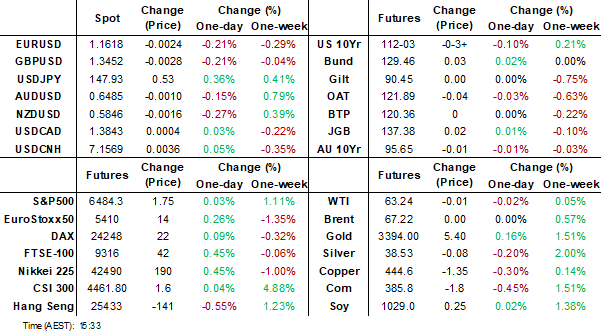

MNI EUROPEAN MARKETS ANALYSIS: USD Recovers Ground

- The USD has been supported in the first part of Wednesday trade. We are heading into corporate month-end and this could explain the market's reticence to press the USD lower as we could see some USD demand potentially over today and tomorrow.

- US Tsy yields are a touch higher, while Aussie bond yields were supported by a firmer July CPI print. The A$ initially rallied but had no follow through.

- China equities continue to rally, while industrial profits pared the rate of y/y decline in July.

- Later the Fed’s Barkin repeats comments previously given. The data calendar is light with only September German GfK consumer confidence of note. Markets are waiting for US PCE price data on Friday.

MARKETS

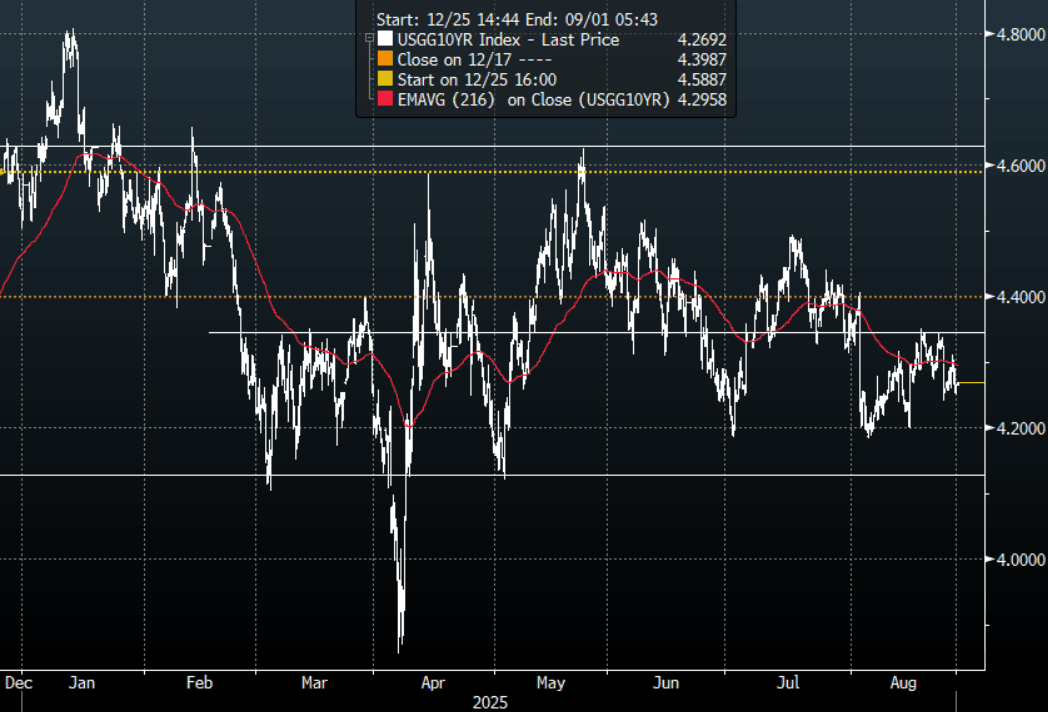

The TYU5 range has been 112-03+ to 112-05+ during the Asia-Pacific session. It last changed hands at 112-04, down 0-02+ from the previous close.

- The US 2-year yield has edged lower trading around 3.6557%, down 0.02 from its close.

- The US 10-year yield has moved higher trading around 4.267%, up 0.01 from its close.

- This has seen the 2s10s steepen in Asia, +2.30 at 60.347.

- 10-Year Yields found buyers above 4.30% again overnight. While the 4.35% area continues to hold, bounces should be met with demand, with the 30-Year taking the brunt of the selling related to challenging the Fed independence. First target is the recent lows around 4.18% then the bottom of the range towards 4.10% comes back into focus.

- Andrew Ackerman on X: “The Fed has deferred any decision on Cook's status because they are expecting a quick decision from a court on Cook's coming request for a judicial order/TRO, according to a Fed official. Would note the Fed has no board meetings scheduled for this week, while Cook is in limbo.”

