AUSSIE BONDS: Respite After A Heavy Week & Even Heavier November

ACGBs (YM +4.0 & XM +1.5) are stronger after a heavy and an extremely heavy November (see chart).

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest sell-off.

- Cash ACGBs are 2bps lower to 1bp higher, with the AU-US 10-year yield differential at +59bps.

- The bills strip has bull-flattened, with pricing flat to +3.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 3% for December to 104% by September and 121% by December 2026.

- Tomorrow, the local calendar will be empty on Monday, ahead of NAB Business Confidence and the RBA Policy Decision on Tuesday.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Monday and A$1000mn of the 1.00% 21 December 2030 bond on Wednesday.

- GlobalCapital – “Australian semi-governments look set to increase their issuance of euro-denominated bonds in 2026 after the first prints by the new group of issuers were well received by SSA investors this year. QTC in May became the first Aussie semi-government to print a public euro benchmark with a €1bn 10 year deal. Four months later, TCV followed with a €2bn 15-year print.” – via BBG

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: Risk Sentiment Stabilizes After Early Sharp Losses, US Session Eyed

Broader risk sentiment stabilized somewhat in recent dealings. US equity futures were last off around 0.15-0.30%, comfortably up from earlier lows, with Eminis supported sub 6750 so far today. Bitcoin got under $100k, but is now back above this level. Earlier lows were just under 99k, with focus on support in the 90-95k region ( a break below this level could signal a deeper correction). There hasn't been a catalyst for this stabilization, with dips buyers potentially emerging after the extent of today's sell-off (particularly for the Asia time zone). The US session later this evening will be a key litmus test for broader risk appetite.

- For Eminis, session lows at 6748.5 will be in focus, while beyond that the 50-day EMA around 6705 is another potential support point. Since early May, moves towards this or just below have been supported.

- Regional equities are also up from session lows. The Kospi was down 6% at one stage, but now sits back at -2.5%, the index back above 4000. Japan equities remain down around 3%, while the Taiex is off 1.4%, with tech sensitive countries remaining in focus.

- Elsewhere, AUD/USD is back to flat, while NZD/USD is slightly higher now, while yen gains have also been pared. AUD/USD got to lows of 0.6459, but is now back at 0.6490/95, NZD was last at 0.5655. AUD/JPY got close to 98.80, but is now around 99.60/65. USD/JPY was last near 153.50.

- US Tsy yields are still down but away from session lows, the 10yr around 4.07% (session lows were at 4.05%). Further risk off is likely to see fresh safe haven demand, which could bring the 4.00% level back into focus.

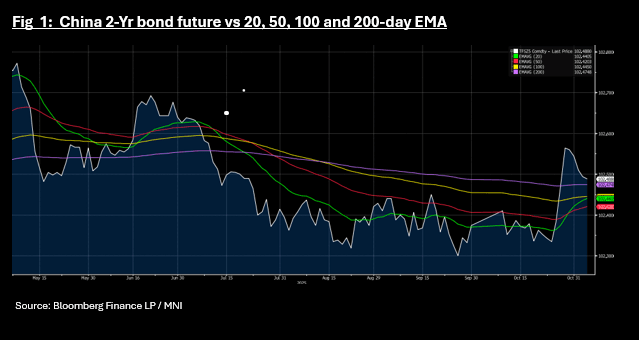

CHINA: Bond Futures Lower 2-Yr Near Key Technical

- As the PBOC withdrew liquidity for a third successive day, bond futures are lower whilst bond yields grind lower.

- The 10-Yr bond future is lower by -0.03 at 108.605 to retain its position above all major moving averages, whilst moving away from overbought on the 14-day RSI

- The 2-Yr is down -0.01 at 102.48 and it too retains it position above all major moving averages, though is now near to the 200-day EMA of 102.47.

- The CGB 10-Yr is marginally lower in yield at 1.791%

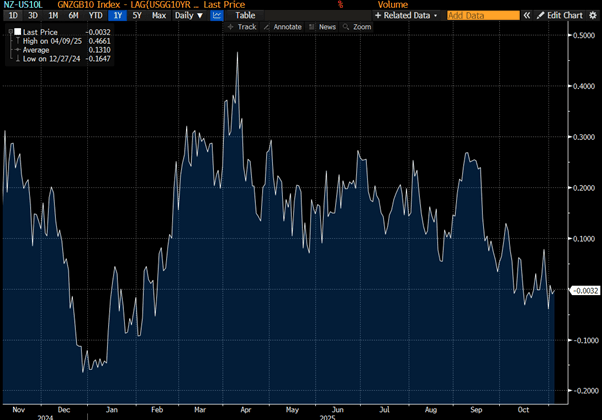

BONDS: NZGBS: Richer But NZ-US10Y Diff Wider

NZGBs closed 2-3bps richer, but with the NZ-US 10-year yield differential 2bps wider at +2bps. (see chart)

- NZ's jobless rate held steady at 5.3% in the third quarter, matching economist expectations. Employment was unchanged quarter-on-quarter, compared with a revised 0.2% fall in the previous quarter, while employment declined 0.6% year-on-year, a smaller drop than in the second quarter. The labour force participation rate was 70.3%.

- Average hourly earnings rose 0.7% from the previous quarter, and non-government wages increased 0.4% including overtime and 0.5% for ordinary time.

- Swap rates are 2-3bps lower, with the 2-year rate rejecting off the 20-day EMA.

- RBNZ dated OIS pricing is slightly softer across meetings. 26bps of easing is priced for November, with a cumulative 33bps by February 2026.

- Tomorrow, the local calendar will see the RBNZ at the Select Committee to discuss the FinStab Report, and the Government will release its 3-Month Financial Statements.

- Also tomorrow, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP