MNI EUROPEAN MARKETS ANALYSIS: Risk Rises On Trade Hopes

- Risk appetite was buoyed by headlines that China is assessing a US request for trade talks. US equity futures recouped earlier losses, while regional equity markets were mostly higher. US yields edged higher.

- Higher beta FX outperformed in the G10 FX space, while USD/Asia pairs were lower across the board. USD/TWD slumped to fresh 12 month lows.

- Asian PMIs were mostly weaker, but market sentiment wasn't impacted.

- Looking forward, the upcoming US NFP print is the main focus point.

MARKETS

US TSYS: Asia Wrap - Yields A Little Higher

TYM5 has traded a little lower within a range of 111-23+ to 112-01 during the Asia-Pacific session. It last changed hands at 111-26, down 0-01 from the previous close.

- The US 10-year yield is a little higher, dealing around 4.23%, up from its close around 4.21%.

- The US 2-year yield is a little higher, dealing around 3.71%, up from its close around 3.698%

- “Japanese Prime Minister Shigeru Ishiba says he was told the second round of tariff talks between his chief negotiator Ryosei Akazawa and US officials including Treasury Secretary Scott Bessent was “positive and constructive.”(per BBG)

- BBG noted: "China's Commerce Ministry said in a Friday statement that it had noted senior US officials repeatedly expressing their willingness to talk to Beijing about tariffs.

- NFP tonight will dictate price action further, with a wide distribution in the survey. There are calls for as low as 50k and some as high as 170k. The consensus seems to be around 138k.

- The 10-year Yield has bounced nicely off its first support around 4.10%. Resistance is seen towards 4.30% and we should see buyers remerge there initially. Range seems to be 4.10% - 4.45%, with the pivot the 4.25/30 area for now.

- Data/Events : US NFP

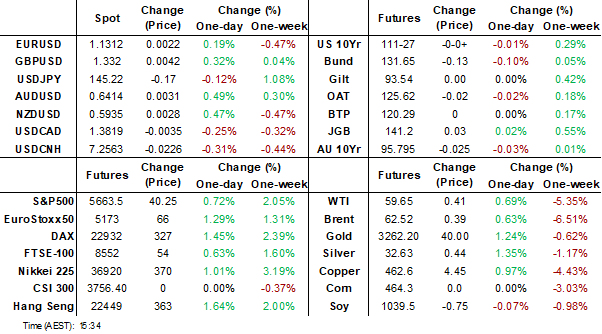

STIR: $-Bloc Markets Little Changed Over Past Week

Rate expectations across the $-bloc have remained broadly unchanged through December 2025 over the past week.

- This stability comes despite a series of key economic releases across most $-bloc economies. Later today will see the April US Employment Report, with the market expecting 138k jobs created after 228k last month. The unemployment rate is expected to be unchanged at 4.2%.

- In Australia, Q1 headline and underlying inflation printed 0.1pp higher than expected but the trimmed mean at 2.9% y/y is below the top of the RBA's 2-3% target band for the first time since Q4 2021. The data was close to the RBA's expectations and at this stage consistent with inflation sustainably remaining within the band. Thus, another 25bp rate cut to 3.85% is likely on May 20.

- The muted reaction underscores how market focus remains firmly on headlines surrounding U.S.–China trade tensions, with macroeconomic data taking a back seat.

- Looking ahead, the next major policy event in the $-bloc is the Fed's May 7 meeting, with markets currently pricing in just an 8% chance of a rate cut.

- Looking ahead to December 2025, the projected official rates and cumulative easing across the $-bloc are as follows: US (FOMC): 3.46%, -88bps; Canada (BOC): 2.23%, -52bps; Australia (RBA): 2.98%, -112bps; and New Zealand (RBNZ): 2.74%, -76bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

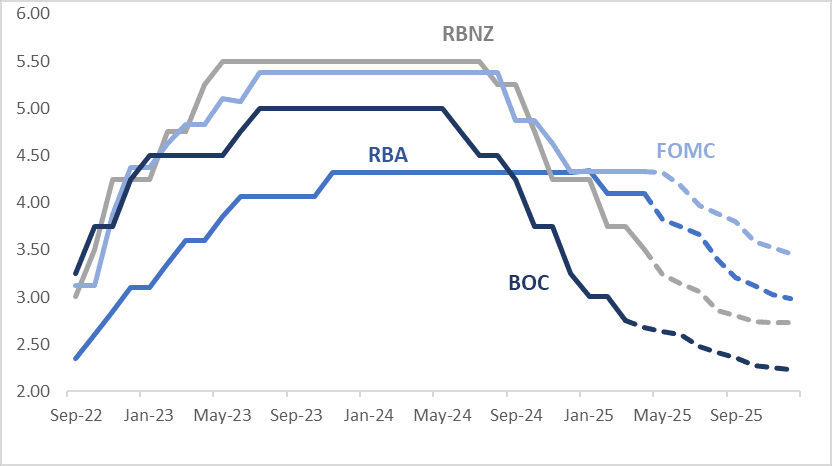

STIR: BoJ-Dated OIS Pricing Softer After BoJ Forecast Downgrades

BoJ-dated OIS pricing has softened by 1-5bps compared to pre-MPM levels, despite the market having had priced in a cautious, wait-and-see stance from the BoJ at yesterday's meeting.

- As widely expected, the BoJ left its policy rate unchanged at 0.50%, which was a unanimous decision of 9-0 by the board.

- The economic outlook was downgraded though in terms of both lower GDP and inflation forecasts. It also noted prices and growth risks for the 2025 and 2026 fiscal years rest to the downside.

- The central bank retained its bias that if the outlook is realised it will raise rates further, but the central bank places a caveat on those given extreme uncertainties around the trade outlook.

- Current OIS pricing assigns just a 3% probability of a 25bp hike at the June meeting, a cumulative 24% probability by September, and a 38% probability by December — a sharp shift from mid-February, when a hike by September was fully priced in.

- December pricing is now almost a full 25bp hike lower than the pre-March MPM level.

Figure 1: BoJ-Dated OIS – Today Vs. Pre-March MPM

Source: MNI – Market News / Bloomberg

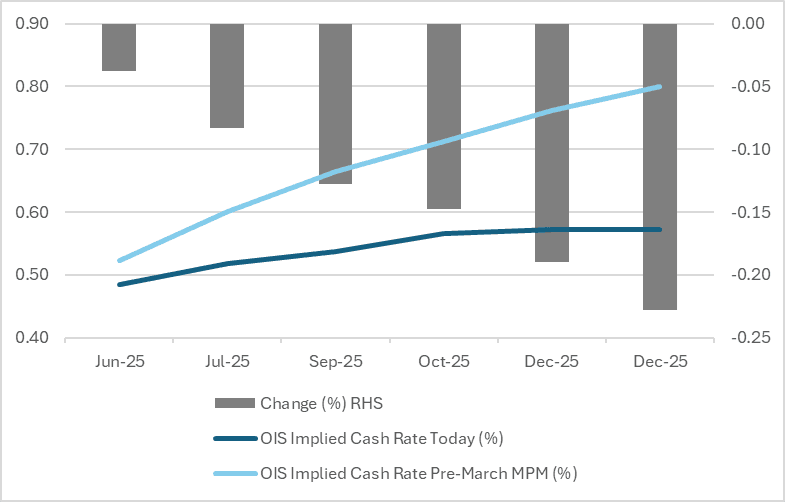

JAPAN DATA: Jobless Rate Edges Higher, But Still Close To Cycle Lows

Japan's jobless rate for March edged up to 2.5%, against a 2.4% forecast, which was also the prior outcome. The job-to-applicant ratio firmed to 1.26, versus a 1.25 forecast and 1.24 recorded in Feb.

- The chart below plots the job-to-applicant ratio, which is inverted (the white line on the chart) against the unemployment rate. Today's March prints don't really change the broader labor market picture. The unemployment rate has risen but only from recent cycle lows, while the slight uptick in the job-to-applicant ratio modestly closes some of the wedge between the two series.

- In terms of the detail, the number of employed people fell by 80k m/m following the -110k drop in Feb. The participation rate edged up to 63.3%, but is sub late 2024 highs.

- A still tight labor market should supporting underlying wage momentum, but some slowing in total people employed will be a watch point.

Fig 1: Japan Jobless Rate Versus Job-To-Applicant Ratio (Inverted)

Source: MNI - Market News/Bloomberg

JAPAN DATA: Local Investors Buy Offshore Bonds For 2nd Straight Week

Aggregate Japan weekly offshore investment flows were more muted in the week ending April 25, see the table below. Offshore investors continued to buy local stocks, marking the 4th straight week of inflows. We continue to see this segment reduce the net selling position built up since the start of the year. Cumulative outflows rest just under -¥1.8trln for 2025. We were at -¥5.6trln at the end of March. Offshore investors continued to add to local bond holdings, but only modestly. This marked the fourth straight week of inflows into this segment.