- ISABELNET on X: “10Y Yield: When the Fed prioritizes the labor market over inflation, it can reduce the immediate risk of recession by sustaining employment. However, this is likely to increase inflation expectations and push yields higher”

- RenMac on X: “Consumers see increasing slack in the jobs market. The Labor Differential continues to soften, falling to a fresh low of 9.7 in August. In particular, we saw a notable jump in those saying “jobs hard to get.” See Fig.1 Below

- Data/Events: MBA Mortgage Applications

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Futures Edge Higher, Outperforming US Tsys, BoJ Speech Tomorrow

JGB futures have traded with a firmer bias post the lunch time break. We were last 137.42, +.06 versus settlement levels for the Sep contract. Earlier lows were at 137.28, which was just above Tuesday lows of 137.22. JGBs have defied the softer tone from US Tsy futures, although highs so far today remain comfortably within week to date ranges.

- Headlines crossed a short while ago from BBG that: "Korea Investment & Securities Co. plans to buy unhedged super-long Japanese government bonds for the first time to take advantage of rich yields and its expectation for the yen to maintain gains against the dollar." (see this link for more details). This may helping at the margins, particularly given expectations of wider fiscal borrowing requirements, along with less onshore appetite to hold government bonds.

- BoJ regular bond buying ops also took place today, another potential marginal positive.

- Cash JGB yields are little changed. The 10yr remains near 1.625%. The 2/30 JGB curve has ticked up to +235bps, but remains within recent highs. The 30yr JGB yield is pressing towards all time highs of 3.22%. Swap rates have edged down slightly, the 10yr last around 1.43%.

- Tomorrow on the data front we just have offshore weekly investment flows. Focus will be on a speech from BoJ board member Nakagawa.

AUSSIE BONDS: Weaker But Away From Lows Post July CPI Beat

Aussie bond futures hold weaker, but away from session lows. Weakness has been concentrated in the front end. The 3yr (YM) future was last 96.565, off 3bps, up slightly from session lows of 96.535. The 10yr future (XM) is off less than 1bp at this stage.

- The main data focus was the July CPI print, which came in well above market expectations (headline at 2.8%y/y versus 2.3% forecast and trimmed mean to 2.7%y/y from 2.1% in June).

- The monthly data are incomplete, for instance services aren’t updated in the first month of the quarter, and headline continues to be impacted in both directions by government electricity rebates. As a result, the RBA continues to focus on the quarterly data with Q3 not released until October 29.

- This may have tempered market reaction to a degree.

- In the cash ACGB space, yields are higher across the curve, with the front end leading. We sit away from yield highs though. The 3yr last near 3.42% (highs were close to 3.44%), up 2.5bps, while the 10yr is up close to 1bp, last near 4.32%.

- There has been a slight firmed in RBA dated OIS, around 2bps for contracts out to April next year. Still a full cut is still priced for the Nov 2025 meeting. Only 20% probability of a cut is given for the Sep meeting.

- Tomorrow, we get further inputs into Q2 GDP, with Private capex out. Earlier, Q2 real value of construction work done rose 3% q/q & 4.8% y/y, highest since Q4 2023 and , stronger than expected, after -0.3% q/q & 3.0% y/y.

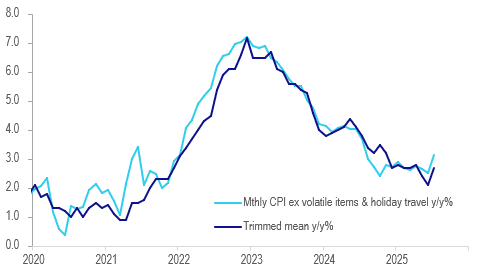

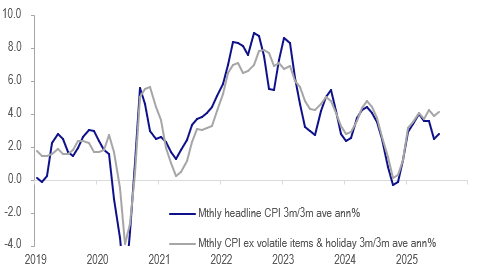

AUSTRALIA DATA: Underlying Inflation Picks Up But Volatile

July trimmed mean CPI inflation jumped to 2.7% y/y from 2.1% and headline to 2.8% from 1.9%. The monthly data are incomplete, for instance services aren’t updated in the first month of the quarter, and headline continues to be impacted in both directions by government electricity rebates. As a result, the RBA continues to focus on the quarterly data with Q3 not released until October 29. Comprehensive monthly CPI data is scheduled for November 26 but it will take time for seasonal trends to emerge.

Australia underlying inflation y/y%

Source: MNI - Market News/ABS

- In terms of underlying inflation, the trimmed mean was its highest in July since April. There was a strong monthly rise in CPI ex volatile items & holiday travel at +0.6% m/m to be 3.1% y/y seasonally adjusted, highest in almost a year, after 2.5% y/y in June. The 3-month annualised momentum remains around 4%, where it has been over most of 2025, and 6-month is just over 3.5%.

- The headline was boosted by a 13.1% y/y rise in electricity prices in July after falling 6.3% in June. They rose 13% m/m due to Commonwealth rebates not paid to households in NSW and ACT which will occur in August. Outside of government payments, electricity rose 4.8% m/m due to the yearly review.

- Other components were contained with rents up 3.9% y/y down from 4.2%, new dwellings rose 0.4% in line with June, and food & non-alcoholic beverages 3% y/y after 3.2%.

