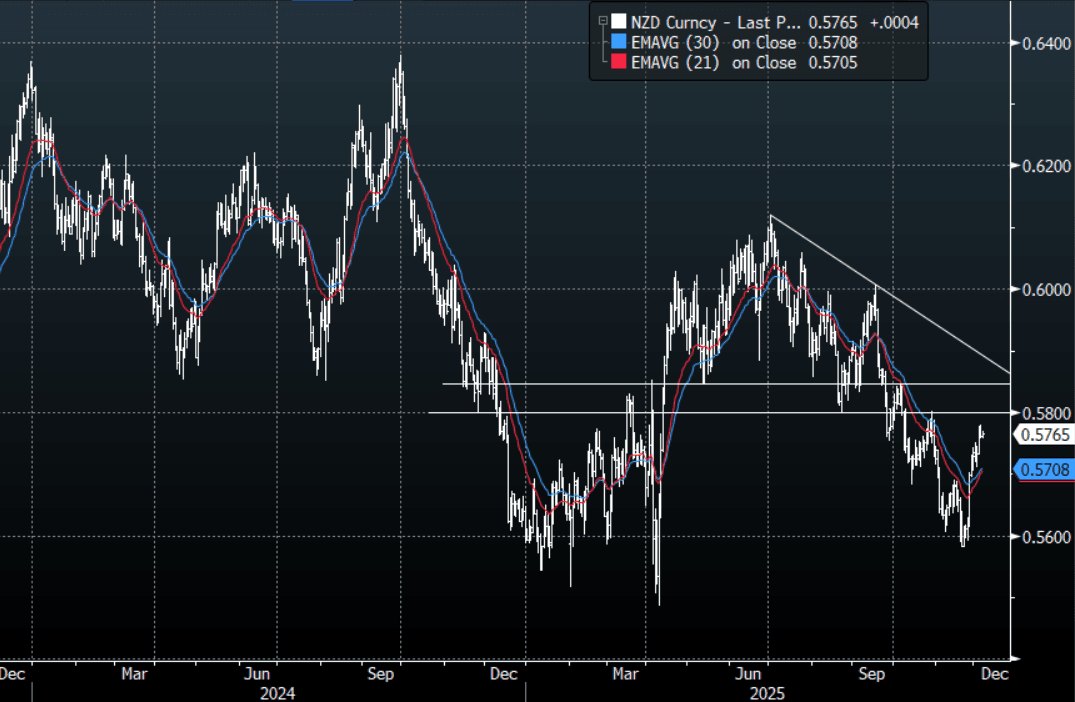

NZD: NZD/USD - Consolidates Above 0.5750, Eyes The 0.5800-50 Area

The NZD/USD had a range today of 0.5758-0.5770 in the Asia-Pac session, going into the London open trading around 0.5765, +0.10%. The NZD/USD has drifted a little higher today in a quiet session. There was not the same pushback by the PBOC today on the China fix so the USD traded slightly softer. On the day, look for support now back towards the 0.5730-0.5750 area as the focus turns back to the more important 0.5800-50 resistance where I suspect sellers could return initially.

- Some key inflation data out of the US tonight should be the driver of price, the market will be focused on PCE tonight after mixed jobs data over the course of the week.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD332m). Upcoming Close Strikes : 0.5670(NZD382m Dec 8 ), 0.5700(NZD557m Dec 10), 0.5730(NZD692m Dec 8 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 34 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: Risk Sentiment Stabilizes After Early Sharp Losses, US Session Eyed

Broader risk sentiment stabilized somewhat in recent dealings. US equity futures were last off around 0.15-0.30%, comfortably up from earlier lows, with Eminis supported sub 6750 so far today. Bitcoin got under $100k, but is now back above this level. Earlier lows were just under 99k, with focus on support in the 90-95k region ( a break below this level could signal a deeper correction). There hasn't been a catalyst for this stabilization, with dips buyers potentially emerging after the extent of today's sell-off (particularly for the Asia time zone). The US session later this evening will be a key litmus test for broader risk appetite.