- In terms of Japan outbound flows, we did see local investors increase offshore bond purchases. We have still seen net outflows for offshore bond purchases for April though. Since the start of the year cumulative flows are close to flat.

- Local investors continued to buy offshore stocks, for the 6th straight week.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending April 25 | Prior Week |

| Foreign Buying Japan Stocks | 278.3 | 705.6 |

| Foreign Buying Japan Bonds | 60.0 | 998.1 |

| Japan Buying Foreign Bonds | 435.2 | 218.2 |

| Japan Buying Foreign Stocks | 133.8 | 610.4 |

Source: MNI - Market News/Bloomberg

JGBS: Cheaper, Trade Deal HLs In Focus, Market Closed On Mon & Tues

JGB futures are slightly higher, +5 compared to settlement levels.

- While the domestic calendar delivered labour market, monetary base and international investment flow data, it was news on trade deals that appeared to dominate the market’s attention.

- "Japanese Prime Minister Shigeru Ishiba says he was told the second round of tariff talks between his chief negotiator Ryosei Akazawa and US officials, including Treasury Secretary Scott Bessent, were "positive and constructive."(per BBG).

- There was also positive US-China trade news, with headlines that China is considering trade talks with the US (which came from the China Ministry of Commerce).

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session. US NFP will dictate price action tonight.

- Cash JGBs are 1bp richer to 5bps cheaper across benchmarks, with a steepening bias.

- Swap rates are 1bp lower to 2bps higher. Swap spreads are mixed.

- The local market is closed on Monday and Tuesday.

AUSSIE BONDS: Cheaper After Some Positive Trade Deal HLs, US NFP Due

ACGBs (YM -3.0 & XM -4.0) are cheaper but near session bests.

- While PPI and retail sales offered some domestic insights, it was offshore developments that dominated local market attention.

- In addition to positive US-China trade headlines, there were some positive trade deal comments from Japan, "Japanese Prime Minister Shigeru Ishiba says he was told the second round of tariff talks between his chief negotiator Ryosei Akazawa and US officials, including Treasury Secretary Scott Bessent, were "positive and constructive."(per BBG).

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session. US NFP will dictate price action tonight.

- Cash ACGBs are 3bps cheaper with the AU-US 10-year yield differential at -1bp.

- The bills strip -2 to -5 across contracts, with a steepening bias

- RBA-dated OIS pricing is flat to 3bps firmer across meetings today, with late 2025 leading. A 50bp rate cut in May is given a 3% probability, with a cumulative 110bps of easing priced by year-end.

- On Monday, the local calendar will see S&P Global PMI Composite & Services, Melbourne Institute Inflation and ANZ-Indeed Job Advertisements.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$1000mn of the 3.75% 21 April 2037 bond on Wednesday and A$700mn of the 2.75% 21 November 2029 bond on Friday.

AUSTRALIA DATA: March Retail Spend Near Estimates, But Q1 Volume Spend Flat

The headline retail sales print for March was close to expectations, rising 0.3%m/m (+0.4% was forecast, while the Feb rise was 0.2%). The strongest segments were food up 0.7%m/m, while other retailing rose 0.7%. Drags came from department stores, off 0.5%, which was its first decline since Sep last year. Cafes, restaurants were down 0.5%m/m as well.

- The ABS noted: Retail turnover rose in all states and territories, except for Queensland (-0.4 per cent) as Ex-Tropical Cyclone Alfred negatively impacted spending. ‘The extreme weather early in the month led to significant disruptions for businesses and households throughout Queensland."

- In y/y terms spending was up 4.3% so fairly close to recent highs ( 4.6%y/y from Dec last year).

- In volume terms though, spending was flat for Q1, against a +0.3% forecast. Q4 of last year was revised down to a 0.8% gain, from +1.0%.

- The ABS noted: ‘Retail sales volumes were flat this quarter and reflected subdued spending. This comes after sustained promotional activity boosted discretionary spending in late 2024,’ Mr Ewing said." And: " Retail volumes on a per capita basis fell 0.4 per cent after growth in the previous two quarters."

- Household goods fell -1.9%q/q, after two solid quarters of growth in Q3/Q4 last year.

- Overall, this suggests some loss of real spending momentum after some pick up in the second half of last year.

