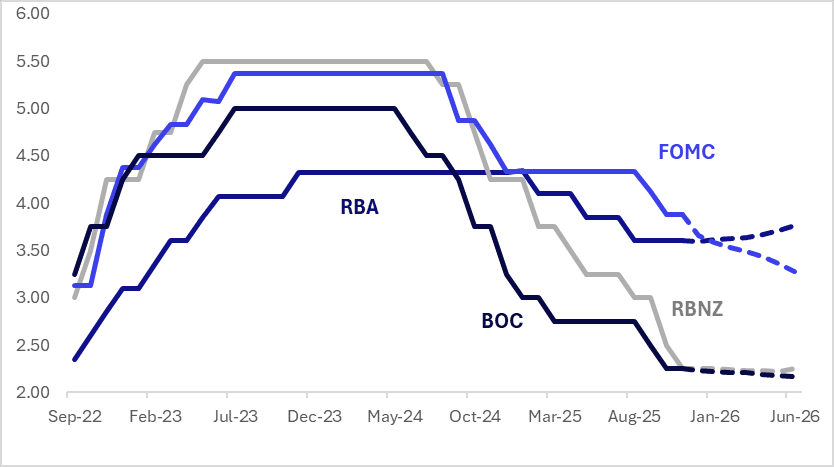

STIR: $-Bloc Pricing Firmer Over The Past Week, Led By AUS

Interest rate expectations across the $-bloc firmed over the past week out to June 2026, led by Australia (+15bps). Canada rose 6bps, while New Zealand and the US edged higher by 2bps and 3bps, respectively.

- The main events were in Australia, with the release of Q3 GDP on Wednesday and October Household Spending on Thursday.

- Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details were a lot stronger than the headline, with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022. The softer GDP print was due to a 0.5pp inventory detraction, the largest since Q2 2023, which may reflect stronger demand driving a drawdown and which may be followed by a rebuild.

- October household spending was another piece of data signalling robust domestic demand in Australia after Q3 showed it rose 1.2% q/q. With Governor Bullock saying yesterday that the output gap has likely closed, this strength on the demand side is another reason for the RBA to be on hold beyond the 9 December decision, given that inflation is above the top of the band.

- The next key regional events are the RBA meeting on 9 December, followed by the FOMC and BoC on 10 December. RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 3% for December to 96% by September and 120% by December 2026.

- The market assigns just a 4% chance of a cut by the BoC, while the US market is 92% priced for a 25bp cut in December.

- Looking ahead to June 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.29%, -59bps; Canada (BOC): 2.17%, -9bp; Australia (RBA): 3.77%, +17bps; and New Zealand (RBNZ): 2.28%, +3bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

