MNI EUROPEAN MARKETS ANALYSIS: Waiting for FED, Markets Mixed

- A relatively subdued end to the week with markets fixated on upcoming Central Bank actions from the FED and the BOJ. This comes as the RBI in India cut rates by 25bps as expected, before announcing a massive bond buying and FX swap program.

- In worrying signs ahead of a potential rate hike, Japanese households are paring back spending for the first time in months according to the latest data.

- National Economic Council Director Kevin Hassett's voice is growing louder as he predicted a cut by the FED of 25bps at the upcoming meeting.

- Ahead for markets is German Manufacturing Orders, France and Italy Industrial Production and Italian Retail Sales and in the US University of Michigan Surveys and Consumer Credit.

MARKETS

US TSYS: Early Gains Moderate, Front End Yields Lower with 10-Yr Flat

Earlier gains for bond futures moderated in the afternoon, with the US 10-Yr bond future. The 10-Yr had rising by +04 earlier but now +02 in the Asia afternoon at 112-25+. TYH6 has upper resistance from the 50-day EMA of 112-27+ which it failed to break earlier.

Cash is given back earlier gains also withe the 10-Yr now flat on the day, having been down -1bps at midday.

- The 2-Yr is down -0.4bps at 3.521%

- The 5-Yr is down -0.3bps at 3.671%

- The 10-Yr is flat at 4.10%

- The 30-Yr is up +0.3bps at 4.759%

- Tonight's focus for issuance will be a 6,13 and 26 week bills as well as a 3-Yr US$58bn note auction.

- Key data for bond markets tonight in the US will be Personal Income/Spending, PCE Prices, Univ of Mich Sentiment/Current Conditions/Expectations and Inflation expectations.

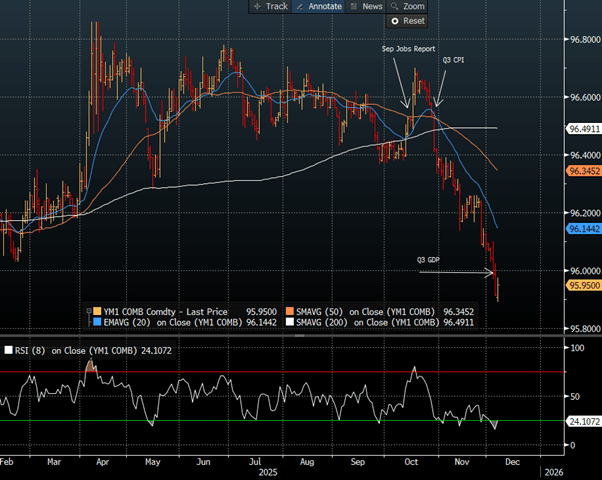

JGBS: Twist-Flattener As 30YY Extends Post-Supply Decline, Dec Hike At 89%

JGB futures are little changed, +4 compared to settlement levels, after a relatively subdued session.

- "Based on recent developments in corporate earnings, wage negotiations, the yen's depreciation in the FX market, and dialogue with the government, it has become increasingly clear that the BOJ is gaining confidence in raising rates at the upcoming December meeting," BofA economist Takayasu Kudo says in a note. The economist expects the BOJ to raise rates in June 2026, followed by hikes in January and July 2027. DJ via BBG

- BOJ-dated OIS currently assigns an 89% probability to a 25bp hike in December, rising to 104% by March 2026. As recently as 21 November, markets saw less than a 20% chance of a December move. Notably, investors are now pricing in more than two 25bp hikes by October 2026.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest sell-off.

- Cash JGBs have twist-flattened across benchmarks, with yields 0.5bp higher to 5bps lower. The benchmark 10-year yield is 0.7bp lower at 1.934% versus the cycle high of 1.941%, set yesterday.

- Swaps have also twist-flattened, with rates 1bp higher to 5bps lower.

- On Monday, the local calendar will see Cash Earnings, Q3 GDP (F), BoP Current Account Balance and Bank Lending.

Source: Bloomberg Finance LP

AUSSIE BONDS: Respite After A Heavy Week & Even Heavier November

ACGBs (YM +4.0 & XM +1.5) are stronger after a heavy and an extremely heavy November (see chart).

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest sell-off.

- Cash ACGBs are 2bps lower to 1bp higher, with the AU-US 10-year yield differential at +59bps.

- The bills strip has bull-flattened, with pricing flat to +3.