BONDS: NZGBS: Closed With A Twist-Flattener After Trade HL-Induced Volatility

NZGBs closed showing a twist-flattener, with benchmark yields 1bp higher to 2bps lower, after a volatile pre-US payrolls session. NZGBs had 7-8bp ranges.

- The Asian session has seen risk trade well as the market attempts to look through the negative earnings of Apple and Amazon to concentrate on some positive US-China trade headlines. As well as some positive trade deal comments from Japan, "Japanese Prime Minister Shigeru Ishiba says he was told the second round of tariff talks between his chief negotiator Ryosei Akazawa and US officials, including Treasury Secretary Scott Bessent, were "positive and constructive."(per BBG).

- Cash US tsys are 1-3bps cheaper in today’s Asia-Pac session. US NFP will dictate price action tonight.

- Swap rates closed 1-2bps higher.

- RBNZ dated OIS pricing closed flat to 4bps firmer across meetings, with early-2026 leading. 26bps of easing is priced for May, with a cumulative 78bps by November 2025.

- The local calendar will be on Monday, ahead of ANZ commodity prices on Tuesday. The data highlight, however, is likely to be the Q1 Employment Report.

FOREX: G10 Wrap - Can The USD follow through?

The BBDXY has had an Asian range of 1225.86 - 1231.01, Asia is currently trading around 1226. The USD has given back some overnight gains as China made comments interpreted as being open to potentially explore trade talks with the US. Bloomberg - “The EU may buy more gas and agricultural products from the US to address the trade imbalance, the FT reported, citing the bloc’s Trade Commissioner Maros Sefcovic.” Reuters - “ Ryanair threatens to cancel huge Boeing order if tariffs raise prices.”

- EUR/USD - Asian range 1.1274 - 1.1316, Asia is currently trading 1.1305. Intra-day support is around the 1.1250 area, should this area not hold demand should remerge on dips back to 1.1100.

- GBP/USD - Asian range 1.3274 - 1.3314, Asia is currently dealing around 1.3305. Intra-day support is around the 1.3250 area, then the pivotal 1.30/31 support is next.

- USD/JPY - Asian range 145.15 - 145.92, has drifted sideways for most of the Asia session. USD/JPY broke the 144.00 resistance yesterday and has quickly moved to the next level of resistance. The 145.50/1.4700 area should be tough to get through initially, watch price action around this crucial area as the bears try to wrest control back once more.