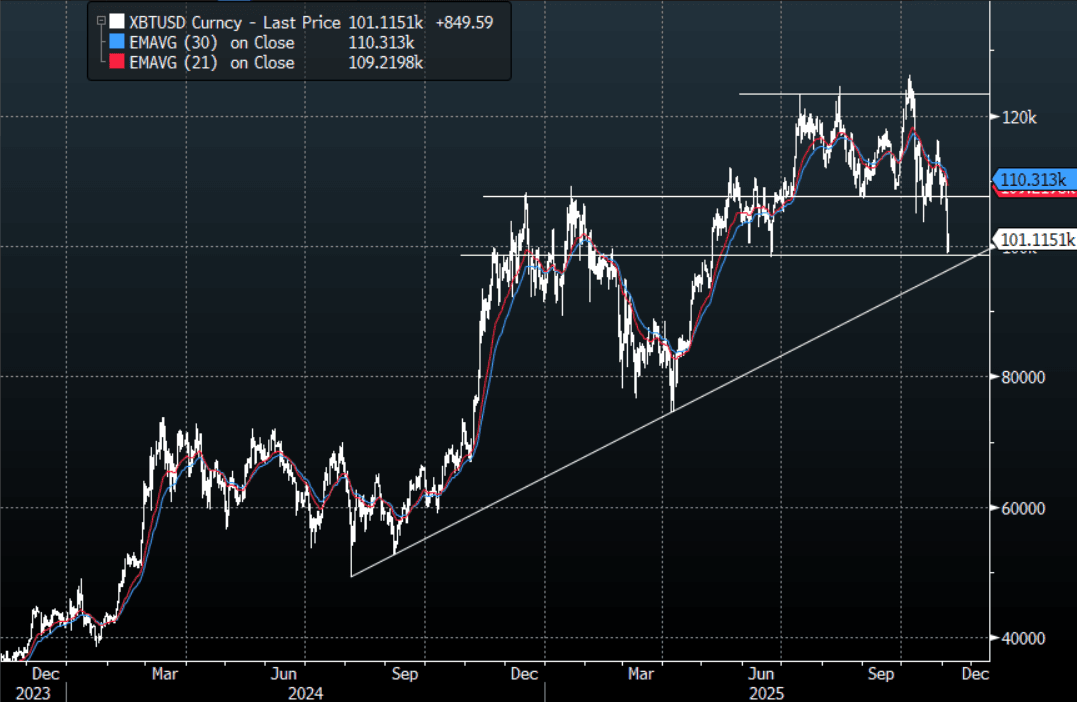

CRYPTO: Bitcoin - Has A Look Below 100k, The 90k-95K Support Is Pivotal

Bitcoin had a range overnight of $98 913.02k - $104 910k, Asia is currently trading around $101 100k, +0.75%. Bitcoin took another leg lower overnight down over 7% on the day as the Crypto space seems to be struggling with a resurgent Dollar and a reversal in the risk backdrop. The Bitcoin support area between $95k-$107k is being tested and should provide those wanting to express a long a good opportunity to fade if that's your way. A break below $90k-$95k though would potentially signal a deeper correction is underway, this scenario would make a few of those treasury companies holding bitcoin on their balance sheet nervous, there are reports that some of these have already started paring back positioning.

- _Checkmate on X pointed out that “ Treasury Companies are starting to sell their coins. This is good to see. The forest fire of bad ideas needs to sweep through and clear out all of this dead wood.” - https://sequans.com/sequans-redeems-50-of-convertible-debt-through-strategic-asset-reallocation/

- Vijay Boyapati agreed with the sentiment “I've been warning about this all year (see various pods I've been on). Most Treasuries will face shareholder pressure to sell BTC and buy their shares when their mNAV dips meaningfully below 1. Saylor is probably the one exception, but even he may face legal pressure.”

Fig 1: Bitcoin spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

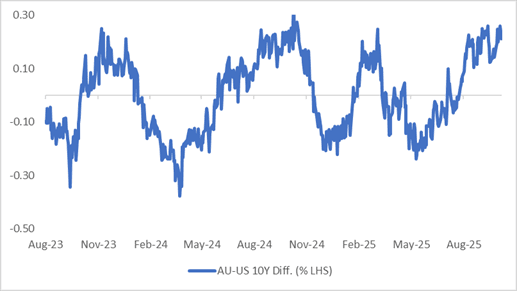

AUSSIE BONDS: A Strong Day For ACGBs But AU-US10Y Diff Sits Near Top Of Range

Cash ACGBs are 5–7bps richer on the day, while the AU–US 10-year yield differential is little changed at +24bps.

- At this level, the spread remains near the upper end of the ±30bps range that has persisted since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is close to fair value.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has increased around 75bps since June to be around the same level as October 2024.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

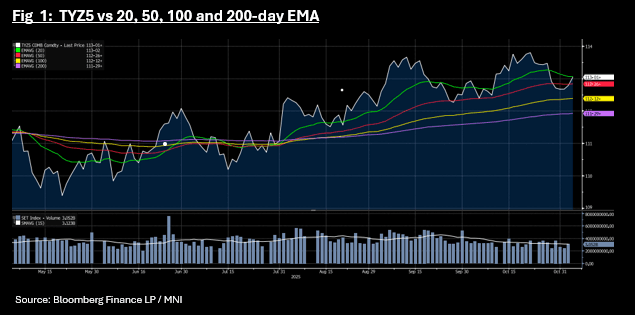

US TSYS: Rally Continues, TYZ5 Approaches Key Technical

Overnight moves in Treasuries spilled over into Asia today with bond futures stronger and yields lower. The 10-Yr bond future is up +08 at 113-01+ taking it near to the 20-day EMA of 113-02+. It has traded below since just prior to the last FED where for some observers, the December rate cut became uncertain. The boost for bonds overnight came from the weakening in equities on profit taking.

Cash has opened up very strong with yields across the curve -3 - 3.5bps lower. The 2s10s curve has flattened modestly.

- The 2-Yr is at 3.549 (-2.9bps)

- The 5-Yr is at 3.663% (-3.5bps)

- The 10-yr is at 4.054% (-3.1bps)

- The 30-Yr is at 4.642% (-2.4bps)

Equity weakness is a key theme for markets today with major markets down and recent star performers like the KOSPI and NIKKEI down over 4% as the tech sector is hit hard. The warning from the Korea Exchange yesterday on SK Hynix was an indicator as to how far these tech stocks have run and were long overdue a correction.