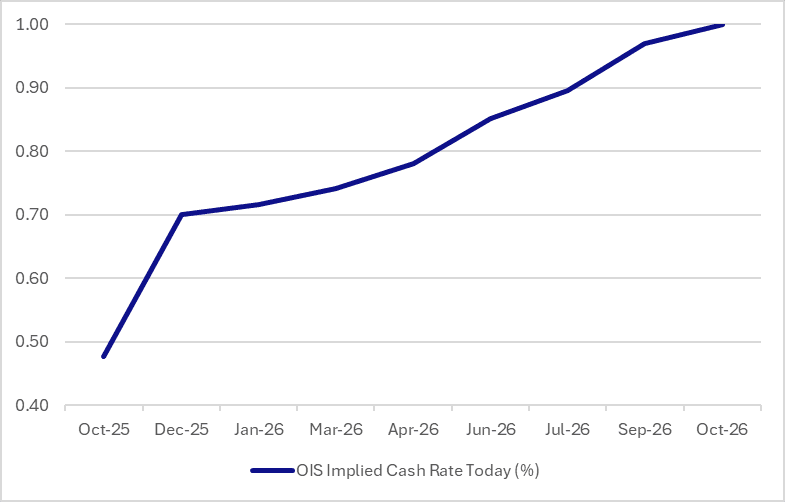

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 3% for December to 104% by September and 121% by December 2026.

- Tomorrow, the local calendar will be empty on Monday, ahead of NAB Business Confidence and the RBA Policy Decision on Tuesday.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Monday and A$1000mn of the 1.00% 21 December 2030 bond on Wednesday.

- GlobalCapital – “Australian semi-governments look set to increase their issuance of euro-denominated bonds in 2026 after the first prints by the new group of issuers were well received by SSA investors this year. QTC in May became the first Aussie semi-government to print a public euro benchmark with a €1bn 10 year deal. Four months later, TCV followed with a €2bn 15-year print.” – via BBG

Bloomberg Finance LP

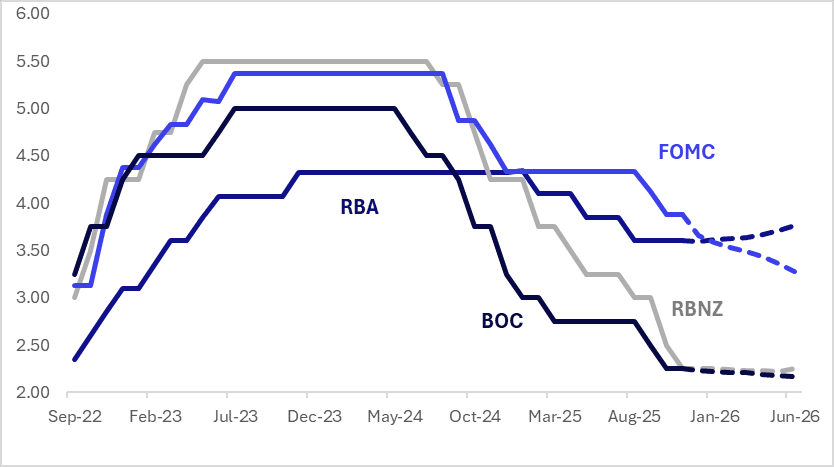

STIR: $-Bloc Pricing Firmer Over The Past Week, Led By AUS

Interest rate expectations across the $-bloc firmed over the past week out to June 2026, led by Australia (+15bps). Canada rose 6bps, while New Zealand and the US edged higher by 2bps and 3bps, respectively.

- The main events were in Australia, with the release of Q3 GDP on Wednesday and October Household Spending on Thursday.

- Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details were a lot stronger than the headline, with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022. The softer GDP print was due to a 0.5pp inventory detraction, the largest since Q2 2023, which may reflect stronger demand driving a drawdown and which may be followed by a rebuild.

- October household spending was another piece of data signalling robust domestic demand in Australia after Q3 showed it rose 1.2% q/q. With Governor Bullock saying yesterday that the output gap has likely closed, this strength on the demand side is another reason for the RBA to be on hold beyond the 9 December decision, given that inflation is above the top of the band.

- The next key regional events are the RBA meeting on 9 December, followed by the FOMC and BoC on 10 December. RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 3% for December to 96% by September and 120% by December 2026.

- The market assigns just a 4% chance of a cut by the BoC, while the US market is 92% priced for a 25bp cut in December.

