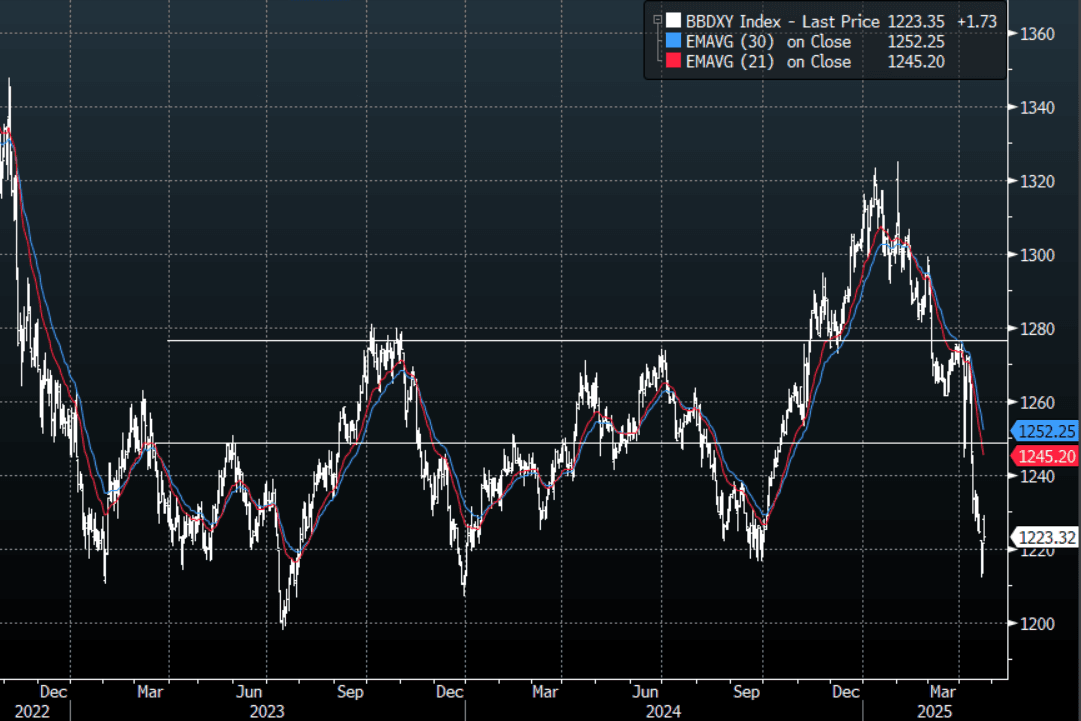

MNI EUROPEAN MARKETS ANALYSIS: Risk Firms On Trump Comments

- Risk appetite continued to firm in the equity space as US President Trump stated he has no intention of firing Fed Chair Powell. He also stated final tariff levels for China will be below the 145% level which currently prevails.

- The USD shot higher, but sits comfortably off best levels in index terms. US Tsy yields are lower at the back end of the curve. Gold fell sharply but is also up from lows.

- The IMF/World Bank & G20 finance ministers/central bank governors meetings take place. The ECB’s Lane and Cipollone participate in panels and BoE’s Bailey and Breeden also appear, while BoE’s Pill speaks at another event.

MARKETS

US TSYS: Asia Wrap - Yields Drift Lower In The Long End

TYM5 has traded higher with a range of 110-20 to 111-00+ during the Asia-Pacific session. It last changed hands at Heading 110-29, up 0.04 from the previous close.

- The US 10-year yield is drifting lower, dealing around 4.34%, down from its open around 4.40%

- The US 2-year yield is unchanged, dealing around 3.81%

- Risk has reversed higher as Trump makes a U-turn saying he won’t fire Powell and made comments that seemed to soften his stance towards China.

- Block Curve flattener flows : SELL 8200 of USM5 traded at 108-06, post-time 01:25:20 BST (DV01 $353,017). BUY 2800 of USM5 traded at 114-22, post-time 01:25:20 BST (DV01 $353,492).

