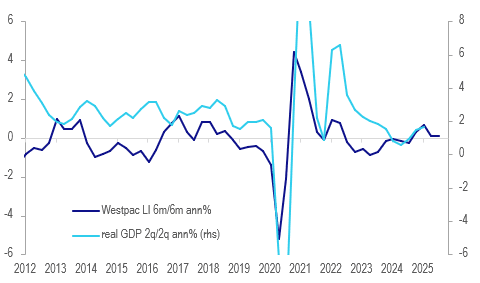

AUSTRALIA DATA: Lead Index Signals Continued Sluggish Growth

The Westpac leading index rose 0.12% m/m in July after being flat in June. This left the 6-month rate little changed at 0.06% signalling that the recovery is likely to remain gradual and lacklustre into year end. The RBA signalled that further rate cuts are consistent with inflation returning to the 2.5% mid-point of the target band and that is likely to remain the case while growth remains sluggish. Westpac expects rates to be on hold in September with November the next cut.

- Westpac is forecasting growth of 1.7% this year up from 1.3% in 2024. It is not expected to return to trend until the end of 2026 with 2.2% projected.

- Westpac notes that six of the eight lead index components contributed to the slowing in the indicator with commodity prices in AUD the main drag over 2025. Consumer confidence and unemployment expectations have also weighed. Equities, US IP and the yield gap have only helped slightly this year.

Australia Westpac lead index vs real GDP %

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LNG: US Gas Prices Start Monday Higher Following US-EU Deal

Natural gas finished last week lower as supplies continue to look ample and demand steady. Weather forecasts for the start of August signal that there is unlikely to be a pick up in cooling demand across the northern hemisphere, while preliminary July manufacturing PMIs imply that industrial demand is not rising either.

- US prices have started the week 0.6% higher at $3.13 following news of a EU-US trade deal over the weekend that involves the purchase of $750bn of US energy over the remainder of President Trump’s term. LNG is likely to be a significant share of this as the EU attempts to end the consumption of Russian fossil fuel.

- US gas was flat on Friday at $3.10 to be down 13.2% on the week and 9.4% in July. The increase of 5 gas rigs in the Baker Hughes count, after +9 the previous week, was offset by the EIA’s report of a below average increase in inventories the previous week. On Friday, US lower-48 production rose 3% y/y, while demand was up only 1% y/y.

- Bloomberg reports that the front-month Henry Hub contract is approaching oversold signals according to the relative strength index.

- European prices rose 0.3% to EUR 32.45 on Friday off the intraday low of EUR 31.91 reached early in the session. They were down 3.4% last week to be -1.4% this month.

- While storage refilling continues at a solid pace, Europe remains vulnerable to disruptions. Norway has planned maintenance in August, which will be monitored closely for any extensions.

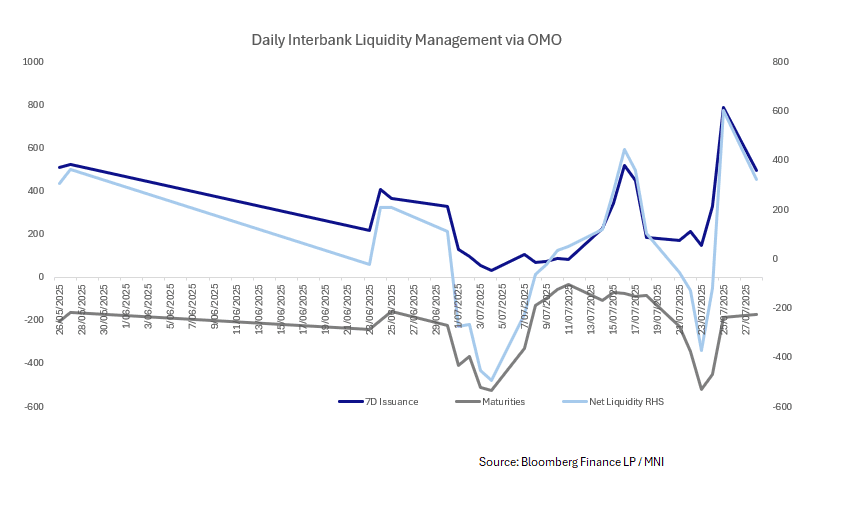

CHINA: Central Bank Injects CNY325.1bn via OMO

- The PBOC issued CNY495.8 bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY170.5bn

- Net liquidity injection CNY325.1bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.52%, from prior close of 1.65%.