- Looking ahead to June 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.29%, -59bps; Canada (BOC): 2.17%, -9bp; Australia (RBA): 3.77%, +17bps; and New Zealand (RBNZ): 2.28%, +3bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

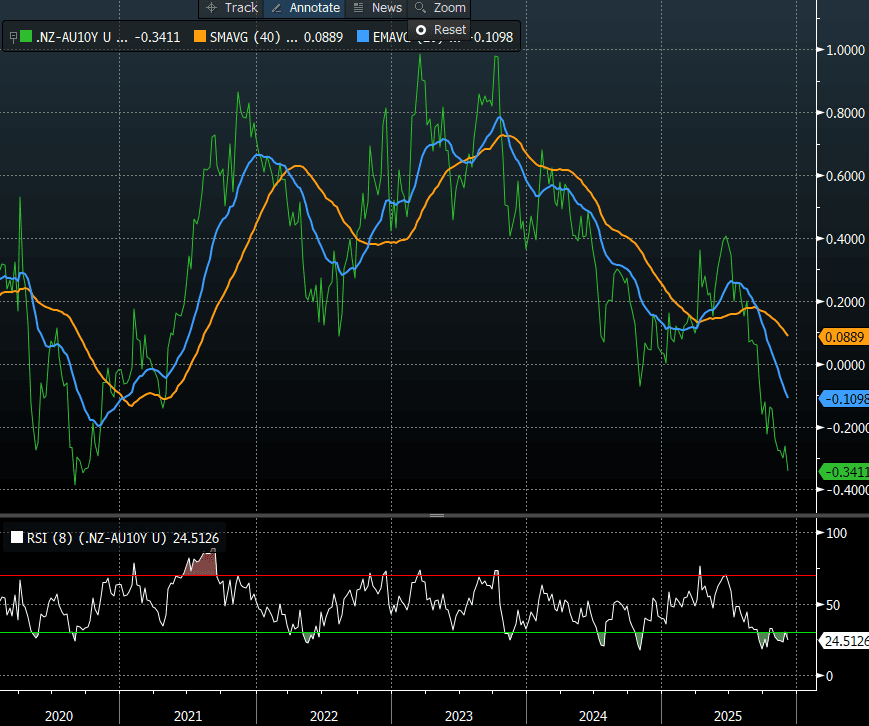

BONDS: NZGBS: Bear-Steepener But NZ-AU 10Y Diff Still Near Cycle Low

NZGBs closed showing a bear-steepener, with benchmark yields flat to 6bps higher.

- On a relative basis, NZGBs also had a tough day with the NZ-US and NZ-AU 10-year yield differentials 5bps wider. Nevertheless, the NZ-AU differential remains near its lowest since 2020 (see chart).

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday’s modest sell-off.

- Friday's US Calendar: Personal Income/Outlays, UofM Consumer Survey. Non-Farm payrolls are not released tomorrow, but are rescheduled for December 16.

- NZ total new lending increased to NZ$14.59 billion in October from NZ$14.29 billion in September, according to data from the RBNZ. – MTN via BBG

- Swap rates closed 3-6bps higher, with implied short-end swap spreads wider.

- RBNZ-dated OIS pricing closed slightly firmer across meetings. 1bps of easing is priced for February, while November 2026 assigns 33bps of tightening.

- Interest rate expectations across the $-bloc firmed over the past week out to June 2026, led by Australia (+15bps). Canada rose 6bps, while NZ and the US edged higher by 2bps and 3bps, respectively.

- Tomorrow, the local calendar will be empty until next Wednesday, when RBNZ Governor Breman hosts a media Q+A alongside Net Migration data.