Australia inflation 3-month momentum %

Source: MNI - Market News/ABS

AUSTRALIA DATA: Tentative Signs Of Stabilisation In Vacancies

RBA Governor Bullock noted that the vacancies/unemployment ratio was well off its highs and thus signalling that the labour market has eased. The quarterly ratio has been moving sideways for a year and remains above the historical average. However, monthly internet vacancies/unemployed appeared to stabilise in the 3 months to July around the series average. The SEEK new job ads index has moved sideways through most of 2025.

Australia SEEK new job ads index 2013=100

- SEEK reported that July vacancies rose a seasonally adjusted 0.8% m/m but are still down 4.8% y/y. However, the 3-month annualised rate turned positive for the first time since July 2022, consistent with some stabilisation. SEEK notes that the trend posted two consecutive monthly increases for the first time since mid-2022.

- There was strong job ad growth in SA and WA and in the medical and hospitality sectors. SEEK observes that skill shortages persist in mining and renewable energy.

- June applicants-per-ad also appears to have peaked after trending higher since the May 2020 trough. In June the measure fell 4% m/m but is still up 9% y/y with 3-month momentum robust. Labour supply remains elevated.

- The stabilisation in vacancies is consistent with the S&P Global PMI which noted in the preliminary August composite report that there was increased hiring to fill a pickup in new orders. August employment is released on September 18.

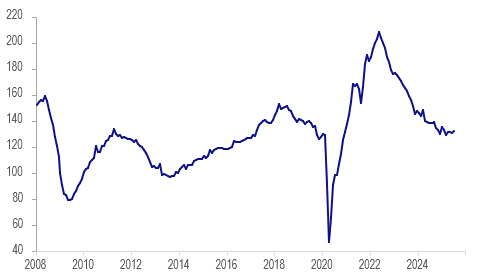

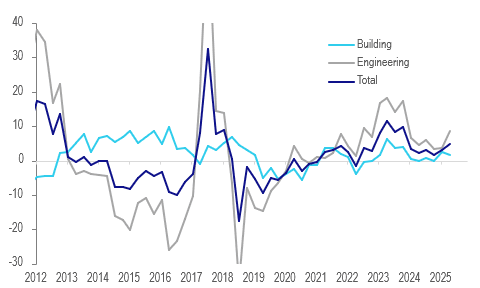

AUSTRALIA DATA: Narrow Rise In Construction Work

Q2 the real value of construction work done rose 3% q/q & 4.8% y/y, highest since Q4 2023 and , stronger than expected, after -0.3% q/q & 3.0% y/y. The rise was driven by engineering work with the building components lacklustre. Q2 GDP is released September 3 with private capex data Thursday, inventories September 1 and net exports and public demand contributions September 2.

Australia real value of construction work done y/y%

- The rise in construction was not broad based with only NT, ACT, SA and Tasmania recording quarterly increases and the NT rising 344.8% q/q.

- Engineering work rose 6.1% q/q to be up 8.5% y/y. This was predominantly done by the private sector leaving total private construction up 4.3% q/q & 6.6% y/y after 3.1% y/y.

- Building increased 0.2% q/q to be up 1.6% y/y with residential +0.1% & 5.3% y/y and non-residential +0.3% & -4.0%. New houses constructed fell 1.6% q/q to be up 2.3% y/y down from Q1’s 6.5% y/y.

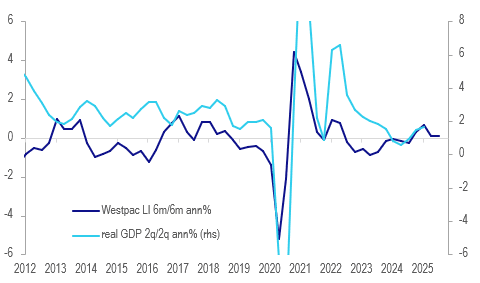

AUSTRALIA DATA: Lead Index Signals Continued Sluggish Growth

The Westpac leading index rose 0.12% m/m in July after being flat in June. This left the 6-month rate little changed at 0.06% signalling that the recovery is likely to remain gradual and lacklustre into year end. The RBA signalled that further rate cuts are consistent with inflation returning to the 2.5% mid-point of the target band and that is likely to remain the case while growth remains sluggish. Westpac expects rates to be on hold in September with November the next cut.

- Westpac is forecasting growth of 1.7% this year up from 1.3% in 2024. It is not expected to return to trend until the end of 2026 with 2.2% projected.

- Westpac notes that six of the eight lead index components contributed to the slowing in the indicator with commodity prices in AUD the main drag over 2025. Consumer confidence and unemployment expectations have also weighed. Equities, US IP and the yield gap have only helped slightly this year.

Australia Westpac lead index vs real GDP %

BONDS: NZGBS: Yields Up From Earlier Lows On ACGB Spillover

NZ government bond yields sit up from earlier lows. We opened with a softer tone, after US yields fell in Tuesday trade. However, 2yr to 10yr tenors are now only down marginally for the session. The 2yr is back to 2.98%, the 10yr near 4.36%. The 15 and 30yr bonds are off around 1bps. Spill over from the Australian monthly CPI beat, which aided firmer Aussie bond yields, has likely been in play. NZ 2yr swap rates have edged up slightly, last around 2.76%.

