FOREX: G10 Wrap - Can The USD follow through?

The BBDXY has had an Asian range of 1225.86 - 1231.01, Asia is currently trading around 1226. The USD has given back some overnight gains as China made comments interpreted as being open to potentially explore trade talks with the US. Bloomberg - “The EU may buy more gas and agricultural products from the US to address the trade imbalance, the FT reported, citing the bloc’s Trade Commissioner Maros Sefcovic.” Reuters - “ Ryanair threatens to cancel huge Boeing order if tariffs raise prices.”

- EUR/USD - Asian range 1.1274 - 1.1316, Asia is currently trading 1.1305. Intra-day support is around the 1.1250 area, should this area not hold demand should remerge on dips back to 1.1100.

- GBP/USD - Asian range 1.3274 - 1.3314, Asia is currently dealing around 1.3305. Intra-day support is around the 1.3250 area, then the pivotal 1.30/31 support is next.

- USD/JPY - Asian range 145.15 - 145.92, has drifted sideways for most of the Asia session. USD/JPY broke the 144.00 resistance yesterday and has quickly moved to the next level of resistance. The 145.50/1.4700 area should be tough to get through initially, watch price action around this crucial area as the bears try to wrest control back once more.

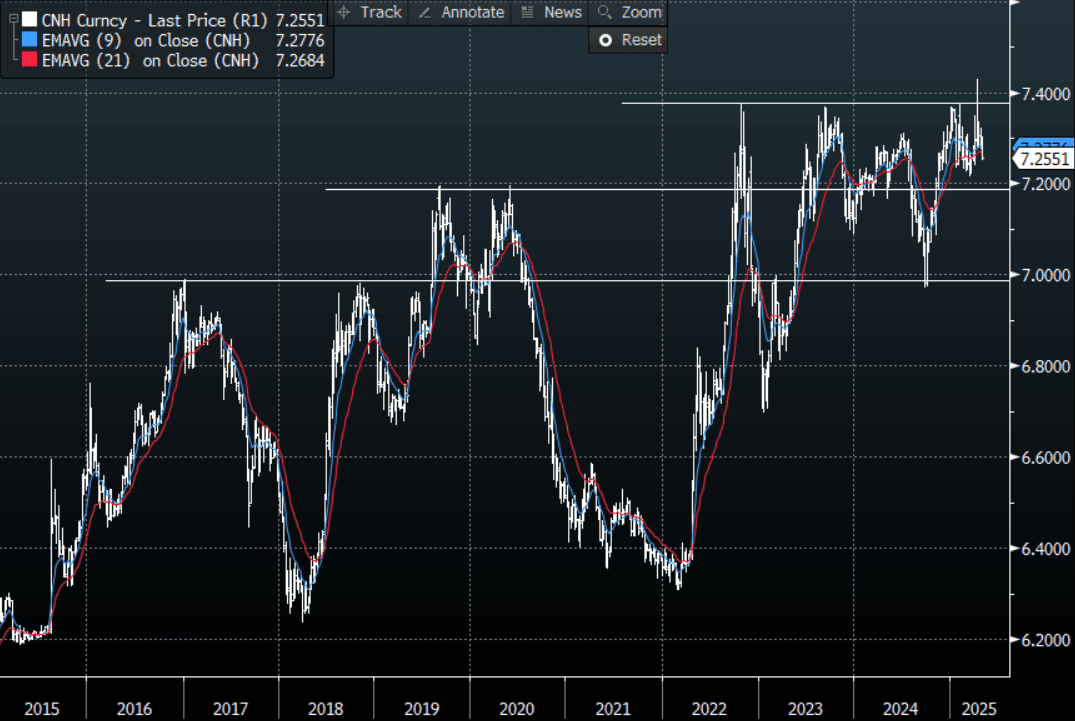

- USD/CNH - Asian range 7.2518 - 7.2808, Chinese stock markets are shut for a holiday. The longs in Usd/Asia are starting to be pared back, this was perceived to be the cleanest expression of the Tariff trade but this move lower in the USD is now starting to bite.

- Cross asset : SPX +0.81%, Gold $3254, US 10-Year yield 4.23%, BBDXY 1226, Crude oil $59.69.

- Data/Events : Dutch CPI, IT Unemployment, US NFP

Fig 1: USD/CNH Spot Weekly Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Cash Bond Bull-Flattener Going Into US Liberation Day News

JGB futures are stronger and near session highs, +14 compared to settlement levels.