Bloomberg Finance LP

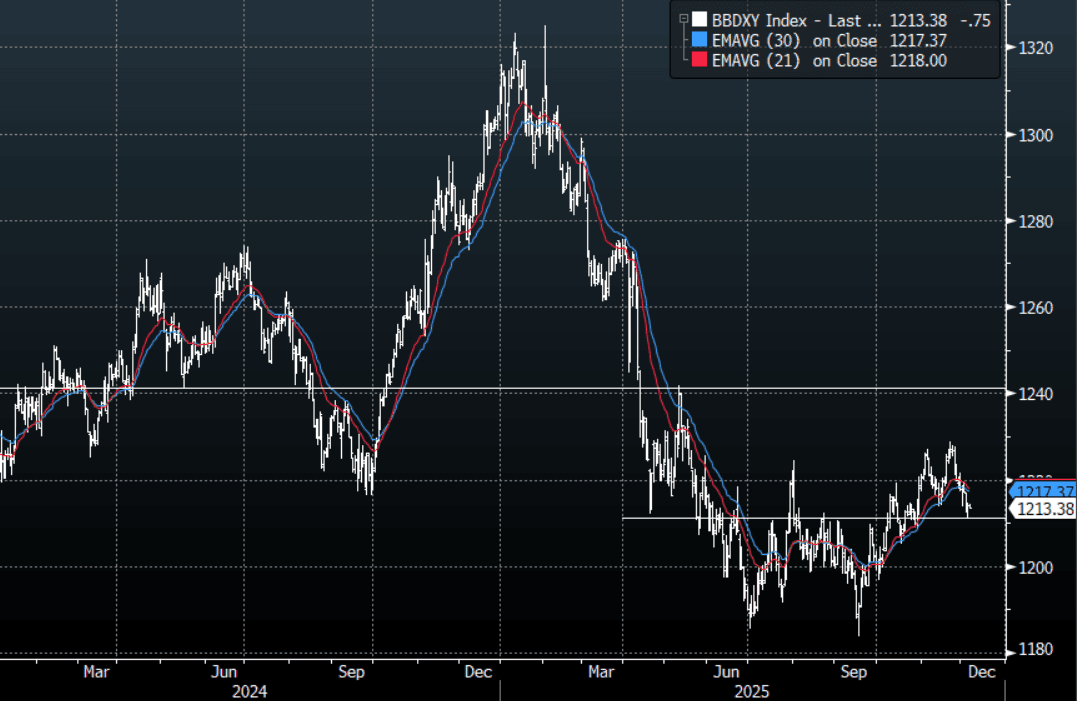

FOREX: USD - BBDXY Slightly Lower In Asia

The BBDXY has had a range today of 1213.22 - 1214.35 in the Asia-Pac session; it is currently trading around 1213, -0.05%. The USD has traded slightly softer in the Asian session as the PBOC did not push back as hard today in the CNY fix. Some key inflation data out of the US tonight should be the driver of price, the market will be focused on PCE tonight after mixed jobs data over the course of the week. The USD saw decent demand back toward the 1210 area and it looks like the range 1210-1230 is here to stay for the moment. On the day look for resistance again back towards the 1216-1218 area where sellers should remerge initially, support remains toward 1210 initially and then the more important 1205 area.

- EUR/USD - Asian range 1.1641-1.1654, Asia is currently trading 1.1650. The pair stalled overnight and was unable to break through the 1.1680 area overnight. On the day it looks like we might consolidate ahead of the US inflation data. Look for dips back toward 1.1580-1600 to be supported initially looking to retest the 1.1680 area again.

- GBP/USD - Asian range 1.3321-1.3334, Asia is currently dealing around 1.3330. The pair did not like it up back towards the 1.3400 area. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3260-1.3290 area, while above here look for the market to retest the 1.3350-70 area again at some point.

- Cross asset : SPX +0.20%, Gold $4215, US 10-Year 4.092%, BBDXY 1213, Crude Oil $59.52

- Data/Events : EZ Household Cons/GDP, Germany Factory Orders, France Trade Balance/ Industrial Production/Manufacturing Production, Spain Industrial Production, Italy Retail sales