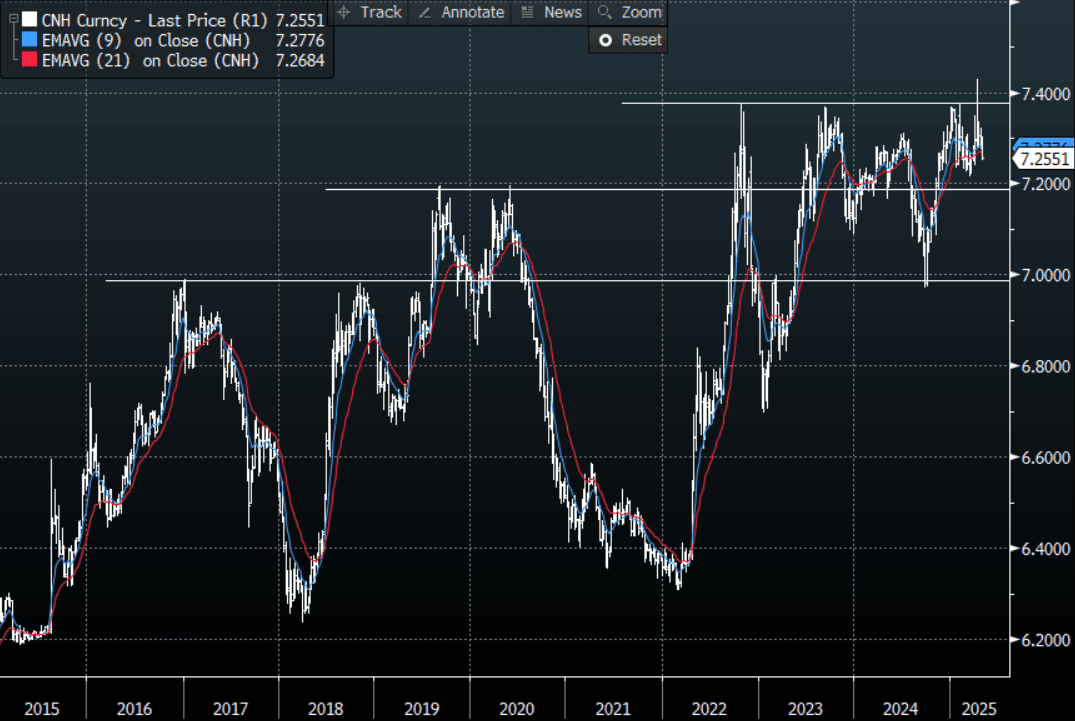

- USD/CNH - Asian range 7.2518 - 7.2808, Chinese stock markets are shut for a holiday. The longs in Usd/Asia are starting to be pared back, this was perceived to be the cleanest expression of the Tariff trade but this move lower in the USD is now starting to bite.

- Cross asset : SPX +0.81%, Gold $3254, US 10-Year yield 4.23%, BBDXY 1226, Crude oil $59.69.

- Data/Events : Dutch CPI, IT Unemployment, US NFP

Fig 1: USD/CNH Spot Weekly Chart

Source: MNI - Market News/Bloomberg

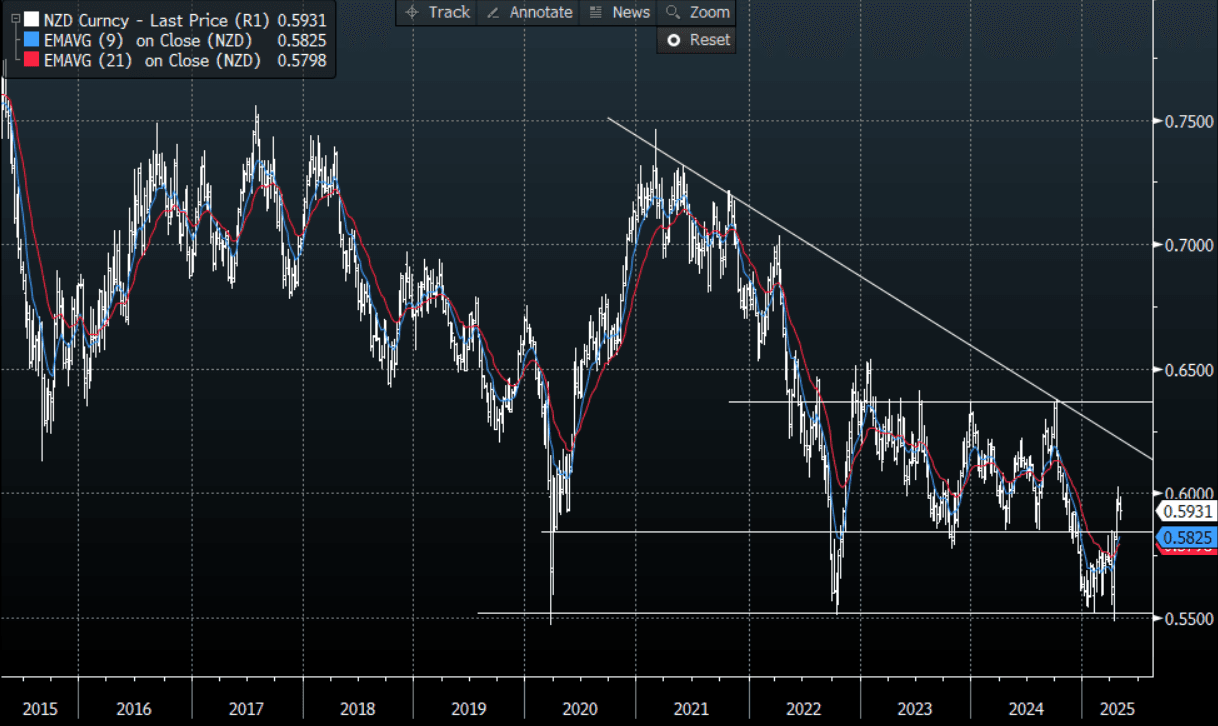

FOREX: Antipodean Wrap - AUD & NZD Continue To Outperform

The Asian session has seen risk trade well this morning as the market attempts to look through the negative earnings of Apple and Amazon to concentrate on some positive US-China trade headlines. As well as some positive trade deal comments from Japan, “Japanese Prime Minister Shigeru Ishiba says he was told the second round of tariff talks between his chief negotiator Ryosei Akazawa and US officials including Treasury Secretary Scott Bessent was “positive and constructive.”(per BBG). NFP will dictate price action tonight.

