikes : 0.6500(AUD971m Nov 7), 0.6600(AUD560m Nov 6), 0.6600(AUD682m Nov 7) - BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Crude Relief Rally After Restrained OPEC Output Decision

Oil prices are higher during Monday’s APAC session after falling sharply last week. The move higher appears to be a relief rally following OPEC’s decision to increase November’s output 137kbd in line with October’s rise. There had been fears that it could have been substantially higher as the IEA is forecasting a record market surplus in 2026. WTI is up 1.6% to $61.85/bbl, close to the intraday high, and Brent is 1.5% higher at $65.48, after reaching $65.52. The USD index is up 0.3%.

- According to Bloomberg there were some dissenting views with Russia arguing that prices needed to be supported and Algeria that demand could weaken but Saudi arguing for a larger target increase.

- The group is trying to regain market share but most members have limited spare capacity except Saudi Arabia, and so the impact of output decisions on physical supply is unclear.

- The Fed’s Schmid speaks later on the economy and monetary policy, and also the ECB’s Lagarde, Lane and de Guindos appear. August euro area retail sales print.

US TSYS: Futures Lower, 10yr Might See Buyers Re-engage Around 4.20%

US Tsy futures hold weaker across the board 10yr last at 112-16+, -05. We remain above the 50-day EMA support point (112-12+) for 10yr futures, which will be watch on any further extension lower. The Sep move through this support zone proved to be a false break. The US Tsy cash curve has had a steepening bias, +56.5bps last. Spill over from a sharp steepening in the cash JGB curve (after Takaichi surprised and won the LDP leadership battle).

- Outside of government shutdown news, with seemingly little progress made over the weekend, focus will remain on what can be gleaned from private sector surveys/economy wide anecdotes. Focus later today may be on Trump administration government job lay offs.

- For US 10yr outright, we remain within recent ranges, last 4.14%, with broader 4.00-4.10% ranges holding. Buyers might re-emerge on any move back toward 4.20%, given on-going signs around labour market softness (with the Fed's Jefferson highlighting on Friday the jobs market is softening across a range of indicators) and how the Fed composition may change as we progress through 2026. Still, with elevated inflation pressures it is unlikely to be a sharp break lower on the downside, rather a steady grind.

- Looking ahead, there is no data scheduled or Fed speakers for Monday. Tuesday's Trade Balance & Import/Export data suspended due to the Gov shutdown. US Treasury supply kicks off Monday with $84B 13W & $75B 26W bill auctions (1130ET).

NZD: NZ$ Outperforming, AUDNZD Range Trading

The kiwi has outperformed the G10 today with NZDUSD up 0.1% to 0.5836, close to the intraday high at 0.5840, helped by stronger US equity futures even though the NZX was lower. The USD index is up 0.25%.

- While the RBNZ is unanimously expected to cut rates on Wednesday, analysts are split between 25bp and 50bp. The NZD OIS market has about a 50% chance of a 50bp move and around 62bp by year end.

- In contrast, the AUD OIS market has around a 50% chance of a 25bp rate cut by end-2025. This divergence has seen AUDNZD trend higher reaching 1.1418 on 30 September, when the RBA left rates unchanged. The pair has moved lower since then. Today it initially rose to 1.1351 but has range traded since then and is currently little changed at 1.1324.

- The S&P e-mini is up 0.3% and Nikkei +4.5% but NZX down 0.4%. A number of Asian markets are closed today with thin trading in Australia. Oil prices are higher with WTI +1.5% to $61.80/bbl. Copper is down 0.1%.

- The Fed’s Schmid speaks later on the economy and monetary policy, and also the ECB’s Lagarde, Lane and de Guindos appear. August euro area retail sales print.