- Local news flow has been light. Via BBG: "New Zealand will introduce a Business Investor Visa that will provide a pathway to residence for business migrants who are ready to invest in, operate and grow established businesses, Immigration Minister Erica Stanford says in emailed statement." The scheme will be open to applications from this November.

- While the NZ FinMin commented on easing the pathway for new supermarket operators to set up in the country, in order to boost competition in the space.

- Tomorrow on the data front, we have July filled jobs, along with the August ANZ business confidence/activity prints.

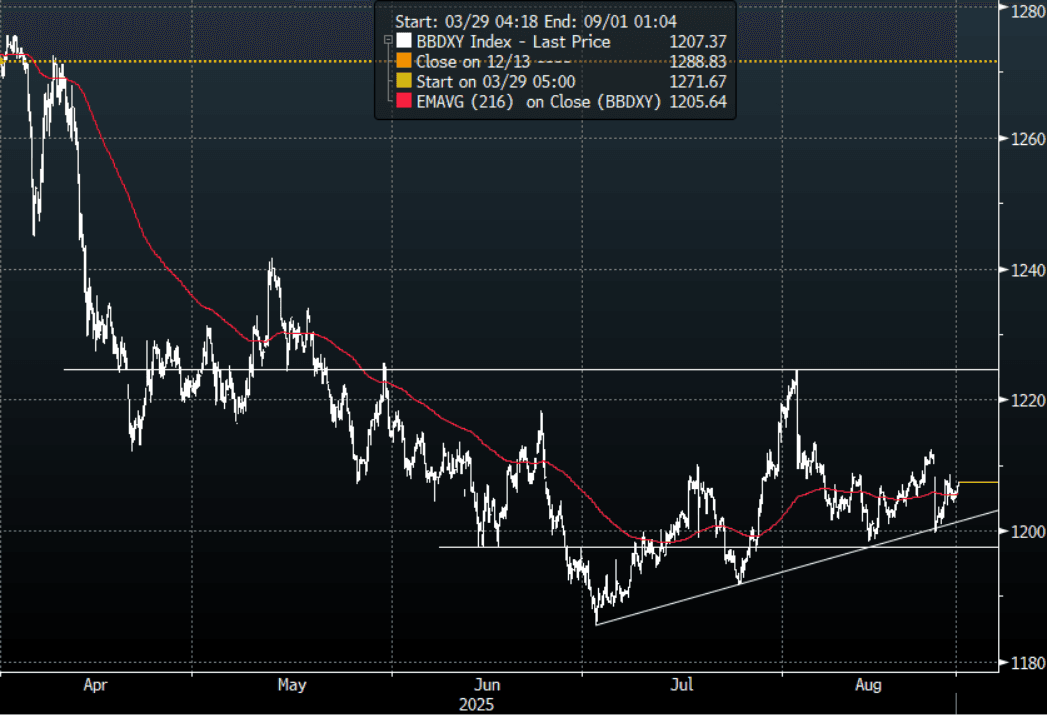

FOREX: Asia FX Wrap - The USD Finds Some Demand Into Month-End

The BBDXY has had a range of 1204.99 - 1207.46 in the Asia-Pac session, it is currently trading around 1207, +0.16%. The USD has been consolidating around 1205, managing to hold above its support in the face of the ongoing Fed debacle. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. We are heading into corporate month-end and this could explain the market's reticence to press the USD lower as we could see some USD demand potentially over today and tomorrow.

- EUR/USD - Asian range 1.1621 - 1.1649, Asia is currently trading 1.1620. The pair is consolidating just above its support. First support is back towards 1.1550, a move back below here could signal a deeper pullback as the market tries to find a base from which to build for another extension higher.

- GBP/USD - Asian range 1.3454 - 1.3483, Asia is currently dealing around 1.3450. The pair is consolidating just below 1.3500. Back in the middle of its recent 1.3350-1.3650 range, the USD’s fate will have a direct impact on which side is tested.

- USD/CNH - Asian range 7.1457-7.1578, the USD/CNY fix printed 7.1108, Asia is currently dealing around 7.1550. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.08%, Gold $3376, US 10-Year 4.27%, BBDXY 1207, Crude Oil $63.26

