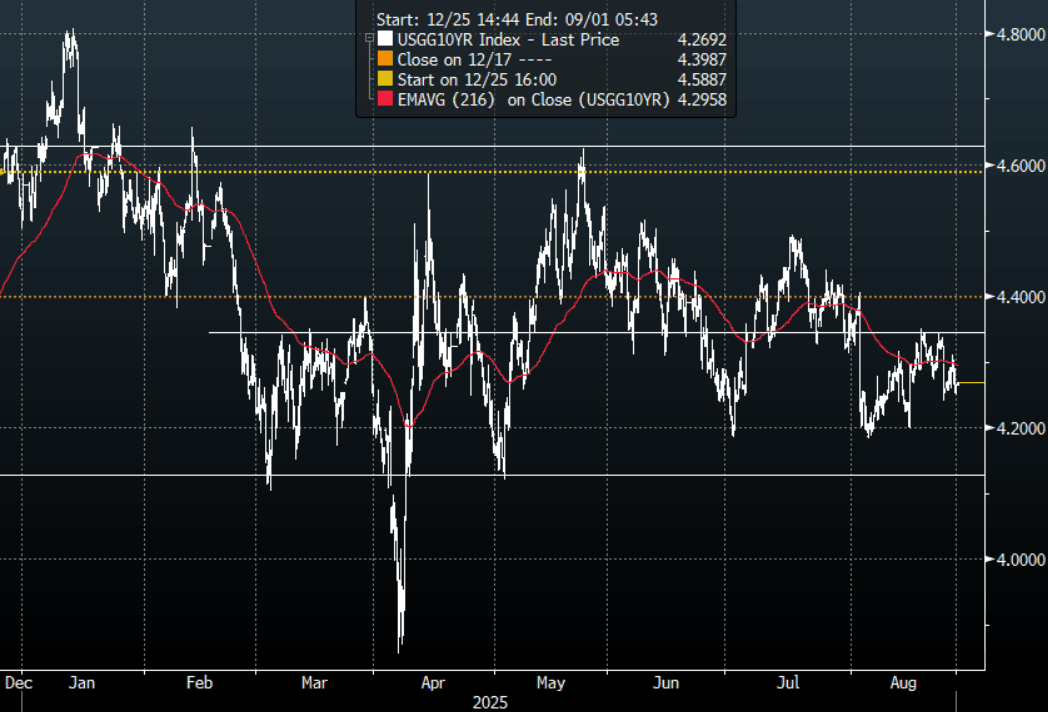

US TSYS: 2s10s Moves Higher

The TYU5 range has been 112-03+ to 112-05+ during the Asia-Pacific session. It last changed hands at 112-04, down 0-02+ from the previous close.

- The US 2-year yield has edged lower trading around 3.6557%, down 0.02 from its close.

- The US 10-year yield has moved higher trading around 4.267%, up 0.01 from its close.

- This has seen the 2s10s steepen in Asia, +2.30 at 60.347.

- 10-Year Yields found buyers above 4.30% again overnight. While the 4.35% area continues to hold, bounces should be met with demand, with the 30-Year taking the brunt of the selling related to challenging the Fed independence. First target is the recent lows around 4.18% then the bottom of the range towards 4.10% comes back into focus.

- Andrew Ackerman on X: “The Fed has deferred any decision on Cook's status because they are expecting a quick decision from a court on Cook's coming request for a judicial order/TRO, according to a Fed official. Would note the Fed has no board meetings scheduled for this week, while Cook is in limbo.”

- ISABELNET on X: “10Y Yield: When the Fed prioritizes the labor market over inflation, it can reduce the immediate risk of recession by sustaining employment. However, this is likely to increase inflation expectations and push yields higher”

- RenMac on X: “Consumers see increasing slack in the jobs market. The Labor Differential continues to soften, falling to a fresh low of 9.7 in August. In particular, we saw a notable jump in those saying “jobs hard to get.” See Fig.1 Below

- Data/Events: MBA Mortgage Applications

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: Asia Wrap - AUD/USD Tries Higher On Trade Deal, No Follow Through

The AUD/USD has had a range of 0.6566 - 0.6586 in the Asia- Pac session, it is currently trading around 0.6567, +0.02%. The pair traded with a heavy tone all through Friday but has attempted to bounce this morning as the market digests news of a US-EU trade deal. The pair failed to gain any momentum above 0.6600 last week and now awaits a very busy calendar this week which could have meaningful implications for risk. Locally the Australian Q2 CPI on Wednesday will be closely watched and could provide a catalyst for some movement. Worth keeping in mind we are approaching the corporate month-end so there could be a demand for some USD’s today but more likely that flow will be executed tomorrow.