- The China overnight interbank repo rate is at 1.45%, from the prior close of 1.55%.

- The China 7-day interbank repo rate is at 1.63%, from the prior close of 1.64%.

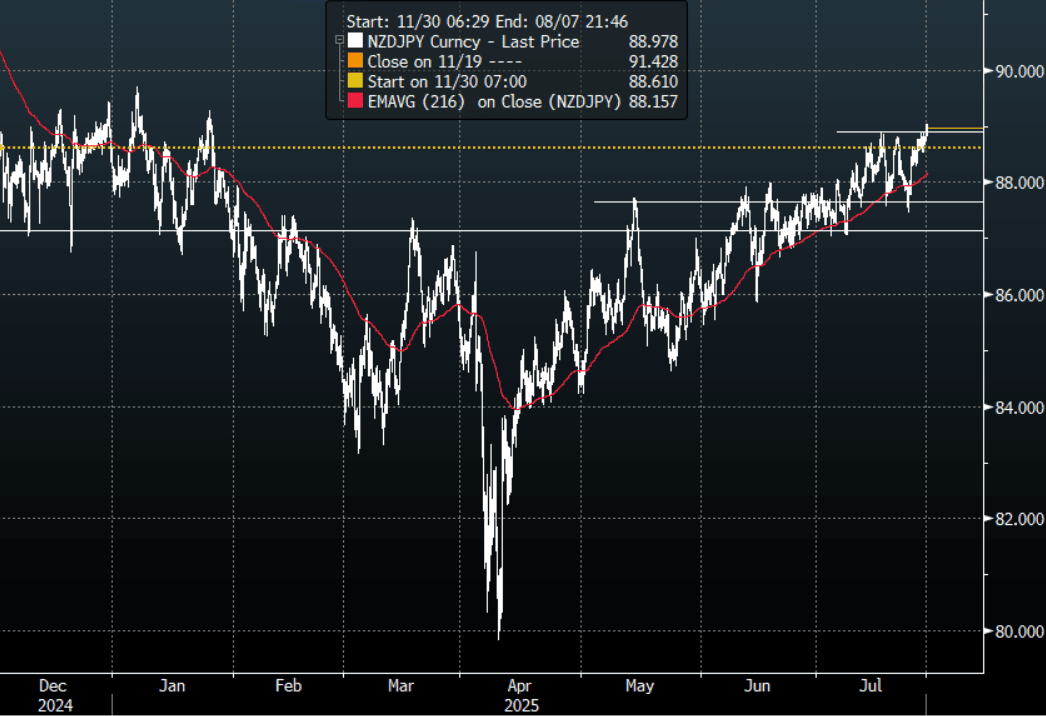

FOREX: JPY Crosses - US-EU Deal Adds To Positive Backdrop, Pressuring The JPY

This morning has seen US futures gap higher in response to the US-EU trade deal, ESU5 +0.36%, NQU5 +0.50%. If risk continues to trade well then this should provide the JPY crosses with a tailwind to move higher, the event-risk posed by this week could provide some short-term challenges.

- EUR/JPY - Friday night range 172.56 - 173.61, Asia is trading around 173.75. This pair has had a decent move higher and has led the charge against the JPY longs. Short-term it is starting to look a little stretched but the direction is clear and should expect demand on dips. First support 170.00 area then the more important 168.00 area.

- GBP/JPY - Friday night 198.14 - 199.08, Asia trades around 198.65. The pair continues to find strong demand around its 198.00 support. It is looking to regain its momentum for a push higher from this base.

- NZD/JPY - Friday night range 88.53 - 88.88, Asia is currently dealing 89.00. The pair is challenging its recent multiple highs towards 89.00, can it look past the risks of this week and extend higher ? Above here and the focus will turn to the 90.00/91.00 area.

- CNH/JPY - Friday night range 20.5099 - 20.6348, Asia is currently trading around 20.6000. This pair found strong demand towards its 20.3000/20.4000 support area, can it regain the upward momentum ? A sustained move back below 20.3000 now would start to turn the pendulum back towards the Bears.

Fig 1 : NZD/JPY 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P