STIR: BoJ-Dated OIS Pricing Softer After BoJ Forecast Downgrades

May-02 02:46

BoJ-dated OIS pricing has softened by 1-5bps compared to pre-MPM levels, despite the market having had priced in a cautious, wait-and-see stance from the BoJ at yesterday's meeting.

- As widely expected, the BoJ left its policy rate unchanged at 0.50%, which was a unanimous decision of 9-0 by the board.

- The economic outlook was downgraded though in terms of both lower GDP and inflation forecasts. It also noted prices and growth risks for the 2025 and 2026 fiscal years rest to the downside.

- The central bank retained its bias that if the outlook is realised it will raise rates further, but the central bank places a caveat on those given extreme uncertainties around the trade outlook.

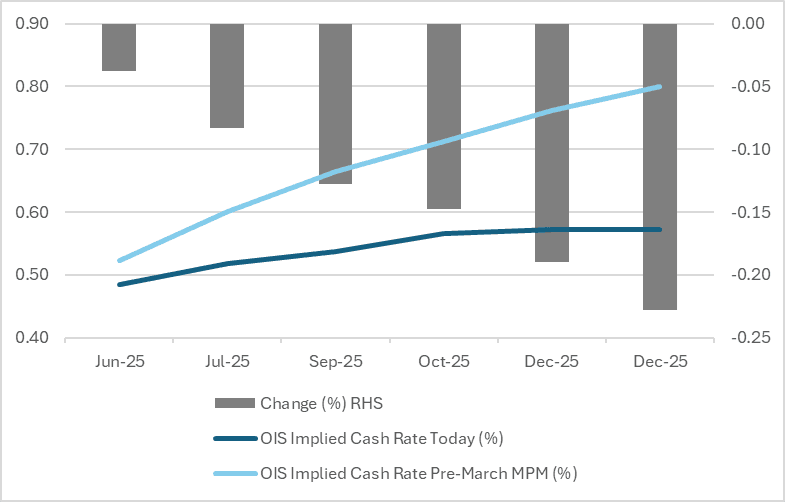

- Current OIS pricing assigns just a 3% probability of a 25bp hike at the June meeting, a cumulative 24% probability by September, and a 38% probability by December — a sharp shift from mid-February, when a hike by September was fully priced in.

- December pricing is now almost a full 25bp hike lower than the pre-March MPM level.

Figure 1: BoJ-Dated OIS – Today Vs. Pre-March MPM

Source: MNI – Market News / Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: MNI Discusses Potential Support For China Property Developers

Apr-02 02:42

MNI discusses potential incoming support aimed at China's property developers. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

CHINA: Bond Futures Rally Ahead of Tariff News.

Apr-02 02:27

- China bond futures are up across all maturities as the equity markets pause ahead of the White House press conference on tariffs.

- The 10YR future is up +0.13 to 107.905, recovering yesterday’s losses.

- The 10YR is within touching distance of the 100-day EMA of 107.92.

- All major trend lines have flattened indicating no strong directional bias at present

- The 2YR future is up +0.03 to 102.382, after yesterday’s loss of -0.04.

- The 2YR future remains below all major moving average trend lines with the closest the 20-day EMA at 102.426.

- Cash market remains subdued with the CGB 10YR at 1.80% (-0.5bps today).

- With no key data releases today, tomorrow sees the Caixin PMI Services and Composite.

AUD: A$ Generally Stronger Ahead Of US Tariff Announcement, AUDNZD Lower

Apr-02 01:58

AUDUSD is approaching its earlier intraday high of 0.6291 and is currently 0.2% higher during today’s APAC session at 0.6290 as markets wait for details on US reciprocal tariffs due to be announced at 1600 ET or 0700 AEDT Thursday. The USD index is unchanged.

- Aussie strengthened further against the yen after the pair rose 0.2% yesterday. AUDJPY is up 0.3% to 94.21 today, close to the intraday high of 94.25. AUDEUR is 0.1% higher at 0.5825 and AUDGBP +0.2% to 0.4867. These gains could be unwound though if US tariffs are seen as worse than expected; a scenario which would likely drive a pullback in risk.

- The AUD is 0.1% lower against risk-sensitive kiwi at 1.1003. It has again found support at 1.1000 and is currently hovering around this level.

- Equities are mixed with the ASX up 0.2%, CSI 300 flat but the Hang Seng down 0.6% and S&P e-mini -0.1%. Oil prices are little changed with WTI around $71.20/bbl. Copper is up 0.3% and iron ore around $104/t.

- Apart from the US tariff announcement, the Fed’s Kugler speaks on inflation expectations and March US ADP employment and February orders are released. The ECB’s Lagarde, Schnabel and Lane talk.