INDONESIA: 3Q GDP Beats Forecasts - Could Be the Boost Currency Needs

- Indonesia's 3Q GDP was ahead of expectations at 5.04% YoY (est 5.00%) and marginally down on 2Q result of 5.12%

- The 3Q QoQ result also topped expectations at 1.43%; though materially down on last quarter's result of 4.04%.

- This continues the run of improving data and provides the Central Bank with greater flexibility.

- The key issues for the economy remains the currency, which is weaker by 2.00% over the last 3 months, despite the BI surprising markets with a hold at their last meeting.

- Today's GDP when added to Monday's marginally higher October CPI (+2.86% vs est of 2.64% and prior of 2.65%) could see the BI on hold at their meeting on November 19.

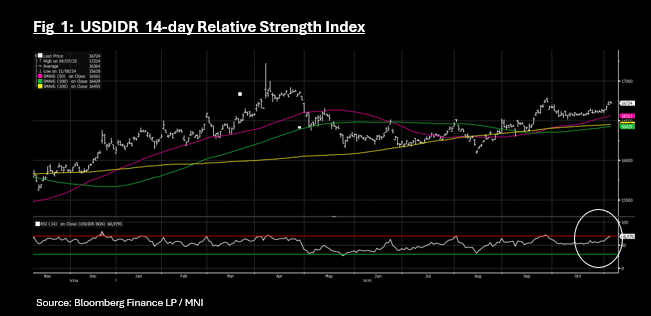

- USDIDR hasn't reacted positively though, losing ground by -0.096% to 16,724 as the local equity markets are bucking regional trends with a rise of +0.30% and bond yields modestly higher.

- USDIDR remains north of all moving averages, and is now nearing oversold territory on the 14-day Relative Strength Index

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD/JPY Testing Above 150.00, Options Volumes See 151-155.00 Strikes

Yen weakness has been the standout today, with USD/JPY breaking above 150.0, off 1.75% so far today for the session. The surprise Takaichi election win from Saturday's LDP leadership race has driven sentiment (with market odds of her victory very low on Friday per Polymarket). BoJ tightening risk has fallen dramatically for Oct just 6bps of tightening priced in against recent highs of 17bps), with Takaichi stating the government and BoJ should be coordinated on economic policy. Takaichi has been a critic of BoJ hikes in the past (but her rhetoric wasn't as strong during this most recent LDP leadership campaign).

- For USD/JPY technicals, a clean break above 150.00, will see focus shift to 150.92, the Aug 1 high and key resistance.

- Positioning focus will rest with asset managers and whether they go back a short position (with leveraged contracts already net short). Asset managers were last net long to the tune of +79.3k.

- The 1 month risk reversal is highs last -0.30, fresh highs back to 2022. So far today we have seen close to $7.4bn in options volumes go through in USD/JPY (63% of total volumes per DTCC on BBG). The larger volume transactions have been skewed towards USD/JPY calls with strikes in 151-155.00 region.

- USD/JPY looks too high relative to US-JP rate differentials, but further position adjustments could still play out in the near term.

- Elsewhere, EUR/USD is back slightly lower at 1.1720/25, with French politics likely to come back into focus.

- The kiwi has outperformed the G10 today with NZDUSD up 0.1% to 0.5836, close to the intraday high at 0.5840, helped by stronger US equity futures even though the NZX was lower.

- AUDUSD fell to 0.6582 in early trading as USDJPY rose following news that Japan’s conservative Takaichi won the LDP leadership. The pair has recovered to be up 0.1% to 0.6609, close to the intraday high of 0.6612, aided by better risk appetite with equities generally stronger. The USD index is 0.3% higher. BBDXY last near 1204.25.

OIL: Crude Relief Rally After Restrained OPEC Output Decision

Oil prices are higher during Monday’s APAC session after falling sharply last week. The move higher appears to be a relief rally following OPEC’s decision to increase November’s output 137kbd in line with October’s rise. There had been fears that it could have been substantially higher as the IEA is forecasting a record market surplus in 2026. WTI is up 1.6% to $61.85/bbl, close to the intraday high, and Brent is 1.5% higher at $65.48, after reaching $65.52. The USD index is up 0.3%.

- According to Bloomberg there were some dissenting views with Russia arguing that prices needed to be supported and Algeria that demand could weaken but Saudi arguing for a larger target increase.

- The group is trying to regain market share but most members have limited spare capacity except Saudi Arabia, and so the impact of output decisions on physical supply is unclear.

- The Fed’s Schmid speaks later on the economy and monetary policy, and also the ECB’s Lagarde, Lane and de Guindos appear. August euro area retail sales print.

US TSYS: Futures Lower, 10yr Might See Buyers Re-engage Around 4.20%

US Tsy futures hold weaker across the board 10yr last at 112-16+, -05. We remain above the 50-day EMA support point (112-12+) for 10yr futures, which will be watch on any further extension lower. The Sep move through this support zone proved to be a false break. The US Tsy cash curve has had a steepening bias, +56.5bps last. Spill over from a sharp steepening in the cash JGB curve (after Takaichi surprised and won the LDP leadership battle).

- Outside of government shutdown news, with seemingly little progress made over the weekend, focus will remain on what can be gleaned from private sector surveys/economy wide anecdotes. Focus later today may be on Trump administration government job lay offs.

- For US 10yr outright, we remain within recent ranges, last 4.14%, with broader 4.00-4.10% ranges holding. Buyers might re-emerge on any move back toward 4.20%, given on-going signs around labour market softness (with the Fed's Jefferson highlighting on Friday the jobs market is softening across a range of indicators) and how the Fed composition may change as we progress through 2026. Still, with elevated inflation pressures it is unlikely to be a sharp break lower on the downside, rather a steady grind.

- Looking ahead, there is no data scheduled or Fed speakers for Monday. Tuesday's Trade Balance & Import/Export data suspended due to the Gov shutdown. US Treasury supply kicks off Monday with $84B 13W & $75B 26W bill auctions (1130ET).