- AUD/USD - Asian range 0.6375 - 0.6420, the AUD is currently dealing around 0.6415. While the support around 0.6350 holds the focus will be on building upward momentum. The AUD looks to be building a solid base from which to move higher again, first target the 0.6600 area.

- AUD/JPY - Asian range 92.64 - 93.48, price goes into London trading around 93.20. AUD/JPY broke the resistance around 92.00 yesterday and has had a powerful extension as shorts are pared back, short term this move could have more to go. Weekly resistance seen between 94.00/96.00 should see sellers remerge.

- NZDUSD - Asian range 0.5894 - 0.5938, going into London trading around 0.5930. With support having held once more around 0.5900, a move above 0.5950 could see the move higher build momentum again.

- AUD/NZD - Asian range 1.0785 - 1.0823, the Asian session currently trading 1.0810. Sellers could be expected again back towards the 1.0850 area.

Fig 1 : NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Strong Day as Trade Agreements Rumours Evolve

With China out today, equity markets remained quiet despite the ongoing headlines that China's Commerce Ministry said it is evaluating the possibility of trade talks with the US, after senior US officials expressed willingness to talk to Beijing about tariffs. Despite the comments the ministry was still demanding that the US show sincerity towards China and its wrong practices; suggesting that the chances of Beijing bowing to Washington’s pressure remains low.

Markets were buoyed by the news and mainly green could be viewed across trading screens with gains in all major markets.

- Taiwan’s TAIEX was the best performer up +2.2% and on track to finish over 4% higher for the week, an 18% gain since the low on 09 April.

- The KOSPI had a positive day, rising +0.32% to take back yesterday’s losses and remain on track to finish the shortened week with a +0.75% gain.

- As Malaysia prepares for a rate decision next week, weaker PMIs weighed heavy on the FTSE Bursa Malay KLCI which was one of the few markets to fall. Down -0.15% for the day, it remains over +1.5% higher for the week.

- In Indonesia the Jakarta Composite has been on a tear of late and despite weak PMIs is up +0.35% today and over +1.5% for the week to deliver its third successive positive week and be 13% higher than the lows of 09 April.

- Singapore’s Straits Times gained +0.30% and the PSEi in the Philippines over 1% gain.

- India’s NIFTY 50 is up +0.88% today as news circulates that India could be one of the first to finalize their trade deal. The index is on track to deliver a 2% gain this week for three successive weeks of gains.

Oil Set for Another Big Weekly Drop (UPDATED)

- Oil had its strongest day of the week as WTI rose as further threats of Iranian sanctions permeated through oil markets.

- Trump stated clearly that the US will sanction any nation or person who buys oil or petrochemicals from Iran in breach of sanctions driving prices higher.

- Additionally, a prominent US Senator and known supporter of Trump has stated publicly that he has the commitment of 72 colleagues on a bill to further sanction Russia and those countries that continue to source their oil from the Kremlin.

- These threats added to the news overnight that April OPEC+ production fell by 200,000 barrels a day due to the winding down of operations in Venezuela by US producers as the threat of increased sanctions gets closer.

- US crude inventories declined by 2.7 million barrels, the biggest fall in more than a month, to around 440.4 million barrels. Refineries processed the most crude since 2019 for this time of year, with oil processing improving in all regions except the Midwest. Gasoline inventories saw a 4 million-barrel decline, driven by a large drawdown in the Midwest, to the lowest since late December.

- In a move that would add more supply to the global outlook, House Republicans plan to raise more than $15 billion in revenue through increasing US oil, gas and coal lease sales, as well as other measures, to help pay for President Donald Trump’s massive tax cut package, according BBG

- WTI finished the US trading session at US58.98 bbl yet has opened in the Asia trading day lower initially before rallying back in the afternoon to be +1.1% better

- Despite today’s gains, WTI is set for a decline of over 5% for the week.

- Brent had opened in the Asia trading session at $61.82 and climbed steadily throughout the trading day to reach $62.52, a gain of 1%.

- Despite the gain, Brent is on track for a loss of over 6% for the week.

Gold Set for Biggest Drop Since February

- Gold’s overnight fall tempered in Asia as markets assessed the latest headlines on trade negotiations.

- Having exhibited ‘safe-haven’ status in recent months as tariff headlines buffeted markets, gold had risen at one point 27% year to date.

