INDIA: RBI to Purchase INR1 tn of Bonds, Enter FX $5bn FX Swap

- In a bid to support liquidity, the RBI announced a bond purchase of up to INR1 trillion and a 3-Year USD/INR FX swap of $5 billion.

- The announcements come as a broader approach to improving liquidity and Rupee stability .

- The additional aim is to reduce borrowing costs for the Modi government as it follows with its aggressive growth plans.

- The OMO and FX-swap announcement comes alongside a cut in the policy repo rate by 25 basis points to 5.25%, and a “neutral” stance from the Monetary Policy Committee.

- The central bank said the liquidity measures — OMO + swap — are “to provide sufficient durable liquidity to the banking system,” especially given currency-in-circulation dynamics, forex operations, and reserve maintenance

- Bonds are rallying with the IGB 10-Yr down -4bps to 6.474% and the 4-Yr down 5bps to 6.082%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: TYZ5 Fails to Hold Above Key Tech Level (amended)

Bond futures took the overnight lead and rallied strongly in the morning session, but failed to hold above a key technical, falling back in the afternoon. TYZ5 is up +0.04 at 112-29+, after a high of 113-02+ earlier, just above the 20-day EMA of 113-01+ only to retreat in afternoon trade.

Cash has been strong also with yields 1-2bps lower across the curve.

- The 2-Yr fell -1.6bps to 3.561%

- The 5-Yr is down -1.7bps at 3.68%

- The 10-Yr is lower by -1.6bps at 4.072%

- The 30-Yr is down -1bps at 4.657%.

The bond market has been starved of data but will get some non-government led releases tonight in the ADP Employment Change (consensus 30k; prior -32k) S&P Global US Services PMI (forecast 55.2; prior 55.2) and ISM Services Index (forecast 50.8; prior 50.0).

For issuance, the focus tonight remains on bill issuance with a US$95bn 6-week bill auction ahead of the US Treasury Quarterly Funding announcement.

MNI EXCLUSIVE: An Advisor On PBoC's Funding Of Tech Firms

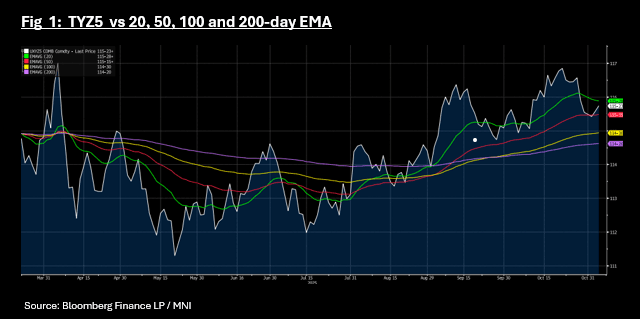

US TSYS: TYZ5 Bounces from Key Tech Level, Gives Back Early Gains

Bond futures took the overnight lead and rallied strongly in the morning session, but failed to hold above a key technical, falling back in the afternoon. TYZ5 is up +0.05 at 115-23+, after a high of 115-29+ earlier, just above the 20-day EMA of 115-28+.

Cash has been strong also with yields 1-2bps lower across the curve.

- The 2-Yr fell -1.6bps to 3.561%

- The 5-Yr is down -1.7bps at 3.68%

- The 10-Yr is lower by -1.6bps at 4.072%

- The 30-Yr is down -1bps at 4.657%.

The bond market has been starved of data but will get some non-government led releases tonight in the ADP Employment Change (consensus 30k; prior -32k) S&P Global US Services PMI (forecast 55.2; prior 55.2) and ISM Services Index (forecast 50.8; prior 50.0).

For issuance, the focus tonight remains on bill issuance with a US$95bn 6-week bill auction ahead of the US Treasury Quarterly Funding announcement.