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

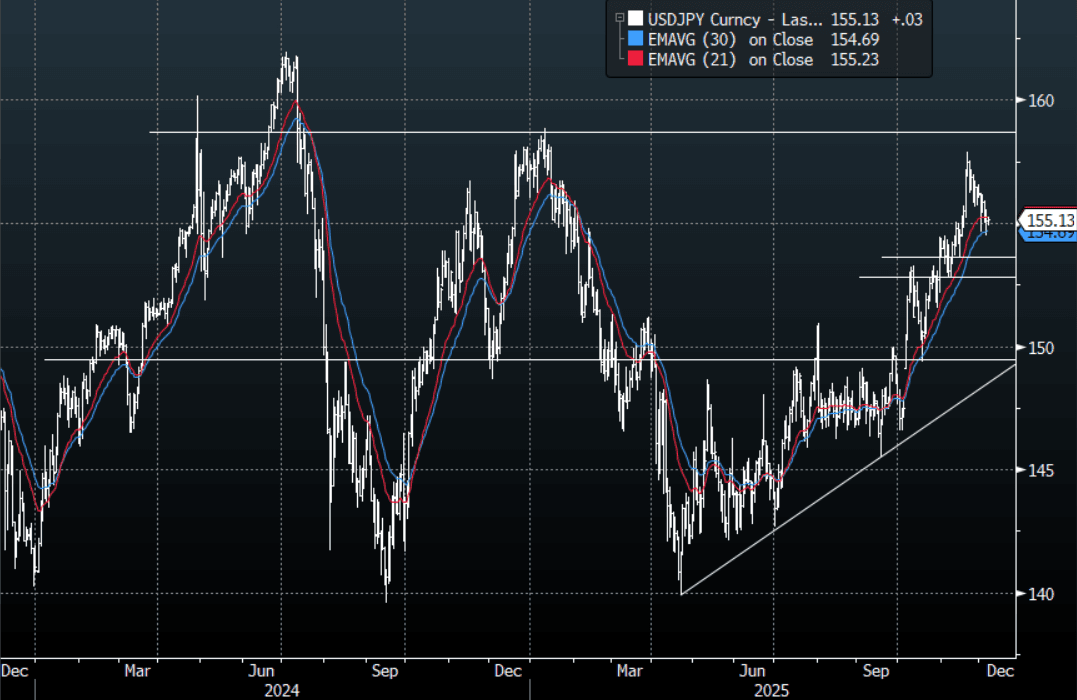

JPY: USD/JPY - Consolidates Around 155.00

The USD/JPY range today has been 154.92 - 155.23 in the Asia-Pac session, it is currently trading around 155.15, +0.05%. The pair has consolidated around the 155.00 area in a quiet session. The market is pricing in the fact that the Yen move looks like it could force the BOJ into action in December. This has stalled the upward momentum and should keep it contained in the short-term but I suspect the market will still look for opportunities to express a long USD at the right levels. Technically USD/JPY is still in an uptrend with the first big support back toward the 153-155 area which should see buyers reemerge. In today's Asian session I suspect we will continue to consolidate within a wider 154.50-156.00 range.

- Some key inflation data out of the US tonight should be the driver of price, the market will be focused on PCE tonight after mixed jobs data over the course of the week.

- Bloomberg - “Japan household spending unexpectedly fell 3% in October from a year earlier, a sign of fragile domestic demand as the BOJ prepares to consider raising rates.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($1.94b), 157.00($895m). Upcoming Close Strikes : 155.00($1.22b Dec 8 ), 156.00($1.49b Dec 8 ), 156.00($740m Dec 10) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 88 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