- It is now more than 5% off its April high of US$3,423.98 and opened the Asia trading data at $3,239.21 having lost -1.50% yesterday.

- Gold managed gains today up +0.51 yet is down over 1.9% for the week at $3,255.91.

- The move overnight sees gold trade below the 20-day EMA of $3,246.90 with the next key technical level the 50-day EMA at $3,115.31

- Gold remains up over 20% this year on trade war concerns and renewed support by Central Banks.

- For gold, the key focus now will likely return to interest rates and the next FED decision as tonight sees the release of the Non-Farm Payrolls.

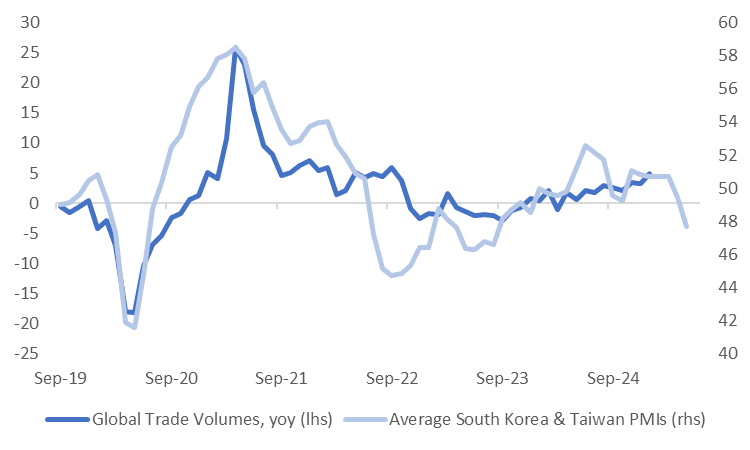

ASIA: Weaker South Korea & Taiwan PMIs Pointing To Slower Trade Growth

South Korea's April PMI fell to 47.5 from 49.1 in March. This is the lowest reading since Sep 2022. The index was at 50.3 in Jan of this year. Output fell to 46.9 from 48.6, which was the lowest reading since mid 2023. New orders were also down, which are also at their lowest level since the middle of 2023.

- Taiwan's PMI fell to 47.8, which is fresh lows back to early 2024. End 2024 levels for the index were back near 53.00. The index did get sub 42.00 in 2022, so we remain above those lows.

- Output for Taiwan's PMI fell to 47.4 from 50.5. Like South Korea, new orders also fell, back to lowest levels since Dec 2023.

- The chart below plots the average of the South Korea and Taiwan PMI levels against global trade volumes in y/y terms. The weakness in the PMI reads is pointing to lower trade volumes growth as we progress through Q2.

Fig 1: Average South Korean & Taiwan PMIs Versus Global Trade Volumes Y/Y

Source: MNI - Market News/Bloomberg

ASIA: PMIs Showing Trade War Strains in April

- A raft of PMIs were released this morning for Asian nations and it is hard not to suggest that the trade war and US tariffs have contributed negatively to the outcome for some.

- Indonesia’s PMI cratered to 46.7, it’s lowest result since August 2021 during a period where political uncertainty drove concerns as to the fiscal position for the country at the same times the US threatened sanctions. The result for Indonesia saw the fall from March’s 52.4 with the 5-year average at +51.5. Output collapsed to +44.3 (from 53 in March) and new orders were the lowest in 4 years

- Malaysia’s April PMI fell into contraction also, marking its lowest reading since late 2024 and the dubious honor of eleven straight months of contracting. April saw a decline to +48.6 from +48.8 in March. Output declined further to +47.4 from +48.4 whilst new orders rose relative to the prior month.

- The Philippines was the standout with April’s result of +53.0 its highest reading this year; with output jumping to +54.9 (from 48.7) and new orders higher relative to the prior month.

- Thailand’s PMI slipped into contraction in March and April saw a further decline at a time with the Bank of Thailand Governor warned that the impact of the trade war could be severely detrimental to the economy. April PMIs declined to +49.5 the lowest in a year yet there may be signs of stabilizing as output rose to +50.3 whilst new orders declined again.

SOUTH KOREA: CPI Causes No Concern for the BOK

- April’s CPI was largely benign as CPI oscillates around the BOK’s 2.% target.

- The April CPI y/y printed in line with the prior month at +2.1%

- The month on month result of +0.1% was lower than the month prior of 0.2%

- The contraction in GDP in Q1 and the uncertainty from tariffs has put downward pressure on activity which has seen the Bank of Korea cut three times since Q3 last year.