- Data/Events : Germany GfK Consumer Confidence, Spain Total Mortgage Lending

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

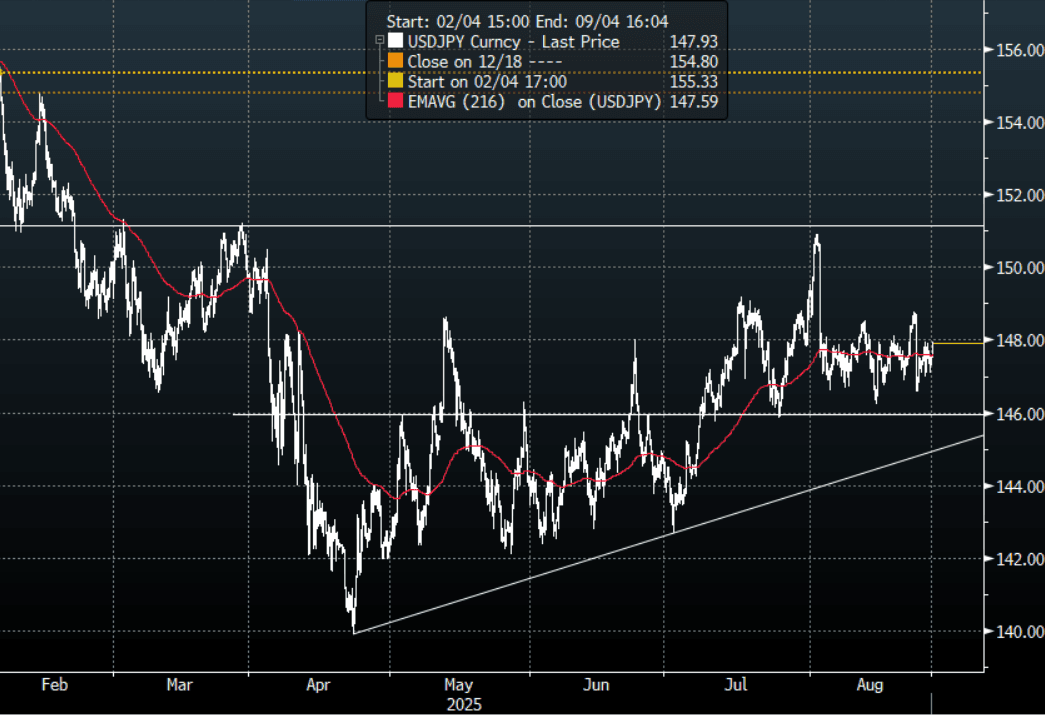

JPY: Asia Wrap - USD Demand Sees USD/JPY Move Back To 148.00

The Asia-Pac USD/JPY range has been 147.30-147.95, Asia is currently trading around 147.90, +0.35%. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. CFTC data for last week shows leveraged accounts again added to JPY shorts so the initial reaction to Powell would have been unwelcome and they would be breathing a little easier as the support continues to hold. We are approaching the corporate month-end so watch for USD demand today and tomorrow. This pair was bid all day today, which does hint at some USD demand flow being executed.

- Kyodo News via BBG - “Long-term interest rates rise to 1.625%, the highest level in 17 years: The yield on the newly issued 10-year government bond (379th issue, nominal interest rate 1.5%), which is an indicator of long-term interest rates, rose to 1.625% at one point, the highest level in about 17 years since October 2008.”

- (Bloomberg) - JGB traders see shorting long-term debt as the gift that keeps giving, with an assist from rising G-10 yields as well as Japan’s Ministry of Finance requesting a bigger budget for its debt financing needs. It’s a vicious cycle for JGBs -- the longer the Bank of Japan stalls in hiking interest rates, the more compensation investors demand for holding super-long bonds as stagflation fears rise.

- “HAYASHI: AKAZAWA VISIT TO THE US NOT DECIDED YET" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.25($765m), 147.95($1.04bm), 148.00($997m).Upcoming Close Strikes : 145.00($1.17b Aug 29), 146.50($1.14b Aug 29), 147.50($806m Aug 29) - BBG.

- CFTC data shows last week asset managers have begun to add to their JPY longs after a consistent period of reduction +71379( Last +60866), leveraged funds though again used the dip to add to their newly built short JPY position -50848(Last -41257).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