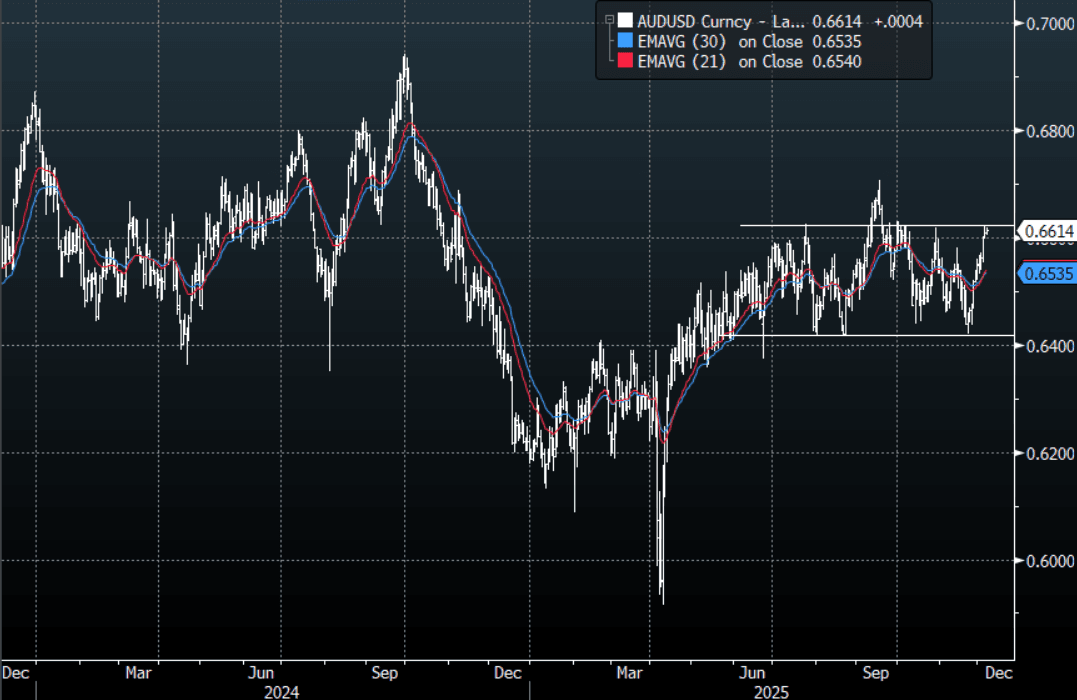

AUD/USD - Holds Above 0.6600, Looking To Test 0.6630

The AUD/USD has had a range today of 0.6605 - 0.6618 in the Asia- Pac session, it is currently trading around 0.6615, +0.05%. The AUD/USD continued to consolidate above 0.6600 in a quiet Friday session. There was not the same pushback by the PBOC today on the China fix so the USD traded slightly softer. The AUD price action remains very constructive and indicative of a market with solid buying interest. On the day, I suspect dips back toward the 0.6560-0.6580 area should continue to be supported. The AUD is now looking to build some momentum to once again test the top end of its recent range, a break of 0.6630 is needed to look toward the 0.6700 area.

- MNI: Future RBA Adjustments Seen As Minor Tweaks To 3.6% Rate. Any adjustment to the Reserve Bank of Australia’s cash rate would only be a minor policy tweak rather than a fundamental shift and would likely be driven by short-term inflation pressures in 2026, former RBA economists told MNI.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD1.11b), 0.6600(AUD487m). Upcoming Close Strikes : 0.6475(AUD814m Dec 8 ) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 34 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

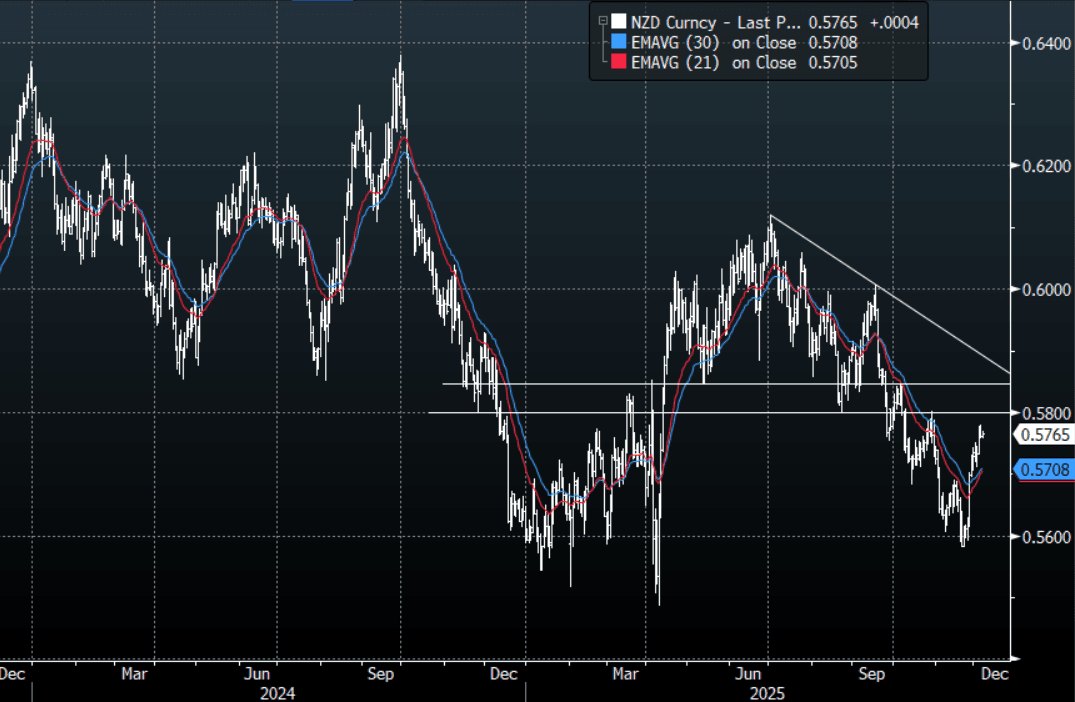

NZD/USD - Consolidates Above 0.5750, Eyes The 0.5800-50 Area

The NZD/USD had a range today of 0.5758-0.5770 in the Asia-Pac session, going into the London open trading around 0.5765, +0.10%. The NZD/USD has drifted a little higher today in a quiet session. There was not the same pushback by the PBOC today on the China fix so the USD traded slightly softer. On the day, look for support now back towards the 0.5730-0.5750 area as the focus turns back to the more important 0.5800-50 resistance where I suspect sellers could return initially.

