AUSSIE BONDS: Subdued Start To Data-Light Session, 3/10 YC Flattest Since March

ACGBs (YM -0.5 & XM flat) are little changed after cash US tsys finished near flat.

- Initial jobless claims 'surprised' higher at 236k (sa, cons 220k) in the week to Dec 6, a consensus reading that had looked for surprisingly little rebound considering it followed the 3+ year low of 219k in the week to Nov 29 in what had looked likely down to difficulty in adjusting around the Thanksgiving holiday. Continuing claims, meanwhile, were also lower than expected at 1838k (sa, cons 1938k) in the week to Nov 29 after a marginally downward revised 1937k (initial 1939k).

- Cash ACGBs are flat with the AU-US 10-year yield differential at +56bps.

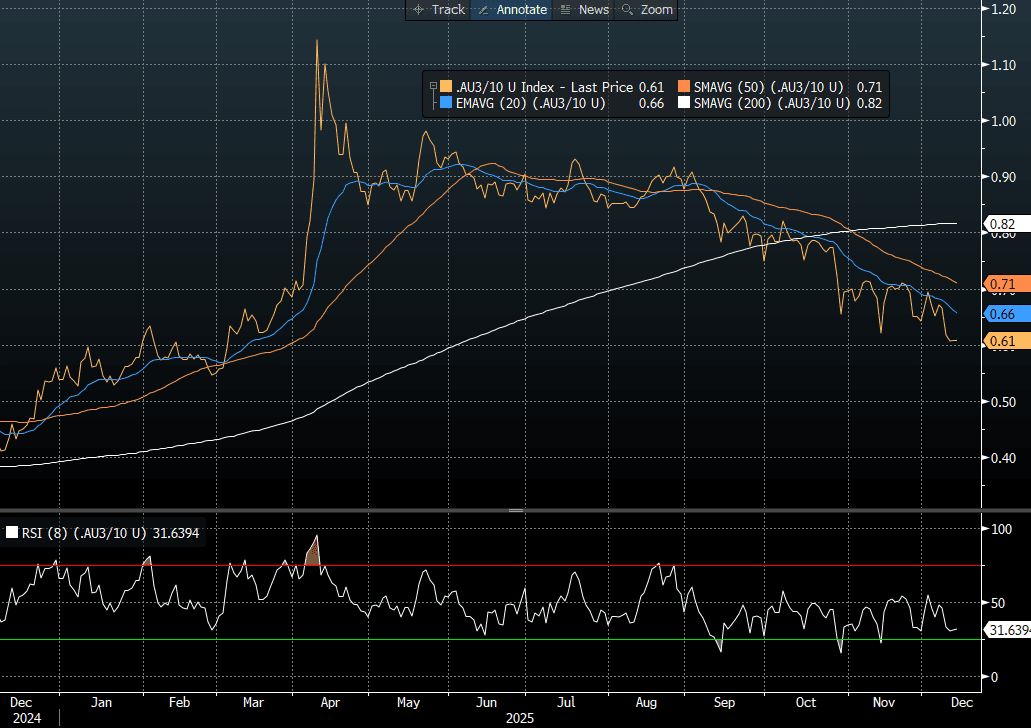

- The 3/10 curve sits at its flattest since March. The recent curve flattening has occurred alongside a steady rise in market forward expectations for the RBA cash rate. A simple regression of the 3s/10s curve against the 1Y3M rate over the past three years suggests the current curve is roughly 20bps too steep relative to its fair value (see chart).

- The bills strip has bear-flattened, with pricing -3 to flat.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 29% for February to 104% by June and 168% by December 2026.

- Today, the local calendar will be empty.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Modestly Stronger, Jobs Data Tomorrow

ACGBs (YM +1.0 & XM +2.0) are modestly stronger after US tsy futures closed firmer.

- Looking ahead, Wednesday’s US data is limited to MBA Mortgage Applications and $42bn 10Y Note. Focus on multiple Fed speakers through the session: Williams, Paulson, Waller, Bostic, Miran and Collins.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +25bps.

- The bills strip is little changed across contracts.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 9% probability, with a cumulative 16bps of easing priced by mid-2026.

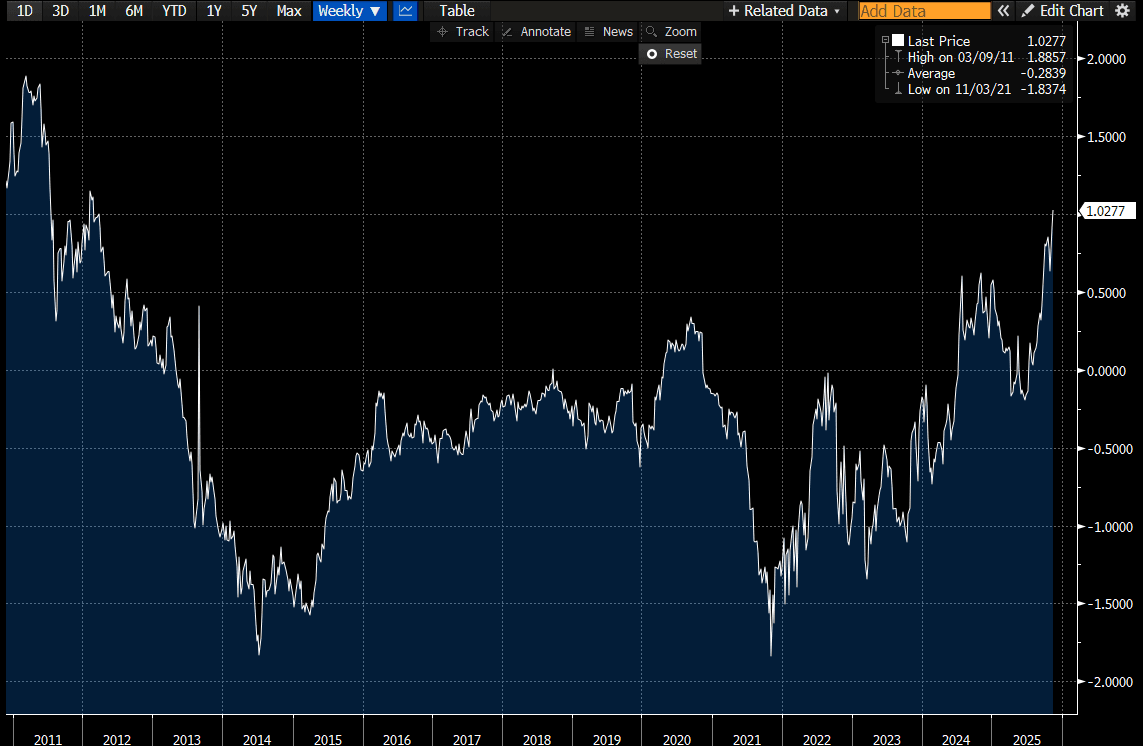

- Interestingly, AU-NZ 1-year forward 3-month swap (1Y3M) spread at 103bps is now at its highest level since 2012.

- Today, the local calendar will see Home Loan data alongside RBA Jones' Fireside Chat.

- However, the highlight of this week's AUS calendar will be Thursday's October jobs data. The unemployment rate rose 0.2pp to 4.5% in September.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035bond today and A$800mn of the 1.75% 21 November 2032 bond on Friday.

GOLD: Corrective Phase Over, US Data Release Schedule Likely Next Week

Gold increased back above $4140 following concerning US ADP data but the move wasn’t held with it then falling to $4097.25. It has recovered somewhat to $4126.85 to be up 0.3% and 3.1% in November finding support from the weaker US dollar (BBDXY -0.1%). The market has around a 67% chance of a December Fed cut but gold’s response to the upcoming end of the US government shutdown signals that it thinks the delayed data will drive increased easing expectations when it is released.

- Advance ADP data suggested private sector job losses in the four weeks to 25 October but the providers noted the data is preliminary and could be revised.

- Our US analysts believe that the post-shutdown data schedule should be published next week but there is a risk that October CPI won’t be released. See their FAQ here.

- Bullion reached $4149.0 on Tuesday, remaining below initial resistance at $4161.4, 22 October high. The recent recovery in gold prices marks the end of the corrective phase which allowed the overbought condition to unwind. The bull trigger is at $4381.5. A decline below the 50-day EMA at $3890.0 would signal scope for a deeper retracement.

- Bloomberg reported gold ETF outflows in the 3 weeks to November 7 following 8 weeks of inflows.

- Silver rose to $51.252, remaining below initial resistance at $52.374, following the ADP data and then fell to $50.290. It then recovered to $51.221 to be up 1.4% on the day and 5.2% on the month. The trend remains bullish with the metal continuing to trade above the 50-day EMA at $46.484.

AUSSIE SWAPS: AU-NZ 1Y3M Spread Highest Since 2012

AU–NZ 1-year forward 3-month swap (1Y3M) spread at 103bps is now at its highest level since 2012.

- The 1Y3M differential is a proxy for the expected relative policy path over the next 12 months.

Bloomberg Finance LP