- The focus of this week will be Wednesday's Q2 CPI data, which is expected to show the underlying trimmed mean measure making further progress towards the band mid-point of 2.5%. Bloomberg consensus is forecasting a 0.7% q/q rise, bringing the annual rate to 2.7% after 0.7% & 2.9% in Q1. This is slightly higher than the RBA's May Q2 forecast of 2.6%. Services developments will also be monitored. The RBA is expected to cut rates 25bp on August 12.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD608m), 0.6550(AUD555m). Upcoming Close Strikes : 0.6600(AUD968m July29), 0.6600(AUD1.38b July 31), 0.6465(AUD1.01b July31) - BBG

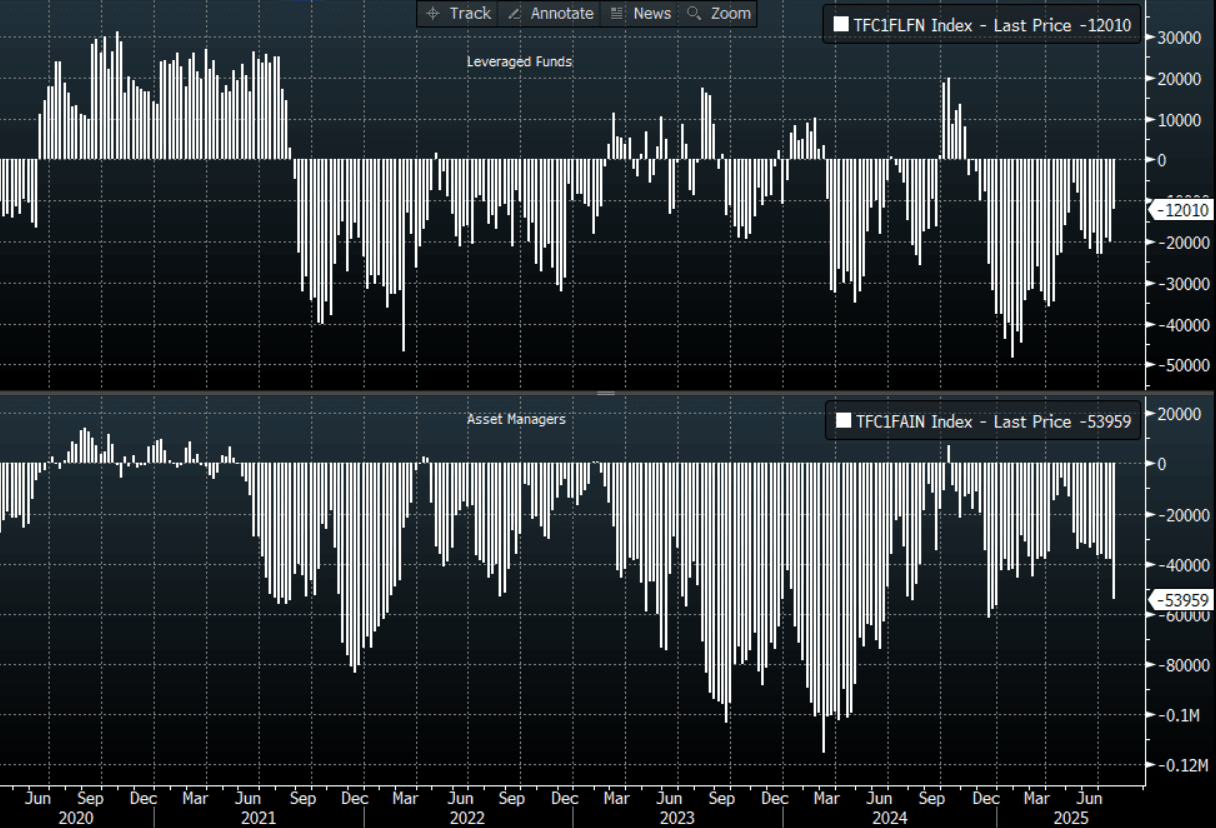

- CFTC Data shows Asset managers added a decent clip to their shorts -53959(Last -38267), the Leveraged community reduced their own shorts to -12010(Last -20048).

- AUD/JPY - Today's Asia-Pac range 97.03 - 97.29, it is trading currently around 96.95, +0.01%. The pair is pressing above its highs of last week. The support between 95.00 - 96.00 held very well last week and the pair is looking to regain its momentum for a move higher. The event-risk coming up this week could provide some short-term headwinds.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Mixed Trends Despite Higher EU Futures On US-EU Trade Deal

Asia Pac stocks are mixed in the first part of Monday trade. This comes despite a better tone to both US and EU equity futures. US futures were last up 0.40-0.55%, with the tech side leading. EU futures were around +1% higher, as market took some comfort from the earlier headlines around a 15% tariff deal between the US and EU (for most EU exports to the US). Positive spillover has been limited to this region so far today.