- Some key inflation data out of the US tonight should be the driver of price, the market will be focused on PCE tonight after mixed jobs data over the course of the week.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD332m). Upcoming Close Strikes : 0.5670(NZD382m Dec 8 ), 0.5700(NZD557m Dec 10), 0.5730(NZD692m Dec 8 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 34 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Asia Stocks Showing Signs that Rally is Faltering

Asian equities were mixed Friday as the FED decision gets closer, and concerns continue to grow for a BOJ rate rise, causing the NIKKEI to fall. The KOSPI is holding onto strong gains for the week as the AI / tech rally is supported by upcoming government policy on dividends. A surge in the share price for China's chipmaker Moore Threads in its trading debut sees tech investors assessing valuations of China's tech compared to Japan and Korea. India's Central Bank the RBI cut rates as expected whilst reducing their outlook for inflation and moving to neutral with their outlook for rates. Following the impact of US data overnight on bonds, eyes turn tonight back to US economic releases following Labour Market data overnight as markets look to firm up pricing for a cut.

- The NIKKEI is down -1.40% today and is barely clinging onto a weekly gain as the KOSPI roared again up by 1% and over 3.6% for the week.

- China's bourses are mixed with the Hang Seng down -0.25% today and flat for the week whilst the CSI 300 is up marginally and holding onto a 0.50% weekly gain. Shenzhen and Shanghai are up but on track for a weekly fall.

- The NIFTY 50 is up marginally post the RBI by +0.20% yet remains down -0.3% for the week with profit taking driving things following recent new highs in place.

- SE Asia's major bourses have delivered positive gains for the week with yet again the Jakarta Comp leading the way with gains of +1.7%, with the SE Thai +1.7% and FTSE Malay KLCI up +0.50%.

ASIA STOCKS: Taiwan and India Have Strong Outflows

- Equity flows in the region continue to be dominated by sizeable outflows. Taiwan's Flows yesterday turned strongly negative leaving total flows for the last 5 trading days barely positive. India's outflows continue to be challenged with another sizeable outflow on the December 3.

- The risk remains into year end that flows out of equities may persist in those markets where the run up in AI / Tech stocks have been significant. Some key AI stocks in Korea for example are up over 200% from the lows of April with concerns raised of bubble like conditions

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 50 | -386 | -6284 |

| Taiwan (USDmn) | -858 | 47 | -7059 |

| India (USDmn)* | -390 | -207 | -16159 |

| Indonesia (USDmn) | -7 | -137 | -1803 |

| Thailand (USDmn) | 39 | 39 | -3363 |

| Malaysia (USDmn) | 14 | -24 | -4646 |

| Philippines (USDmn) | -32 | -73 | -705 |

| Total (USDmn) | -1184 | -740 | -40018 |

| * Data Up To 03 DEC |

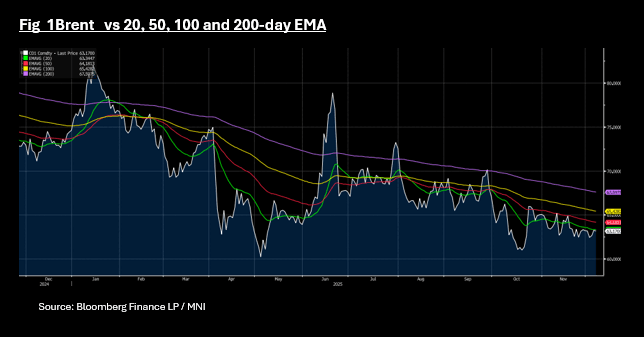

Oil Down After Strong Week, Brent Fails Key Tech Level

- Both WTI and Brent failed to follow on from overnight gains and are down moderately in the Asia trading day.

- WTI is down -0.33% to US$59.52, yet remains up over 1.5% for the week in its best week for a month.

- Brent is down -0.29% to US$63.17 yet nearing flat on the week. With gains overnight Brent was near the 20-day EMA of 63.34 only to turn away with moderate falls today.

- As the Ukraine and Russia talks appeared stalled, with Putin emphasizing that several points in the US backed peace plan were unacceptable, when added to news price cuts were enough to support prices for a second day.

