JGBS: Futures Edge Higher, Outperforming US Tsys, BoJ Speech Tomorrow

JGB futures have traded with a firmer bias post the lunch time break. We were last 137.42, +.06 versus settlement levels for the Sep contract. Earlier lows were at 137.28, which was just above Tuesday lows of 137.22. JGBs have defied the softer tone from US Tsy futures, although highs so far today remain comfortably within week to date ranges.

- Headlines crossed a short while ago from BBG that: "Korea Investment & Securities Co. plans to buy unhedged super-long Japanese government bonds for the first time to take advantage of rich yields and its expectation for the yen to maintain gains against the dollar." (see this link for more details). This may helping at the margins, particularly given expectations of wider fiscal borrowing requirements, along with less onshore appetite to hold government bonds.

- BoJ regular bond buying ops also took place today, another potential marginal positive.

- Cash JGB yields are little changed. The 10yr remains near 1.625%. The 2/30 JGB curve has ticked up to +235bps, but remains within recent highs. The 30yr JGB yield is pressing towards all time highs of 3.22%. Swap rates have edged down slightly, the 10yr last around 1.43%.

- Tomorrow on the data front we just have offshore weekly investment flows. Focus will be on a speech from BoJ board member Nakagawa.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Closed With A Modest Bull-Flattener

NZGBs closed at session bests, with the 2/10 curve showing a bull-flattener. Yields closed 1-3bps lower after being 1-2bps higher earlier in the session.

- The NZ-US and NZ-AU 10-year yield differentials finished 2-3bps tighter, reversing Friday's widening.

- Swap rates closed little changed.

- RBNZ dated OIS pricing closed little changed across meetings. 21bps of easing is priced for August, with a cumulative 35bps by November 2025.

- This week, the local calendar will see ANZ business confidence for July released on Wednesday. It continues to point to a gradual recovery in the economy. Cost and price components remain elevated, and inflation expectations are at 2.7% off their low.

- ANZ July consumer confidence is out on Friday. It rose sharply in June to 98.8, the highest this year but still off December's 100.2. Rate cuts, which take time to feed through to mortgage payments, have helped with households' financial situation and improved the time to buy component.

- June building permits will also print on Friday. They rose 10.4% m/m in May and indicators suggest that the construction sector is recovering.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 4.50% May-30 bond and NZ$175mn of the 4.25% May-34 bond.

FOREX: Asia FX Wrap - BBDXY Opens Lower But Claws Back Losses.

The BBDXY has had a range of 1196.82 - 1198.86 in the Asia-Pac session, it is currently trading around 1198, -0.04%. The USD’s slide lower finally stalled at the back end of last week and some profit-taking was seen. The market is much more comfortable selling USD’s and while below 1220 rallies should continue to find supply. There is lots of event risk coming up this week and we are heading into month-end so caution is warranted, this could potentially see some more paring back of USD shorts. Worth noting that corporate month-end tomorrow will most likely see some USD demand as well.

- EUR/USD - Asian range 1.1747 - 1.1770, Asia is currently trading 1.1750. The pair’s upward momentum seems to be stalling towards 1.1800. The price looks a little stretched in the short term, but while the USD is trading poorly the EUR will continue to be the main beneficiary. No real follow through on the trade deal in our session.