- Outside of the previously outlined monetary base date, BoJ Governor Ueda has stated that US tariffs could significantly impact trade activity in affected nations, depending on their size and area. Ueda expressed uncertainty about the overall picture of the policies, awaiting an official announcement, and will closely watch developments to grasp their economic impacts.

- “The Japanese government will continue to strongly urge the US to exempt Japan from tariff measures, while assessing the details and potential impact on the country, Finance Minister Katsunobu Kato says” (per BBG)

- Cash US tsys are ~2bps cheaper ahead of Wednesday afternoon's Liberation (tariff) Day announcement from the White House (1600ET est). Trump's tariffs will take immediate effect after they are announced. Today's US calendar will see ADP Employment Change and Factory Orders data, and Fedspeak from Kugler on Inflation Expectations.

- Cash JGBs have bull-flattened, with yields flat to 3bps lower. The benchmark 10-year yield is -0.4bp at 1.495% versus the cycle high of 1.596%.

- Swap rates are little changed. Swap spreads are mixed.

- Tomorrow, the local calendar will see Weekly International Investment Flow and Jibun Bank Composite & Services PMIs data.

FOREX: A$ & NZD Outperform Yen Ahead Of US Tariff Announcement

AUD and NZD gains, against both the USD and JPY, have been the main focus points in the first part of Wednesday trade G10 FX trade. The USD BBDXY index was last just under 1273, a touch below end Tuesday levels in NY. Focus remains firmly on the US reciprocal tariff announcement, later on Wednesday US time (4pm EST).

- We had a number of news wire stories related to tariffs towards the tail end of the US Tuesday session/early Asia Pac trade. To recap:

A CNBC reporter posted on X, citing Republican Rep. Kevin Hern, that the tariff rates announced Wednesday will be the highest they will go and countries can then take steps to bring the tariffs down. This reportedly followed a meeting with US Tsy Secretary Bessent. - The WSJ also noted earlier the USTR is preparing another tariff option for Trump: ""The U.S. Trade Representative's office is preparing a third option of across-the-board tariff on a subset of nations that likely would not be as high as the 20% universal tariff option, according to people with knowledge of the plans."

- There was also a Washington Post article around the use of tariff revenue to support the economy, including options for a tax dividend or refund, but these plans are reportedly only in the very early stages.

- US equity futures re-opened higher, but positive momentum waned and we were last -0.10% for Eminis. US Tsy yields are higher across the benchmarks, up 2bps for the 10yr to 4.19%. This has likely helped nudge USD/JPY a little higher, but at 149.80/85 we are only marginally above end Tuesday levels. EUR/USD is holding under 1.0800.

- AUD and NZD have ticked up. AUD/USD last near 0.6300, while NZD/USD is back to 0.5720, slightly outperforming the AUD. Both currencies are firmer against the yen and challenging 20-day EMA resistance points. AUD/JPY was last near 94.35/40, while NZD/JPY was at 85.70/75.

- Looking ahead, apart from the US tariff announcement, the Fed’s Kugler speaks on inflation expectations and March US ADP employment and February orders are released. The ECB’s Lagarde, Schnabel and Lane talk.

AUSSIE BONDS: Little Changed Ahead Of Trump Tariff Announcement

ACGBs (YM -1.0 & XM +1.0) are little changed after dealing in narrow ranges in today's local session.

- There was a small payback in February non-house building approvals. Nevertheless, looking through the volatility the total number is trending robustly higher.

- Cash US tsys are ~2bps cheaper ahead of Wednesday afternoon's Liberation (tariff) Day announcement from the White House (1600ET est). Today's US calendar will see ADP Employment Change and Factory Orders data, and Fedspeak from Kugler on Inflation Expectations.

- Cash ACGBs have bear-flattened, with yields flat to 2bps higher, with the AU-US 10-year yield differential unchanged. At +22bps, the differential is approaching the top of the range that it has traded in since late 2022.

- The latest round of ACGB May-34 supply sees the weighted average yield print 0.35bps through prevailing mids, with the cover ratio of 3.9125x was significantly higher than at the previous auction.

- Swap rates are flat to 1bp lower, with EFPs tighter.

- The bills strip is little changed.

- RBA-dated OIS pricing is slightly softer today. A 25bp rate cut in May is given a 77% probability, with a cumulative 71bps of easing priced by year-end.

- Tomorrow, the local calendar will see S&P Global Composite and Services PMIs.