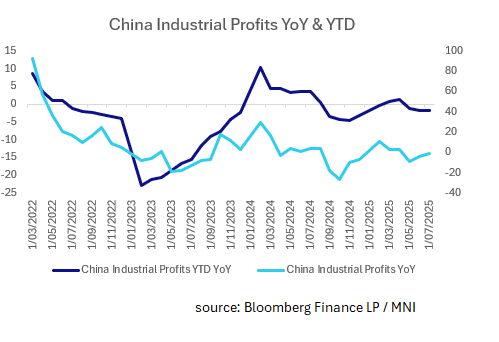

CHINA: Industrial Profit Declines Continue

- China's Industrial Profit in July declined, marking a third consecutive month.

- China Industrial Profits YoY contracted -1.5%, following -4.3% in June.

- This is the seventh monthly decline out of the prior 12.

- The Year to date result of -1.70% was in line with the prior month's result of -1.8%.

- The Year to date Industrial Company's Profit was CNY4.02tn.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSTRALIA: All Eyes On Wednesday’s Q2 CPI Data

The focus of this week will be Wednesday’s Q2 CPI data which is expected to show the underlying trimmed mean measure making further progress towards the band mid-point of 2.5%. Bloomberg consensus is forecasting a 0.7% q/q rise bringing the annual rate to 2.7% after 0.7% & 2.9% in Q1. This is slightly higher than the RBA’s May Q2 forecast of 2.6%. Services developments will also be monitored. The RBA is expected to cut rates 25bp on August 12.

- Q2 headline CPI will continue to be impacted by state and federal government electricity rebates. It is expected to rise 0.8% q/q and 2.2% y/y down from 2.4% y/y. The monthly June headline is forecast to be unchanged at 2.1% y/y.

- On Thursday, RBA Deputy Governor Hauser appears at the Barrenjoey Economic Forum at 0920 AEST. This is also likely to be watched closely following the RBA’s surprise July decision to hold rates.

- Thursday also sees Q2 retail sales volumes which are projected to rise only 0.1% q/q after a flat Q1 reading consistent with ongoing disappointing private consumption.

- June monthly retail sales values are also on Thursday but this will be the last release with household spending, which includes services, to replace it thereafter. Consensus expects a 0.4% m/m rise after 0.2% in May.

- Building approvals for June are also on Thursday and are forecast to rise 1.8% m/m after 3.2%. The series is notoriously volatile due to the multi-dwelling component.

- Q2 trade prices print Thursday with export prices expected to fall 3% q/q and import 0.4% q/q after rising 2.1% and 3.3% in Q1 respectively. A print in line with this would suggest a deterioration in the terms of trade.

- Other data include RBA June private credit released Thursday, Q2 PPI Friday, Cotality July home values Friday and final July S&P Global manufacturing PMI Friday.

LNG: US Gas Prices Start Monday Higher Following US-EU Deal

Natural gas finished last week lower as supplies continue to look ample and demand steady. Weather forecasts for the start of August signal that there is unlikely to be a pick up in cooling demand across the northern hemisphere, while preliminary July manufacturing PMIs imply that industrial demand is not rising either.

- US prices have started the week 0.6% higher at $3.13 following news of a EU-US trade deal over the weekend that involves the purchase of $750bn of US energy over the remainder of President Trump’s term. LNG is likely to be a significant share of this as the EU attempts to end the consumption of Russian fossil fuel.

- US gas was flat on Friday at $3.10 to be down 13.2% on the week and 9.4% in July. The increase of 5 gas rigs in the Baker Hughes count, after +9 the previous week, was offset by the EIA’s report of a below average increase in inventories the previous week. On Friday, US lower-48 production rose 3% y/y, while demand was up only 1% y/y.

- Bloomberg reports that the front-month Henry Hub contract is approaching oversold signals according to the relative strength index.

- European prices rose 0.3% to EUR 32.45 on Friday off the intraday low of EUR 31.91 reached early in the session. They were down 3.4% last week to be -1.4% this month.

- While storage refilling continues at a solid pace, Europe remains vulnerable to disruptions. Norway has planned maintenance in August, which will be monitored closely for any extensions.

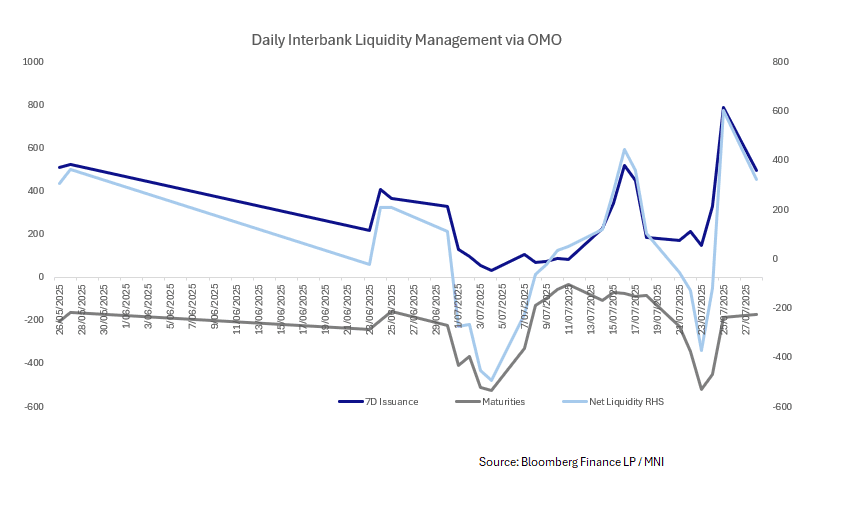

CHINA: Central Bank Injects CNY325.1bn via OMO

- The PBOC issued CNY495.8 bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY170.5bn

- Net liquidity injection CNY325.1bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.52%, from prior close of 1.65%.

- The China overnight interbank repo rate is at 1.45%, from the prior close of 1.55%.

- The China 7-day interbank repo rate is at 1.63%, from the prior close of 1.64%.