- 10-year Yields, having bounced off their support around the 4.25 area, yields are consolidating with the range looking something like 4.25/4.50% for now.

- Data/Events : US S&P Global Services & Manufacturing PMI, New Home sales

JGBS: Futures Off Lows, Twist-Flattener Remains, PPI Services Tomorrow

JGB futures are weaker but at session highs, -14 compared to settlement levels

- Risk-on sentiment extended into today's Asia-Pacific session after US President Trump stated that he had no intention of firing Fed Chair Powell.

- Trump also stated that the final tariff number for China wouldn't be near the current 145%.

- Cash US tsys have twist-flattened in today's Asia-Pac session, with yields 2bps higher to 8bps lower.

- While attention has been mostly focused abroad, the latest Reuters Poll on the BoJ Outlook showed: 84% of economists expect the BoJ to keep the key interest rate at 0.50% through end-June. 52% predict a rate hike to 0.75% in Q3, down from 70% in the March poll. Only 28% now expect a July hike, compared to 70% in March; 23% foresee the next hike happening in 2026 or later. 87% say Japan is unlikely to enter a recession in 2025.

- The cash JGB curve has twist-flattened, pivoting at the 20-year, with yields 2bps higher to 6bps lower.

- The swaps curve has also twist-flattened, with rates 2bps higher to 5bps lower.

- Tomorrow, the local calendar will see PPI Services, International Investment Flow and Machine Orders data alongside 2-year supply.

AUSSIE BONDS: Twist-Flattener, IMF Panel Discussion For RBA Gov

ACGBs (YM -6.0 & XM +1.5) are dealing mixed on a data light Sydney session, with the short-end under pressure as markets re-assess tariff-tied risks to global trade and the Trump Admin's efforts to meddling with the Federal Reserve's independent policy making.

- Risk-on sentiment extended into today's Asia-Pacific session after US President Trump stated that he had no intention of firing Fed Chair Powell.

- Trump also stated that the final tariff number for China wouldn't be near the current 145%.

- Cash US tsys have twist-flattened in today's Asia-Pac session, with yields 2bps higher to 8bps lower.

- Cash ACGBs are 5bps cheaper to 1bp richer with the AU-US 10-year yield differential at -10bps.

- Today’s auction of the Apr-29 bond saw the weighted average yield settle 0.88bps below the prevailing mid-yield. However, the cover ratio declined dramatically to 3.2200x from 4.2143x at the previous auction.

- Swap rates are flat to 5bps higher, with the 3s10s curve flatter.

- The bills strip is cheaper with pricing -4 to -9.

- RBA-dated OIS pricing is 2-11bps firmer across meetings today. A 50bp rate cut in May is given a 13% probability, with a cumulative 114bps of easing priced by year-end.

- Tomorrow morning, RBA Governor Bullock will participate in a panel discussion at the IMF Spring Meetings.

AUSTRALIA: Q1 NZ CPI Data Suggest Australian Services Inflation Moderated

Q1 Australian CPI data is released on Wednesday April 30 and will be an important input into the May 20 RBA decision, where a rate cut is largely expected. There are high correlations between NZ and Australian CPI data and given NZ’s Q1 has already been released, there are possibly trends that we can ascertain. Australia may see a pickup in goods inflation, while sticky services may moderate.

- NZ headline, non-tradeables & tradeables printed higher than expected but both headline and core were in the RBNZ’s 1-3% target band at 2.5% y/y and 2.9% y/y respectively.

- With government electricity rebates continuing to reduce Australia’s headline inflation, there is little to be gained by looking at NZ’s trends here.

- There is a 3-year rolling correlation of around 90% between Australia/NZ underlying inflation measures. The RBNZ’s sector factor model estimate of core moderated 0.1pp to 2.9% in Q1. In addition, Australia’s monthly data are pointing to a moderation in quarterly trimmed mean inflation in Q1.

Australia vs NZ core CPI y/y%

- Domestically-driven services inflation has been monitored closely for some time and the Australia/NZ correlation is also close to 90%. NZ services inflation moderated 0.6pp to 4.2% y/y and non-tradeables 0.5pp to 4.0% y/y, which is good news for Australia.

- Australia is likely to see a pickup in goods inflation, which is significantly determined by global factors. It rose to 1.4% y/y in NZ from 0.6% signalling that its disinflationary pressure is likely over, consistent with Australia’s monthly goods inflation data.

Australia vs NZ services y/y%

AUSTRALIA DATA: Exports & Confidence Impacted By Protectionism

The S&P Global preliminary April PMIs showed steady but moderate growth at the start of Q2 with the composite at 51.4 down slightly from 51.6 with services printing inline. Manufacturing activity eased slightly with the PMI at 51.7 after 52.1 in March, but the fourth consecutive month in positive territory after spending most of 2024 contracting. Strength was driven by the domestic economy though with global trade developments weighing on exports and confidence.

- Growth in new business rose in April to its fastest in two years with strength coming from services but manufacturing also saw a moderate pickup. This drove continued hiring, which remains at a 23-month high, but also the strongest rise in outstanding business in almost three years, according to S&P Global.

- Stronger demand resulted in a deterioration in the inflation picture with firms able to pass on higher costs to customers. Input inflation remains elevated driven by raw materials, energy, wages and imports due to the weaker AUD. Selling price increases rose this month with manufacturing at its fastest in more than 2 years.

- New business appears to be concentrated in the domestic economy though with exports falling for the second straight month due to increased uncertainty over US trade policy.

- Fears of a global trade war and resulting slower global growth weighed on confidence regarding the outlook with it falling to its lowest in 6 months.

Australia S&P Global PMIs

AUSTRALIA: Minority Government Distinct Possibility As Focus On Certain Seats

Australia holds its federal election on May 3 and as the date approaches the incumbent Labor Party (ALP) has increased its share of both the primary and 2-party preferred vote across opinion polls. If the actual result comes in close to the surveys, which are currently around the 2022 outcome, then Labor could hold its small majority in the House of Representatives but trends are unlikely to be uniform across seats and the risk of a minority government remains high.

Australia average of opinion polls - 2-party preferred %

Source: MNI - Market News/Wikipedia

- The ALP had been behind the opposition LNP in the important 2-party preferred measure (Australia has a preferential voting system) from September last year but turned that around once the election campaign officially began.

- Polls in April are showing that the ALP could achieve a primary vote of around its May 2022 33% result with a 2-party preferred possibly around 2022’s 52.1%. It is difficult to ascertain if that will allow it to keep its 2 seat majority of 77 as outcomes in individual seats will be particularly important given the high number of incumbent and candidate independents as well as local issues.

- The average of recent surveys is showing that in terms of percentages the 2025 election could be very similar to 2022 with the average of the last 3 polls (Freshwater, Newspoll, Roy Morgan) showing the centre-left ALP with 34% (+1pp), centre-right LNP 36% (unchanged), Greens (+1pp), independents 13% (+3pp) and right-wing One Nation 7% (+2pp). The 2-party preferred is in line with 2022 at 52:48 to the ALP.

- The most recent Freshwater poll taken over April 14-16 showed a seat projection of ALP 68 (-9), LNP 69 (+16), Greens 1 (-3) and other 12 (-3), which is signalling a minority government but unclear of which persuasion. This poll reinforces the importance of the outcomes in individual seats.

Australia average of opinion polls - primary vote %

BONDS: NZGBS: Closed Slightly Cheaper, Focus Abroad As Risk-On Extends

NZGBs closed slightly cheaper, with benchmark yields 1-2bps cheaper. With the local calendar light today, the domestic market has focused its attention abroad.

- Risk-on sentiment extended into today's Asia-Pac session after US President Trump stated that he had no intention of firing Fed Chair Powell.

- Trump also stated that the final tariff number for China wouldn't be near the current 145%. He also expressed optimism around trade deals with lots of countries and spoke of the large investment agreements reached for flows into the US.

- Cash US tsys have twist-flattened in today's Asia-Pac session, with yields 2bps higher to 8bps lower.

- The NZ–US 10-year yield differential widened by 6bps to +14bps. This places the spread roughly where it was in early March, though it's about 20bps narrower than its levels in early April.

- Swap rates closed flat to 3bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed flat to 3bps firmer across meetings, with late 2025 leading. 27bps of easing is priced for May, with a cumulative 80bps by November 2025.

- Tomorrow, the local calendar will see ANZ Consumer Confidence.

- The NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond and NZ$250mn of the 4.25% May-36 bond tomorrow.

The BBDXY had an Asian range of 1221.87 - 1229.02. With risk turning around on Trump’s U-turn on Powell and China, as well as Tesla soaring on Elon Musk saying he would be pulling back significantly from DOGE, the USD has had a decent bounce. Is this move sustainable ? Should risk continue to rally we could see some relief from short-term oversold levels but the market will see a decent bounce as an opportunity to once again fade. Bloomberg reports Emmanuel Macron is exploring the possibility of dissolving parliament and holding snap elections as soon as this fall.

- EUR/USD - Asian range 1.1308 - 1.1429, has given back all of Mondays gains and more. The EUR comes off from levels that are overbought, it's been a huge move when you consider it was trading sub 1.0400 the beginning of March. The consensus trade is now to be short USD, a short term rally would be healthy. Demand should remerge on dips back to 1.1100.

- GBP/USD - Asian range 1.3234 - 1.3338, like the EUR Asia looked to be stopping out weaker hands. Dips should be supported, first around 1.3200 then the big support towards 1.3000.

- USD/JPY - Asian range 141.49 - 143.22, large gap higher in the Asian open in what looked to be stops being executed as risk rallied. Supply returned above 143.00 and we have drifted lower for the session from then onwards. USD/JPY’s fate is tied to whether risk is able to hold onto these gains and begin a sustained rally or if this is just another bounce to be faded.

- AUD/USD - Asian Range 0.6349 - 0.6405, The initial leg higher in risk saw the AUD move lower as the USD got bought. Decent buyers emerged around 0.6350 and the AUD has moved back towards 0.6400 going into London.

- USD/CNH - Asian range 7.2922 - 7.3156, the USD/CNY fix printed at 7.2116. USD/CNH continues to trade sideways and find support towards 7.2800.

- Cross asset : SPX +1.58%, Gold 3340, US 10yr 4.35%, BBDXY 1223, Crude oil 64.22.

- Data/Events : US S&P Global Services & Manufacturing PMI, FRA PMI’s, GER PMI’s, EC PMI’s, EC Trade Balance

Fig 1 : BBDXY Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: All In The Green Amid Tariff Hopes/Trump Call On Powell

Asia Pac equity markets are all in the green, led by tech related plays and Hong Kong markets. We had strong cash gains in US markets on Tuesday, while US futures are firmly in the first part of Wednesday trade. Trump remarks have dominated sentiment, with the US President stating he had no intention of firing Fed Chair Powell (which has been a source of concern for markets recently), while also stating final tariff levels on China will be lower than the 145% that currently prevails. This followed reported comments from US Tsy Secretary Bessent that the tariff standoff is unsustainable, and he expects de-escalation with China.

- Eminis are up over 1.5%, but the contract has been unable to sustain +5400 levels. A move into 5500/5600 region would likely be needed to unnerve recent shorts for this benchmark. Nasdaq futures are +1.8% at this stage.

- Japan markets are up over 2% at this stage, with the NKY 225 trending back towards 35000. The Taiex has outperformed in Taiwan up nearly 4%, while the South Korean Kospi is up around 1.5%, above 2500 in index terms.

- Hong Kong markets have the HSI up 2.4% at the break, with the tech sub index over 3%.

- Despite appearing to soften his stance on China, onshore China markets are only a touch higher at this stage. The CSI 300 up +0.22%, lagging the gains seen elsewhere.

- Trends are slightly more modest in SEA markets, the Singapore Straits Times up around 1%, same too for JCI in Jakarta, +1.2%. Gains elsewhere though are under 1%, while Philippine markets are down slightly.

OIL: Crude Higher Again But Iran Outlook Highly Uncertain, US EIA Data Out Later

Oil prices have continued trending higher during APAC trading as risk appetite improved in relief following President Trump’s comments that he wouldn’t sack Fed Chair Powell and that China’s tariffs would finish below the current 145%. China is the world’s largest importer of crude. The USD index is off today’s high but still up 0.2%.

- WTI is 0.9% higher today to $64.23/bbl after a peak of $64.48 and is now up slightly this week but still down sharply in April. Brent is up 0.8% to $67.98 with gains above $68.00 unsustained but is currently steady on the week. The prompt spread structure is in bullish backwardation, according to Bloomberg.

- With demand/supply concerns persisting, US inventory data remain in focus. US industry-based figures showed a sharp drawdown in crude and both gasoline and distillate, suggesting demand remains solid which has contributed to today’s higher oil prices. The official EIA data is out later today.

- Significant uncertainty around the outlook for Iran’s oil exports persists after the US Treasury said there would be stricter enforcement of sanctions and introduced measures against an LPG magnate with a large shipping fleet. Iran’s foreign minister is headed to China following recent talks with the US. China is the main buyer of its oil.

- Later there is more Fedspeak with Goolsbee, Musalem, Waller, Hammack and Kugler appearing. US preliminary April S&P Global PMIs, March housing data and the Fed’s Beige Book are released. European April PMIs and euro area February trade print.

- The IMF/World Bank & G20 finance ministers/central bank governors meetings take place. The ECB’s Lane and Cipollone participate in panels and BoE’s Bailey and Breeden also appear, while BoE’s Pill speaks at another event.

GOLD: Tracking Lower For 2nd Straight Session, But Still Well Above Key Support

Gold made lows just under $3316 in the first part of trade, where liquidity was lighter amid strong USD gains. We stabilized since then but found selling interest above $3386. We last racked near $3340, still off 1.20% for the session.

- Gold has been moving in lock step with USD weakness recently, so it no surprise that we have corrected lower for bullion as USD sentiment has stabilized. Trump remarks, particularly around having no intention to fire Fed Chair Powell, has aided USD sentiment, but we sit off earlier highs though for the BBDXY index (last under 1224).

- Gold is still in a technical bullish uptrend though. Focus will be on re-testing $3500 on the upside. Initial firm support lies at $3163.5, the 20-day EMA.

SOUTH KOREA: Consumer Sentiment Edges Higher, So Do Inflation Expectations

Earlier the consumer sentiment reading for April printed. It nudged up to 93.8 from 93.4. We are up from late 2024 lows sub 90.0 for the index, but for much of the prior 12 months we were above 100, so consumer confidence is still to return to these levels.

- At face value this suggests a still tepid domestic demand backdrop. The BOK has noted this though, with its recent commentary stating that its February forecast for 2025 growth would be revised down.

- Carry over from political uncertainty, along with the trade/tariff outlook, have been headwinds for South Korean growth. The IMF revised down its 2025 growth forecasts for South Korea to 1%.

- The other focus point from this survey will be the tick up in inflation expectations. Consumers 12 month outlook rose to 2.8%, from 2.7%. We have been sticky just under this 3% level for expectations since the second half of last year.

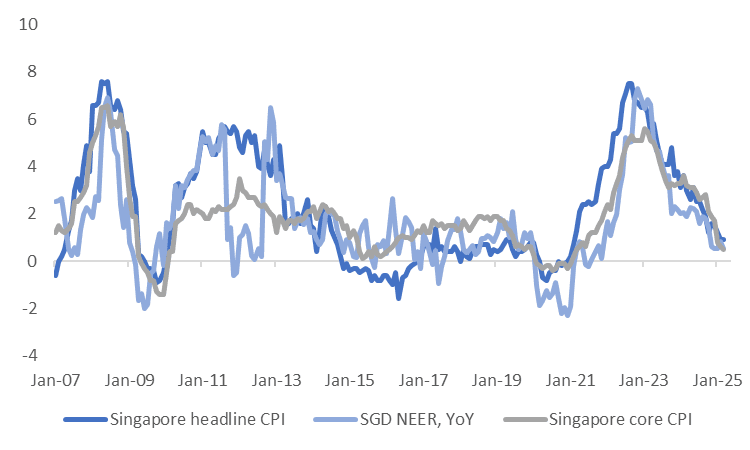

SINGAPORE: March Inflation Below Expectations, Core At Just +0.5%y/y

March inflation figures in Singapore were slightly below consensus forecasts. M/M fell -0.1%, against a 0.1% forecast, while 0.8% was the Feb outcome. In y/y terms we were 0.9%, also sub the 1.1% forecast. Core inflation printed 0.5%y/y against market expectations of a 0.7% gain. The core print fell 0.1%m/m as well.

- The detail showed clothing and footwear, household durables, transport and communication all down in m/m terms. Recreation and culture at +0.4% m/m, was the strongest sub category last month.

- In y/y terms, trends were mixed, with communication and recreation the weak points, while transport and health care were close to +2%.

- This time last year, Singapore core CPI was above 3% in y/y terms. The chart below plots this measure along with headline CPI against the SGD NEER (also y/y).

- The last MAS policy statement saw the annualized pace of SGD NEER eased but still positive. There is scope to bring this to neutral or flat at the next meeting in July, which is something supported by today's inflation data.

Fig 1: SGD NEER & Singapore Inflation Y/Y

Source: MNI - Market News/Bloomberg

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 23/04/2025 | 0600/0700 | *** | Public Sector Finances | |

| 23/04/2025 | 0630/0730 | DMO remit revision following FY24/25 CGNCR | ||

| 23/04/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 23/04/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 23/04/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 23/04/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 23/04/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 23/04/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 23/04/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 23/04/2025 | 0800/1000 | ECB Wage Tracker | ||

| 23/04/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 23/04/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 23/04/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 23/04/2025 | 0900/1100 | ** | Construction Production | |

| 23/04/2025 | 0900/1100 | * | Trade Balance | |

| 23/04/2025 | 1030/1130 | BOE's Pill speech at University of Leeds | ||

| 23/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 23/04/2025 | 1300/0900 | Chicago Fed's Austan Goolsbee | ||

| 23/04/2025 | 1330/0930 | St. Louis Fed's Alberto Musalem | ||

| 23/04/2025 | 1330/0930 | Fed Governor Christopher Waller | ||

| 23/04/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/04/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/04/2025 | 1400/1000 | *** | New Home Sales | |

| 23/04/2025 | 1400/1000 | Treasury Secretary Scott Bessent | ||

| 23/04/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 23/04/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 23/04/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 23/04/2025 | 1715/1815 | BOE's Bailey at Institute of International Finance | ||

| 23/04/2025 | 1800/1400 | Fed Beige Book | ||

| 23/04/2025 | 1800/1900 | BOE's Breeden on Monetary Policy and Financial Stability | ||

| 23/04/2025 | 1915/2115 | ECB's Lane in panel on Central Bankers' Dilemmas Amid Changing Liquidity | ||

| 23/04/2025 | 1945/2145 | ECB's Cipollone in panel on Tokenization and the Financial System | ||

| 23/04/2025 | 2230/1830 | Cleveland Fed's Beth Hammack | ||

| 24/04/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 24/04/2025 | 0700/0900 | ** | PPI | |

| 24/04/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 24/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 24/04/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/04/2025 | 1230/0830 | * | Payroll employment | |

| 24/04/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 24/04/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/04/2025 | 1300/1500 | ECB's Lane at Peterson Institute Webcast on Monetary Policy Strategy | ||

| 24/04/2025 | 1325/1425 | BOE's Lombardelli on Monetary Policy Strategy |