- OPEC+ had affirmed over the weekend a previous decision to pause production increases in the first quarter of next year, citing a period of weaker seasonal demand during winter months across much of Asia, Europe and North America and following that Saudi Arabia cut the price of its flagship crude grade to the lowest level in five years, amid persistent signs of a surplus in global oil markets. (source BBG)

- The Trump administration extended a waiver for Lukoil PJSC's gas stations outside of Russia, allowing them to continue operations until late April 2026 (source BBG)

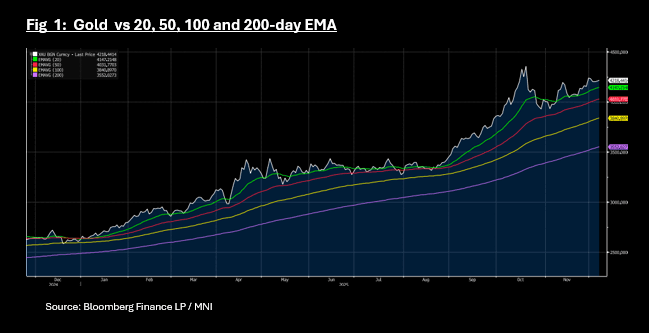

Gold Down for Week, Awaits FED

- Gold is up +0.20% Friday at US$4,215.95 yet on track for moderate falls of around -0.50% for the week after last week's significant gains. Gold traders attention will remain firmly on the probabilities for a rate cut as the economic data flow continues between now and the FED.

- Gold remains just over 3% below the October high of US$4,356.30 and sits above all major moving averages, with the 20-day EMA below at US$4,147.20

- Having ended October weaker, Gold has rebounded since with a strong rally yet evidence suggests that ETF buying has been the driver and that potentially CB banks may be behind the recent run. (source BBG)

- For the first time in 15-Years a new underground gold mine opened yesterday in South Africa, with the South African company West Wits Mining opening of the Qala Shallows project. (source BBG)

INDIA: RBI Cuts Rate, Signals End to Easing

- Repo Rate Cut: The RBI reduced the key interest rate by 25 basis points to 5.25%, bringing the cumulative reduction in the 2025 financial year to 125 basis points. This decision followed previous rate cuts earlier in the year.

- Economic Outlook: Whilst India's economy showed strength in the first half of FY26 with 8.2% GDP growth in the July-September quarter, some sectors like manufacturing are showing signs of moderating, as tariffs continue to impact the economy.

- Inflation: CPI was a mere +0.25% in October yet the RBI cautioned about potential increases in inflation in the fourth quarter of FY26 and first quarter of FY27 due to base effects, food prices and demand.

- Risk assessment: The decision balances growth support with vigilance over inflation and external risks. The MPC will continue monitoring the macroeconomic landscape

- Bonds have rallied on the news with the 4-Yr down -4bps to 6.09% and the 10-Yr down -2bps to 6.49%.

INDIA: RBI to Purchase INR1 tn of Bonds, Enter FX $5bn FX Swap

- In a bid to support liquidity, the RBI announced a bond purchase of up to INR1 trillion and a 3-Year USD/INR FX swap of $5 billion.

- The announcements come as a broader approach to improving liquidity and Rupee stability .

- The additional aim is to reduce borrowing costs for the Modi government as it follows with its aggressive growth plans.

- The OMO and FX-swap announcement comes alongside a cut in the policy repo rate by 25 basis points to 5.25%, and a “neutral” stance from the Monetary Policy Committee.

- The central bank said the liquidity measures — OMO + swap — are “to provide sufficient durable liquidity to the banking system,” especially given currency-in-circulation dynamics, forex operations, and reserve maintenance

- Bonds are rallying with the IGB 10-Yr down -4bps to 6.474% and the 4-Yr down 5bps to 6.082%

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 05/12/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/12/2025 | 0730/0730 | DMO to publish issuance calendar for FQ4 | ||

| 05/12/2025 | 0745/0845 | * | Industrial Production | |

| 05/12/2025 | 0745/0845 | * | Foreign Trade | |

| 05/12/2025 | 0800/0900 | ** | Industrial Production | |

| 05/12/2025 | 0900/1000 | * | Retail Sales | |

| 05/12/2025 | 1000/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/12/2025 | 1330/0830 | *** | Labour Force Survey | |

| 05/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 05/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 05/12/2025 | 1500/1000 | *** | Personal Income and Consumption | |

| 05/12/2025 | 1510/1610 | ECB Lane in Panel at CEPR Paris Symposium | ||

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 2000/1500 | * | Consumer Credit |