FOREX: FX Wrap - USD Rebounds

The BBDXY had an Asian range of 1221.87 - 1229.02. With risk turning around on Trump’s U-turn on Powell and China, as well as Tesla soaring on Elon Musk saying he would be pulling back significantly from DOGE, the USD has had a decent bounce. Is this move sustainable ? Should risk continue to rally we could see some relief from short-term oversold levels but the market will see a decent bounce as an opportunity to once again fade. Bloomberg reports Emmanuel Macron is exploring the possibility of dissolving parliament and holding snap elections as soon as this fall.

- EUR/USD - Asian range 1.1308 - 1.1429, has given back all of Mondays gains and more. The EUR comes off from levels that are overbought, it's been a huge move when you consider it was trading sub 1.0400 the beginning of March. The consensus trade is now to be short USD, a short term rally would be healthy. Demand should remerge on dips back to 1.1100.

- GBP/USD - Asian range 1.3234 - 1.3338, like the EUR Asia looked to be stopping out weaker hands. Dips should be supported, first around 1.3200 then the big support towards 1.3000.

- USD/JPY - Asian range 141.49 - 143.22, large gap higher in the Asian open in what looked to be stops being executed as risk rallied. Supply returned above 143.00 and we have drifted lower for the session from then onwards. USD/JPY’s fate is tied to whether risk is able to hold onto these gains and begin a sustained rally or if this is just another bounce to be faded.

- AUD/USD - Asian Range 0.6349 - 0.6405, The initial leg higher in risk saw the AUD move lower as the USD got bought. Decent buyers emerged around 0.6350 and the AUD has moved back towards 0.6400 going into London.

- USD/CNH - Asian range 7.2922 - 7.3156, the USD/CNY fix printed at 7.2116. USD/CNH continues to trade sideways and find support towards 7.2800.

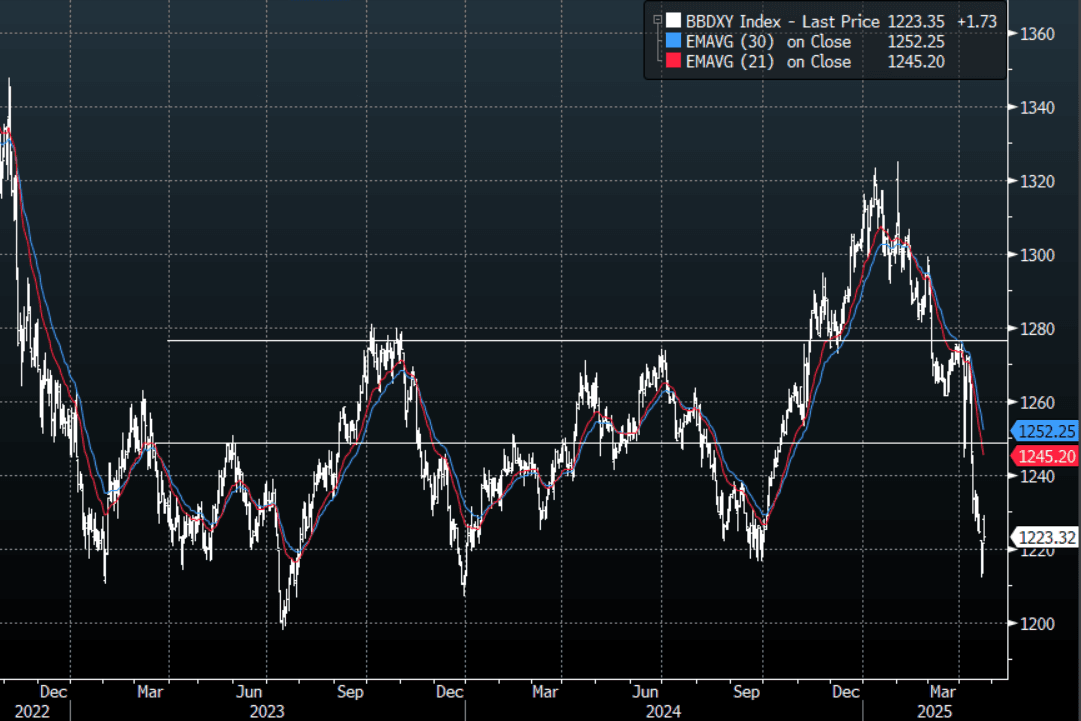

- Cross asset : SPX +1.58%, Gold 3340, US 10yr 4.35%, BBDXY 1223, Crude oil 64.22.

- Data/Events : US S&P Global Services & Manufacturing PMI, FRA PMI’s, GER PMI’s, EC PMI’s, EC Trade Balance

Fig 1 : BBDXY Daily Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: US$ Off Lows, US PMIs Coming Up

Given higher US yields, G10 currencies are struggling to make gains against the US dollar (BBDXY USD index slightly higher). The yen has underperformed through the day following disappointing PMI data and weak government ratings. BoJ comments reiterating the need for “stable” FX moves and likely rate normalisation going ahead failed to strengthen the yen.

- USDJPY trended higher through today and is up 0.3% to 149.73, around where it has stabilised, following a high of 149.95. Initial resistance is at 150.15, 19 March high, while support is at 148.18, 20 March low.

- AUDUSD has given up most of its earlier gains to be up 0.1% to around 0.6279. It reached 0.6295 and then trended lower on Hang Seng/ASX softness. Copper and iron ore have been slightly stronger up 0.2% and around $101.50/t respectively. AUDJPY is off its high of 94.26 but still up 0.4% to 94.01.

- NZDUSD reached a peak of 0.5750 but then trended down and is currently 0.2% lower at 0.5724. This has boosted AUDNZD 0.3% to 1.0970, close to today’s high.

- EURUSD is little changed at 1.0823 and GBPUSD at 1.2918, it has struggled to break above 1.30. This has left EURGBP slightly higher at around 0.8378.

- Equities are mixed with the Hang Seng down 0.1%, Topix -0.4% but ASX up 0.1%, CSI 300 +0.2% and S&P e-mini +0.6%. Oil prices are slightly lower with WTI -0.3% to $68.04/bbl.

- Later the Fed’s Bostic and Barr appear and preliminary March S&P Global PMIs and February Chicago activity index are released. European March PMIs are also out.

GOLD: Gold Trending Lower on Profit Taking.

* Last week gold finally broke through US$3,000 for the first time in what for many analysts was earlier than expected.

* Gold began Monday at $3,022.15 and has trended lower for most of the session to be at $3,017.72.

* Up almost 16% year to date, gold has been one asset class that has benefitted from the factors driving global markets namely tariff risks, Federal Reserve policy uncertainty and inflation.

* Globally analysts have been adjusting their forecasts for gold for 2025 with some now predicting US$3,500 before year end.

AUSSIE BONDS: Subdued Session Ahead of Federal Budget Tomorrow & CPI (Wed)

ACGBs (YM flat & XM -1.0) are little changed on a data light session.

- Cash US tsys are 2-3bps cheaper across benchmarks in today's Asia-Pac session after Friday's uneventful end to the trading week. Monday's US focus will be on S&P flash PMIs alongside more Fed speakers including Atlanta Fed Bostic on Bbg TV and Fed Gov Barr on small business lending late in the afternoon.

- Cash ACGBs are 1bp richer to 1bp cheaper with the 3/10 curve steeper and the AU-US 10-year yield differential at +13bps.

- The swap curve has bull-steepened, with rates flat to 2bps lower.

- The bills strip is flat to +3, with a flattening bias.

- RBA-dated OIS pricing is flat to 2bps softer across meetings today. A 25bp rate cut in April is given a 4% probability, with a cumulative 68bps of easing priced by year-end (based on an effective cash rate of 4.09%).

- Tomorrow will see the Federal Budget, with an election likely to be called soon after. It is expected to show deficits across the forecast horizon with additional expenditure likely in an attempt to win votes.

- The key data item for the week is Wednesday's February CPI data.