- Japan markets are weaker, the Topix off around 0.50%, while the NKY 225 is down around 0.90%. Sell-side analysts have noted profit taking ahead of key earnings in the Chip sector as a potential headwind (via BBG), while political uncertainty also continues. PM Ishiba has vowed to stay on as PM, despite recently losing upper house elections (and after onshore media outlets indicated he would resign in August).

- In Hong Kong, markets are modestly higher, the HSI up around 0.4%, while the CSI 300 is down a touch in China. Over the weekend we saw profit results remain negative in y/y terms for June, albeit up from the May decline.

- South Korea's Kospi has been volatile, initially rallying at the open, aiding by a large Samsung chip order (for Tesla) but once again the index has struggled above 3200. Focus remains on US-South Korea trade negotiations ahead of the Aug 1 deadline at the end of the week, with officials set to meet later in the week (reportedly July 31).

- Thailand markets are out today, as the US attempts to lead efforts to de-escalate tensions on the Thailand/Cambodian border.

- Indonesia is up +1.25%, one of the better performers in SEA so far today. The initial tone in Indian markets is for modest downside, continuing the recent run of underperformance for these markets.

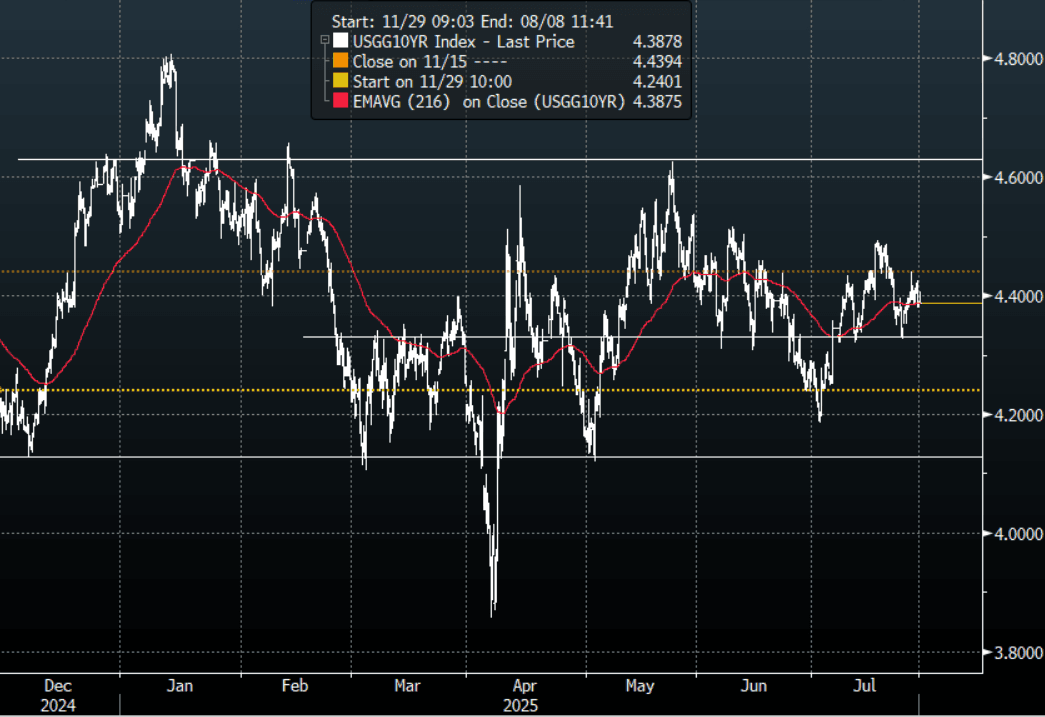

US TSYS: Yields Largely Unchanged In The Asia-Pac Session

The TYU5 range has been 110-26 to 110-30+ during the Asia-Pacific session. It last changed hands at 110-30, down 0-01 from the previous close.

- The US 2-year yield is trading around 3.923%.

- The US 10-year yield is trading around 4.388%.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, decent supply was seen around 4.30/35% first up. A decent bounce off its support but the move has failed to follow through above 4.40% for now. The Data this week should provide more clarity going forward.

- (Bloomberg) - “Strong demand for investment-grade corporate bond supply is likely to overwhelm a lack of supply this week. That can act to narrow US high-grade bond spreads.”

- (Bloomberg) - “Investors pulled $3.9 billion from Treasuries in June and added $10 billion to US and European IG company debt — a shift away from the idea that US government debt is the safest bet.”

- Data/Events: Dallas Fed Manf. Activity

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P