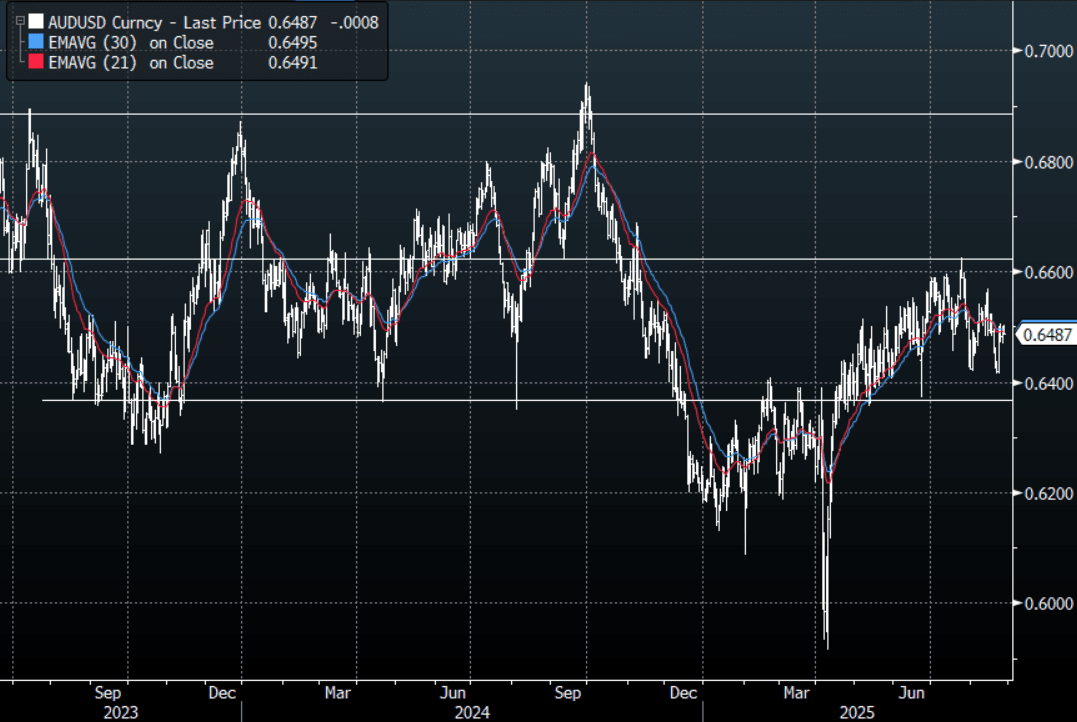

AUD: Asia Wrap - AUD/USD Tries And Fails Above 0.6500 On CPI Print

The AUD/USD has had a range of 0.6487 - 0.6504 in the Asia- Pac session, it is currently trading around 0.6490, -0.10%. The AUD initially tried to push higher after the CPI print but stalled above 0.6500 and drifted back lower for the rest of our session. The AUD finds itself firmly back in the middle of its recent multi-month range of 0.6350-0.6650 and will need a clearer direction from both the USD and risk to embark on a decent move in either direction. We are approaching the corporate month-end so there could be some demand for USD today or tomorrow which is worth looking out for.

- Underlying Inflation Picks Up But Volatile: July trimmed mean CPI inflation jumped to 2.7% y/y from 2.1% and headline to 2.8% from 1.9%. The monthly data are incomplete, for instance services aren’t updated in the first month of the quarter, and headline continues to be impacted in both directions by government electricity rebates. As a result, the RBA continues to focus on the quarterly data with Q3 not released until October 29. Comprehensive monthly CPI data is scheduled for November 26 but it will take time for seasonal trends to emerge.

- Narrow Rise In Construction Work: Q2 the real value of construction work done rose 3% q/q & 4.8% y/y, highest since Q4 2023 and , stronger than expected, after -0.3% q/q & 3.0% y/y. The rise was driven by engineering work with the building components lacklustre. Q2 GDP is released September 3 with private capex data Thursday, inventories September 1 and net exports and public demand contributions September 2

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6525(AUD695m). Upcoming Close Strikes : 0.6400(AUD571m Aug 28), 0.6500(AUD782m Aug 29), 0.6455(AUD555m Sept 1) - BBG

- AUD/JPY - Asia-Pac range 95.61 - 96.00, Asia is trading around 95.95. The pair continues to grind higher back towards the 96.00 area. This pair’s direction will be determined by the market's ability to follow on with this risk-on move or not. A sustained move back above 96.50 would turn the trend higher again but until then sellers should be around looking for this move to top out.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

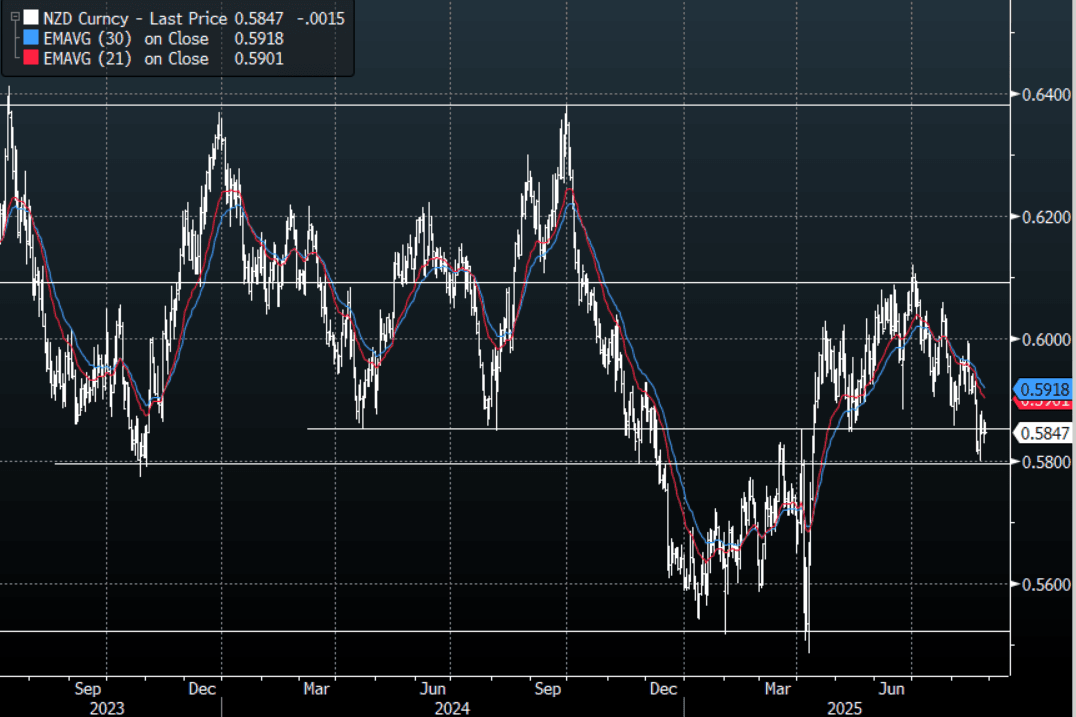

NZD: Asia Wrap - NZD/USD Trades Heavy

The NZD/USD had a range of 0.5843 - 0.5864 in the Asia-Pac session, going into the London open trading around 0.5845, -0.30%. US equities once again found buyers on the dip and the USD traded a little soft overnight. The NZD traded heavy all through Asia as the USD found a bid tone this morning. We are approaching the corporate month-end so there could be some demand for USD today or tomorrow. US Futures have traded slightly higher this morning, E-minis +0.10%, NQU5 +0.12%.