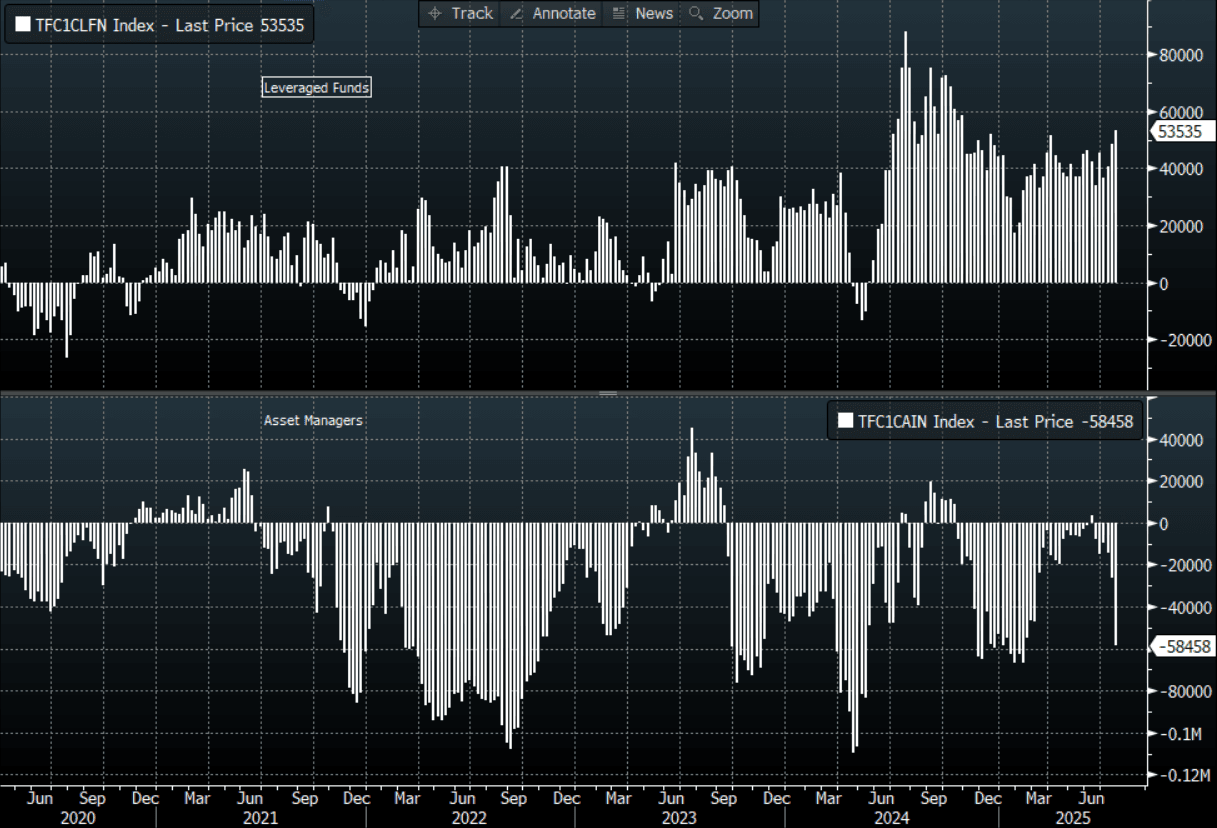

- GBP/USD - Asian range 1.3428 - 1.3453, Asia is currently dealing around 1.3440. The support around 1.3350/1.3400 has proved to be solid first up. The pair could not build on its move higher and has drifted back to the middle of its recent range. While the support holds the market will be encouraged to continue to play from the long side. A sustained break below 1.3350 could signal a deeper correction. CFTC Data shows Asset managers sold quite aggressively last week building their shorts back up -58458(Last -26467)

- USD/CNH - Asian range 7.1511 - 7.1722, the USD/CNY fix printed 7.1467, Asia is currently dealing around 7.1680. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.42%, Gold $3341, US 10-Year 4.388%, BBDXY 1198, Crude oil $65.43

- Data/Events :

Fig 1: GBP CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Gold Slightly Higher But Now Waiting For Week’s Key Events

Despite the announcement of an EU-US trade deal, gold is little changed in today’s APAC session. It seems to have priced in trade optimism on Friday when it fell almost a percent and is currently 0.1% higher at $3340.7/oz. With US-China talks and Wednesday’s Fed decision now in focus as well as significant US data over the week, bullion and other markets are range trading. The USD index and US yields are little changed.

- Equities are generally stronger with Euro stoxx futures +1.0% & S&P +0.4%. In Asia, the Hang Seng is up 0.4% but the Nikkei is down 1.0%. Oil prices are moderately higher with WTI +0.4% to $65.45/bbl. Copper is down 0.1%. Silver is up 0.2% to $38.23 after reaching $38.31 earlier.

- Markets are watching this week’s August 1 tariff deadline closely as negotiations with the US continue. In addition, there are the Fed’s decision on July 30, Q2 GDP & June PCE July 30 & 31, and US July payrolls August 1. A dovish Fed or weak US data would be supportive of gold prices.

- There are few events today with only the July Dallas Fed manufacturing and the ECB survey of monetary analysts released.