- Bond markets continue to see some room for rate cuts with 66bps of cuts priced in over the next 12 months but only 14bps for the next three.

- The BOK next meets on May 29, not long before the next presidential election.

INDONESIA: CPI Up Again in April.

- Indonesia’s CPI in April rose +1.95% YoY beating estimates of +1.50% YoY and up on March’s result of +1.03%.

- Core CPI was relatively stable at 2.50%, following March’s 2.50% result. The Central Bank - Bank Indonesia has an inflation target of +1.5%-3.5% for headline.

- The MoM figure saw a modest rise also to 1.17% from 1.02%

- The decline in CPI reached a low of -0.09 in February with the primary driver for this deflation was a 50% electricity discount implemented in January and February.

- CPI has continued to inch back up since and whilst today’s result will hold present no concerns for the BI for now, they will be cognizant of a near 1% jump in March and April.

- The PMI’s today point to the impacts of the trade war and tariffs and with that the potential for inflationary pressures exist and one that the BI will be keen to contain.

- The Indonesia 10YR is marginally lower by ½ bp today at 6.87%

ASIA FX: USD/TWD Collapses Amid US-China Trade Hopes, Stronger Equities

In North East Asia, FX sentiment has been firm, particularly for TWD, posting its biggest intra-day gain since 2011 (per BBG). USD/KRW is also lower shrugging off local political concerns, while USD/CNH has lagged these downside moves. Onshore markets in China remain closed until next Tuesday.

- South Korean and Taiwan PMIs fell in April, amid negative trade sentiment. The average of these indices is pointing to slower global trade growth. Still, sentiment was buoyed by headlines from the China Commerce Ministry that it is assessing the US request for trade talks. There are still lots of caveats but the market drew hope that discussions may take place, which in turn could lead to a lowering in trade tensions.

- USD/CNH is eyeing a downside test sub 7.2500, but has been supported around the 200-day EMA in Friday trade to date. Further south is the simple 200-day MA (near 7.2230). The pair couldn't sustain tests below this support level in March. Hong Kong markets are up firmly, aided by trade hopes, the HSI last +1.6%.

- USD/TWD has collapsed. The pair got to session lows of 31.154, but we sit up around 31.30/35 in latest dealings, still +2.1% stronger in TWD terms. US-China Trade hopes has seen TWD outperform, while local equities are up over 2%. Some recent tech results which still hint at firm AI related demand a likely positive. Taiwan's GDP beat from late on Wednesday is also likely aiding the currency (local markets were shut yesterday). The pair is oversold based off RSI (14), but the trend is clearly skewed lower. If we can break sub 31.00, note that late 2023 lows were around 30.65.

- Spot USD/KRW initially lagged softer USD/Asia trends, with yesterday's resignation of the Finance Minister adding to the onshore political turmoil. The pair got to highs near 1440, but we sit back near 1420 in latest dealings. The won has clearly lagged the TWD move though.

INDIA: Country Wrap: PMIs Show the Gap Between Regional Peers

- On a day where (with the exception of the Philippines) all regional Asian PMIs slipped to contraction, India’s April PMI stands out and shows the gap emerging. At 58.2 it is the strongest PMI of its peer group and has remained extremely resilient despite the US trade war. The reading was the highest since the middle of 2024 with output up at +61.9 despite new orders dipping from last month’s release. It has been a remarkable period for India’s PMIs with a 5-year average of 56.8. (source MNI Market News)

- Vice President Vance says a trade deal with India is imminent will be one of the first and any deal will fundamentally open the country to American technology and agriculture (source BBG).

- India's NIFTY 50 is up +0.88% today as news circulates that India could be one of the first to finalize their trade deal. The index is on track to deliver a 2% gain this week for three successive weeks of gains.

- The rupee has had a strong week gaining 1.8% to be at 83.90

- Bonds have had a good week on the back of the announcement for May’s OMO seeing significant purchases of government bonds to come. IGB 10YR 6.35% (-1bp today)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/05/2025 | 0630/0730 | DMO to announce details of long syndication for W/C 19 May | ||

| 02/05/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0900/1100 | *** | HICP (p) | |

| 02/05/2025 | 0900/1100 | ** | Unemployment | |

| 02/05/2025 | 1230/0830 | *** | Employment Report | |

| 02/05/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 02/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |