AUSSIE BONDS: Solid Rally But AU-US10Y Diff Sits Near Top Of Range

ACGBs (YM +5.5 & XM +3.5) are stronger but off session bests. Today’s move leaves futures 4bps stronger than yesterday’s pre-RBA levels despite RBA Governor Bullock’s hawkish tone.

- Global bonds are benefiting from a general risk-off tone across markets, although there has been a bounce off lows.

- Cash US tsys are 1-2bps richer in today’s Asia-Pac session after yesterday’s modest rally.

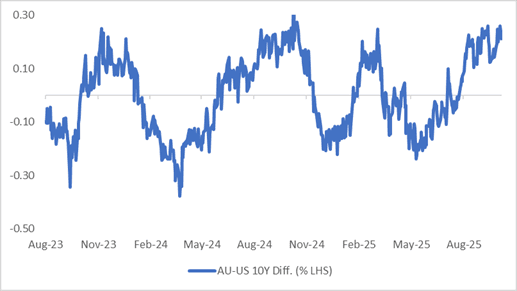

- Cash ACGBs are 4-5bps richer with the AU-US 10-year yield differential at +24bps. At this level, the spread remains near the upper end of the ±30bps range that has persisted since November 2022. (see chart)

- Today’s auction of the Mar-36 bond showed solid pricing for ACGBs, with the weighted average yield coming in 0.43bps below prevailing mid-yields, according to Yieldbroker. Moreover, the cover ratio nudged higher to 3.5167x from 3.4917x.

- The bills strip has bull-flattened across contracts, with pricing +1 to +6.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 15% probability, with a cumulative 11bps of easing priced by February 2026.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Curves Steeper, But Sub Recent Highs, 30yr Debt Auction Tomorrow

All the action today has away from the 10yr JGB, which has been fairly steady, last near 1.67%. The front end is weaker, back end firmer in yield terms as markets have moved to price in less BoJ hike risks, as well greater fiscal uncertainty. The 2/10s curve was last +76.5bps, +4.5bps for the session, while the 2/30s was +239bps, up 17bps.

- We noted earlier after the initial adjustment to Takaichi's victory, sentiment may stabilize and await cabinet announcements and early policy outcomes before taking the curve to fresh highs. The early Sep high for 2/30s was +245bps. The 30yr outright was last 3.30%, the 40yr 3.53%, while the 2yr was near 0.91%.

- These moves have largely been mirrored in the swap space, although yield moves haven't been as large at the back end (with JGBs likely more susceptible to fiscal policy concerns).

- BoJ tightening risk has fallen dramatically for Oct, with just 6bps of tightening priced in against recent highs of 17bps, as Takaichi stated the government and BoJ should be coordinated on economic policy. Takaichi has been a critic of BoJ hikes in the past (but her rhetoric wasn't as strong during this most recent LDP leadership campaign).

- JGB futures are back to flat, last 135.93, +.02, but well off earlier highs of 136.53.

- Note tomorrow, we get on the data front, Aug Household spending prints. Greater focus will be on 30yr dent auction, the first test for the new Takaichi regime.

FOREX: USD/JPY Testing Above 150.00, Options Volumes See 151-155.00 Strikes

Yen weakness has been the standout today, with USD/JPY breaking above 150.0, off 1.75% so far today for the session. The surprise Takaichi election win from Saturday's LDP leadership race has driven sentiment (with market odds of her victory very low on Friday per Polymarket). BoJ tightening risk has fallen dramatically for Oct just 6bps of tightening priced in against recent highs of 17bps), with Takaichi stating the government and BoJ should be coordinated on economic policy. Takaichi has been a critic of BoJ hikes in the past (but her rhetoric wasn't as strong during this most recent LDP leadership campaign).

- For USD/JPY technicals, a clean break above 150.00, will see focus shift to 150.92, the Aug 1 high and key resistance.

- Positioning focus will rest with asset managers and whether they go back a short position (with leveraged contracts already net short). Asset managers were last net long to the tune of +79.3k.

- The 1 month risk reversal is highs last -0.30, fresh highs back to 2022. So far today we have seen close to $7.4bn in options volumes go through in USD/JPY (63% of total volumes per DTCC on BBG). The larger volume transactions have been skewed towards USD/JPY calls with strikes in 151-155.00 region.

- USD/JPY looks too high relative to US-JP rate differentials, but further position adjustments could still play out in the near term.

- Elsewhere, EUR/USD is back slightly lower at 1.1720/25, with French politics likely to come back into focus.

- The kiwi has outperformed the G10 today with NZDUSD up 0.1% to 0.5836, close to the intraday high at 0.5840, helped by stronger US equity futures even though the NZX was lower.

- AUDUSD fell to 0.6582 in early trading as USDJPY rose following news that Japan’s conservative Takaichi won the LDP leadership. The pair has recovered to be up 0.1% to 0.6609, close to the intraday high of 0.6612, aided by better risk appetite with equities generally stronger. The USD index is 0.3% higher. BBDXY last near 1204.25.

OIL: Crude Relief Rally After Restrained OPEC Output Decision

Oil prices are higher during Monday’s APAC session after falling sharply last week. The move higher appears to be a relief rally following OPEC’s decision to increase November’s output 137kbd in line with October’s rise. There had been fears that it could have been substantially higher as the IEA is forecasting a record market surplus in 2026. WTI is up 1.6% to $61.85/bbl, close to the intraday high, and Brent is 1.5% higher at $65.48, after reaching $65.52. The USD index is up 0.3%.

- According to Bloomberg there were some dissenting views with Russia arguing that prices needed to be supported and Algeria that demand could weaken but Saudi arguing for a larger target increase.

- The group is trying to regain market share but most members have limited spare capacity except Saudi Arabia, and so the impact of output decisions on physical supply is unclear.

- The Fed’s Schmid speaks later on the economy and monetary policy, and also the ECB’s Lagarde, Lane and de Guindos appear. August euro area retail sales print.