- For Eminis, session lows at 6748.5 will be in focus, while beyond that the 50-day EMA around 6705 is another potential support point. Since early May, moves towards this or just below have been supported.

- Regional equities are also up from session lows. The Kospi was down 6% at one stage, but now sits back at -2.5%, the index back above 4000. Japan equities remain down around 3%, while the Taiex is off 1.4%, with tech sensitive countries remaining in focus.

- Elsewhere, AUD/USD is back to flat, while NZD/USD is slightly higher now, while yen gains have also been pared. AUD/USD got to lows of 0.6459, but is now back at 0.6490/95, NZD was last at 0.5655. AUD/JPY got close to 98.80, but is now around 99.60/65. USD/JPY was last near 153.50.

- US Tsy yields are still down but away from session lows, the 10yr around 4.07% (session lows were at 4.05%). Further risk off is likely to see fresh safe haven demand, which could bring the 4.00% level back into focus.

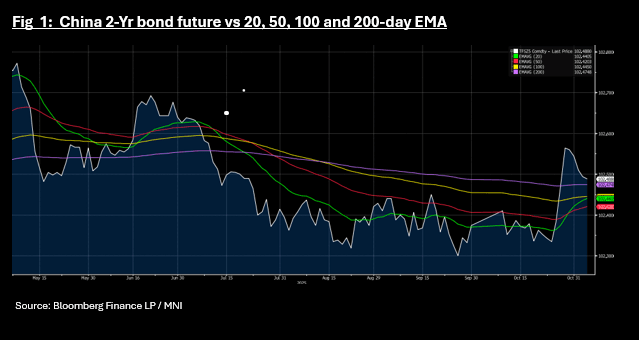

CHINA: Bond Futures Lower 2-Yr Near Key Technical

- As the PBOC withdrew liquidity for a third successive day, bond futures are lower whilst bond yields grind lower.

- The 10-Yr bond future is lower by -0.03 at 108.605 to retain its position above all major moving averages, whilst moving away from overbought on the 14-day RSI

- The 2-Yr is down -0.01 at 102.48 and it too retains it position above all major moving averages, though is now near to the 200-day EMA of 102.47.

- The CGB 10-Yr is marginally lower in yield at 1.791%

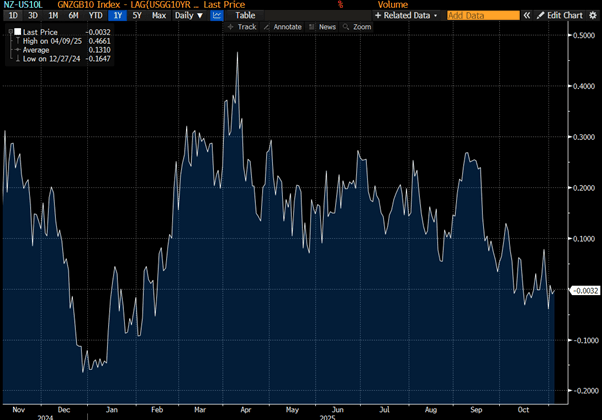

BONDS: NZGBS: Richer But NZ-US10Y Diff Wider

NZGBs closed 2-3bps richer, but with the NZ-US 10-year yield differential 2bps wider at +2bps. (see chart)

- NZ's jobless rate held steady at 5.3% in the third quarter, matching economist expectations. Employment was unchanged quarter-on-quarter, compared with a revised 0.2% fall in the previous quarter, while employment declined 0.6% year-on-year, a smaller drop than in the second quarter. The labour force participation rate was 70.3%.

- Average hourly earnings rose 0.7% from the previous quarter, and non-government wages increased 0.4% including overtime and 0.5% for ordinary time.

- Swap rates are 2-3bps lower, with the 2-year rate rejecting off the 20-day EMA.

- RBNZ dated OIS pricing is slightly softer across meetings. 26bps of easing is priced for November, with a cumulative 33bps by February 2026.

- Tomorrow, the local calendar will see the RBNZ at the Select Committee to discuss the FinStab Report, and the Government will release its 3-Month Financial Statements.

- Also tomorrow, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP