AUSTRALIA: Q1 NZ CPI Data Suggest Australian Services Inflation Moderated

Q1 Australian CPI data is released on Wednesday April 30 and will be an important input into the May 20 RBA decision, where a rate cut is largely expected. There are high correlations between NZ and Australian CPI data and given NZ’s Q1 has already been released, there are possibly trends that we can ascertain. Australia may see a pickup in goods inflation, while sticky services may moderate.

- NZ headline, non-tradeables & tradeables printed higher than expected but both headline and core were in the RBNZ’s 1-3% target band at 2.5% y/y and 2.9% y/y respectively.

- With government electricity rebates continuing to reduce Australia’s headline inflation, there is little to be gained by looking at NZ’s trends here.

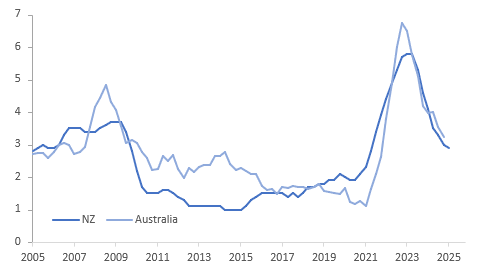

- There is a 3-year rolling correlation of around 90% between Australia/NZ underlying inflation measures. The RBNZ’s sector factor model estimate of core moderated 0.1pp to 2.9% in Q1. In addition, Australia’s monthly data are pointing to a moderation in quarterly trimmed mean inflation in Q1.

Australia vs NZ core CPI y/y%

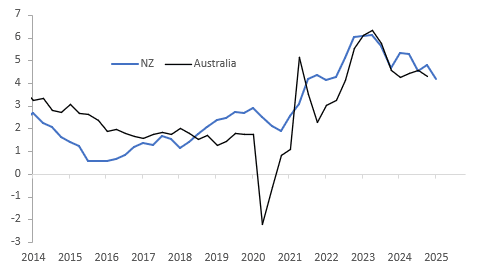

- Domestically-driven services inflation has been monitored closely for some time and the Australia/NZ correlation is also close to 90%. NZ services inflation moderated 0.6pp to 4.2% y/y and non-tradeables 0.5pp to 4.0% y/y, which is good news for Australia.

- Australia is likely to see a pickup in goods inflation, which is significantly determined by global factors. It rose to 1.4% y/y in NZ from 0.6% signalling that its disinflationary pressure is likely over, consistent with Australia’s monthly goods inflation data.

Australia vs NZ services y/y%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Subdued Session To Start Week, No Shocks From BoJ Ueda & Uchida

JGB futures are weaker and at Tokyo session lows, -15 compared to the settlement levels.

- BoJ Governor Ueda said on Monday the central bank will continue to raise interest rates if its underlying inflation target is likely to be achieved, despite potential losses on its government bond holdings. "We have said that we will continue adjusting the degree of monetary easing if underlying inflation is likely to approach 2%," Ueda said in parliament when asked about the impact of losses on the BoJ's huge holdings of Japanese government bonds. (per RTRS)

- “Japan has not yet beaten deflation despite years of persistently rising consumer prices and the largest round of annual wage increases in three decades, the country’s finance minister has warned.” (per FT)

- Cash US tsys are 2-3bps cheaper across benchmarks in today's Asia-Pac session after Friday's uneventful end to the trading week. The US Treasury will bring a combined supply of $183bn of new two-, five- and seven-year notes.

- Cash JGBs are flat to 2bps cheaper across benchmarks. The benchmark 10-year yield is 1.6bps higher at 1.54% versus the cycle high of 1.584%.

- Swap rates are 1-2bps higher, with swap spreads mostly wider.

- Tomorrow, the local calendar will see the BoJ Minutes for January MPM and Department Sales data alongside an auction for Enhanced-Liquidity 5-15.5-years.

FOREX: US$ Off Lows, US PMIs Coming Up

Given higher US yields, G10 currencies are struggling to make gains against the US dollar (BBDXY USD index slightly higher). The yen has underperformed through the day following disappointing PMI data and weak government ratings. BoJ comments reiterating the need for “stable” FX moves and likely rate normalisation going ahead failed to strengthen the yen.

- USDJPY trended higher through today and is up 0.3% to 149.73, around where it has stabilised, following a high of 149.95. Initial resistance is at 150.15, 19 March high, while support is at 148.18, 20 March low.

- AUDUSD has given up most of its earlier gains to be up 0.1% to around 0.6279. It reached 0.6295 and then trended lower on Hang Seng/ASX softness. Copper and iron ore have been slightly stronger up 0.2% and around $101.50/t respectively. AUDJPY is off its high of 94.26 but still up 0.4% to 94.01.

- NZDUSD reached a peak of 0.5750 but then trended down and is currently 0.2% lower at 0.5724. This has boosted AUDNZD 0.3% to 1.0970, close to today’s high.

- EURUSD is little changed at 1.0823 and GBPUSD at 1.2918, it has struggled to break above 1.30. This has left EURGBP slightly higher at around 0.8378.

- Equities are mixed with the Hang Seng down 0.1%, Topix -0.4% but ASX up 0.1%, CSI 300 +0.2% and S&P e-mini +0.6%. Oil prices are slightly lower with WTI -0.3% to $68.04/bbl.

- Later the Fed’s Bostic and Barr appear and preliminary March S&P Global PMIs and February Chicago activity index are released. European March PMIs are also out.

GOLD: Gold Trending Lower on Profit Taking.

* Last week gold finally broke through US$3,000 for the first time in what for many analysts was earlier than expected.

* Gold began Monday at $3,022.15 and has trended lower for most of the session to be at $3,017.72.

* Up almost 16% year to date, gold has been one asset class that has benefitted from the factors driving global markets namely tariff risks, Federal Reserve policy uncertainty and inflation.

* Globally analysts have been adjusting their forecasts for gold for 2025 with some now predicting US$3,500 before year end.