- Bloomberg - “RBNZ increased its foreign currency intervention capacity to NZ$26.3b at the end of July, according to data released by the central bank on its website. The capacity - foreign currency assets that are readily liquefiable less foreign currency liabilities that fall due in the next 12 months - rose from NZ$25.6b in June”

- “The strengthening yuan is opening the door for more upside for regional peers, particularly those most sensitive to the Chinese currency’s moves such as the Aussie and kiwi dollar, Korean won and Singapore dollar.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6200(NZD355m). Upcoming Close Strikes : none - BBG

- CFTC Data of last week shows Asset Managers slightly reduced their new short position in the NZD -3198(Last -3679), the Leveraged community also reduced their own shorts slightly -4004(Last -4190).

- AUD/NZD range for the session has been 1.1079 - 1.1109, currently trading 1.1095. The dovish RBNZ has seen the Cross surge higher breaking back above 1.100 convincingly. This move should now continue to see dips supported as it looks to build momentum to push higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Strong Day of Gains for Major Regional Bourses

The recent uptrend for China's stocks continued today with major bourses delivering gains as markets turn their attention to Nvidia's earnings and the US inflation report to come. Tech shares in the region remain strong with key AI companies in focus.

- The NIKKEI is up +0.29% today, attempting to recover from yesterday's falls of nearly 15.

- In China, whilst the Hang Seng hovered around where it opened, the onshore offshore divide continues with the CSI 300 up +0.72%, Shanghai up +0.33% and Shenzhen one of the best regional performers up +0.80%.

- The TAIEX in Taiwan rose +0.74% to mark three days of gains of just over 3%.

- The KOSPI ignored better than expected retail sales and ahead of the BOK decision is only marginally higher on the day.

- In South East Asia, the FTSE Malay KLCI is flat, whilst the Jakarta Composite is up +0.30%.

- In the Philippines, the PSEi is one of the best regional performers ahead of the BSP decision, up +1.3%.

- The NIFTY 50 in India is closed, having finished yesterday down heavily by -1%.

OIL: Crude Holding Onto Tuesday’s Losses As Watching Developments

Oil prices are little changed in today’s APAC session following a sharp sell off on Tuesday. WTI is around $63.25/bbl after falling to $63.15 and reaching $63.46 early in trading. Brent is 0.1% higher at $67.26/bbl off the intraday low of $67.13. The USD index is 0.2% higher.

- US 25% punitive tariffs on India came into effect today because it continues to purchase Russian oil. It has not been put off by the threat and likely believes that duties will be delayed or withdrawn. There are concerns that global supplies will be materially impacted if they are extended to China and enforced. Progress on negotiating a Ukraine peace appears to have stalled.

- Bloomberg quotes sources that Indian refiners plan to buy 1.4-1.6mbd for delivery from October down from H1’s 1.8mbd.

- Bloomberg reported that US crude inventories fell 1mn barrels last week, according to people familiar with the API data. Products were also lower with gasoline down 2.1mn and distillate 1.5mn. The official EIA data is out today.

- Later the Fed’s Barkin repeats comments previously given. The data calendar is light with only September German GfK consumer confidence of note. Markets are waiting for US PCE price data on Friday.

Gold Lower As Greenback Strengthens

Gold has given up some of Tuesday’s gains in today’s APAC session. It has been pressured by a stronger US dollar (BBDXY +0.2%) and higher yields and is down 0.6% to $3374.7/oz, close to the intraday low.

- Bullion reached a high of $3394.31 on Tuesday on concerns that the Fed was losing its independence after President Trump announced the removal of Governor Cook. She is fighting the decision though. If Trump can replace her, then he can have four of the seven FOMC members and possibly engineer more dovish monetary policy, which would be positive for gold prices.

- The rally early this week did not see bullion testing initial resistance at $3409.2, 8 August high. Initial support is $3311.6, 20 August low. Moving average studies remain in bull mode.

- Silver is 0.4% lower at $38.44 after falling to $38.439. It started Wednesday around $38.704. The outlook for the metal remains bullish with initial resistance at $39.655. A clear break of the 50-day EMA at $37.282 is needed to switch to a bearish trend.

- Equities are generally stronger with the S&P e-mini up 0.1% and CSI 300 +0.7%. Oil prices are little changed with WTI around $63.28/bbl. Copper is down 0.2%.

- Later the Fed’s Barkin repeats comments previously given. The data calendar is light with only September German GfK consumer confidence of note. Markets are waiting for US PCE price data on Friday.

MNI BOK Preview August 2025: On Hold with Eyes on Housing

Download Preview Here:

- The BOK are likely to remain on hold given the stable outlook for inflation, albeit below year end forecasts.

- The government policies announced to cool the housing market, are yet to come into effect.

- The uncertainty arising from the trade war is removed, whilst exports have remained resilient.

- The consumer's outlook is strong with consumer confidence and retail sales up.

MNI BSP Preview August 2025: BSP to Cut Further

Download Full Document Here:

- Inflation remains below the BSP target and moderated further in July, hitting lowest levels in more than 5-years.

- Whilst the tariff uncertainty has now been removed, the impact of the imposition of tariffs is yet to be felt across economy.

- The decline in oil whilst good for the economy, will put further downward pressure on inflation.

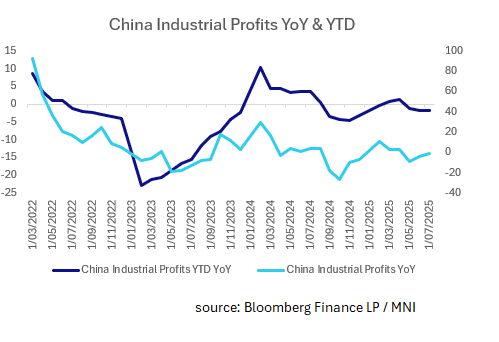

CHINA: Industrial Profit Declines Continue

- China's Industrial Profit in July declined, marking a third consecutive month.

- China Industrial Profits YoY contracted -1.5%, following -4.3% in June.

- This is the seventh monthly decline out of the prior 12.

- The Year to date result of -1.70% was in line with the prior month's result of -1.8%.

- The Year to date Industrial Company's Profit was CNY4.02tn.

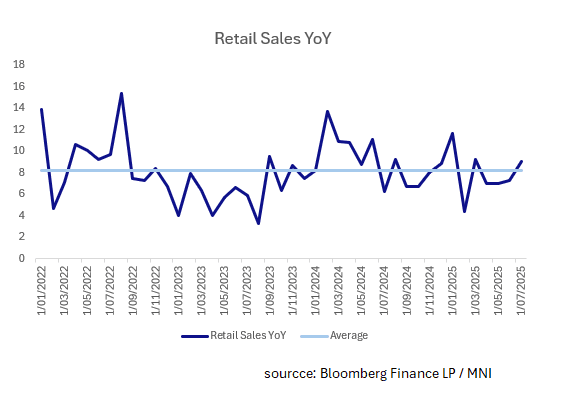

SOUTH KOREA: July Retail Sales Post Strong Gains Ahead of BOK Decision

- Korea's July Retail Sales YoY posted the strongest month in four as the recovery in consumer confidence becomes evident.

- July's result of +9.1% was marked uptick from June's +7.3%

- Department Store Sales YoY rose +5.1% for its strongest month since January.

- Discount Store Sales YoY contracted for a second month, this time by -2.4%.

- The growing strength of the consumer gives the BOK something to think about as they approach the monetary policy decision tomorrow. Market consensus as this stage if for no change, following on from the July meeting where they remained on hold also.

ASIA FX: Most Firmer USD/Asia Bias, USD/HKD Bucks The Trend

In North East Asia FX, the bias has been for a slightly stronger USD. USD/CNH got to lows of 7.1457, aided by the stronger CNY fixing and the lower USD/CNY spot open onshore, but we have steadily recovered ground since then. The pair was last back above 7.1560. Broader USD sentiment has been supported against the majors, which may reflect month end dynamics. The BBDXY is up close to 0.20%, the DXY +0.25% so far today. China equities continue to rally, the CSI 300 up a further 0.72%.

- Spot USD/KRW has traded with a positive bias, but at 1396, remains sub intra-session highs from Tuesday (1398.45). The BoK policy announcement is tomorrow, but no change is expected.

- USD/TWD is little changed, last near 30.55. Spot USD/HKD has bucked these trends and is tracking under 7.7800 in latest dealings. This appears to reflect further carry trade unwinds. HKD T/N points are approaching flat, while Hibor rates are up noticeably today and over recent weeks.

- In South East Asia, the bias has also been for a stronger USD. USD/IDR is up around 0.30%, last near 16345, while USD/MYR and USD/PHP are both up around 0.20%. This puts USD/MYR back near 4.2300, while USD/PHP is just above 57.20. USD/THB is up more modestly, close to 32.52 in latest dealings.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 27/08/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 27/08/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 27/08/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 27/08/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 27/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 27/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 27/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 27/08/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 27/08/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/08/2025 | 0130/1130 | * | Private New Capex and Expected Expenditure | |

| 28/08/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/08/2025 | 0700/0900 | *** | GDP | |

| 28/08/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 28/08/2025 | 0800/1000 | ** | M3 | |

| 28/08/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 28/08/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 28/08/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 28/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 28/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 28/08/2025 | 1230/0830 | * | Current account | |

| 28/08/2025 | 1230/0830 | * | Payroll employment | |

| 28/08/2025 | 1230/0830 | *** | GDP / PCE Quarterly |