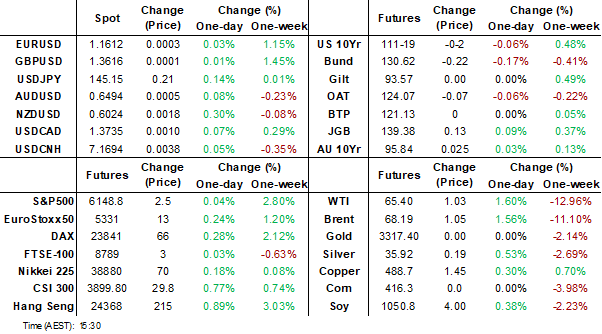

MNI EUROPEAN MARKETS ANALYSIS: Positive Sentiment Continues

- Equity markets delivered a second day of gains with China's major bourses leading the way.

- The European Union advises that it intends to to impose retaliatory tariffs on the US.

- Chairman Powell of the Fed still sees the USD as the Global Reserve Currency.

- BOJ Members remain hawkish and suggest more cuts to come.

- The day ahead sees Spanish GDP, German Consumer Confidence, US Home Sales, Durable Goods and GDP.

MARKETS

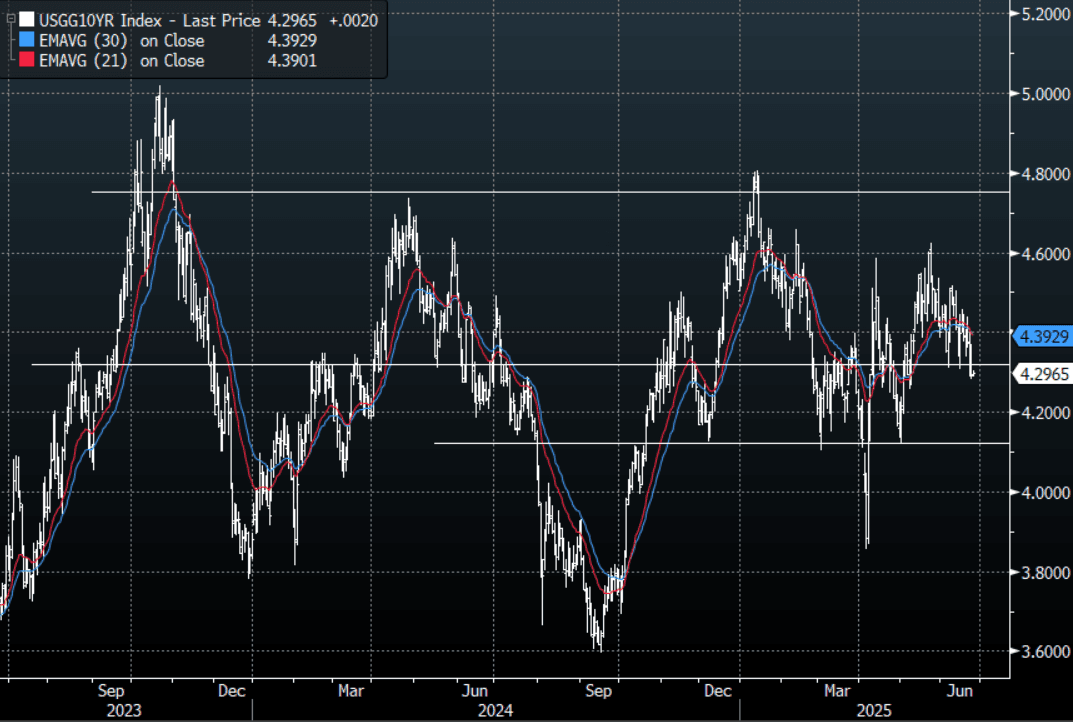

US TSYS: Asia Wrap - Front End Yield Extends Lower

The TYU5 range has been 111-17+ to 111.22 during the Asia-Pacific session. It last changed hands at 110-19+, down 0-01+ from the previous close.

- The US 2-year yield has moved lower trading around 3.79%, down 0.03 from its close.

- The US 10-year yield is relatively unchanged around 4.30%.

- This has seen the yield curve steepen: 2s10s +3.61 at 50.143

- (Bloomberg) - US bond investors are too complacent about inflation and the Fed’s fears it will reaccelerate. Expectations for the decline in yields to accelerate look optimistic given that President Trump’s tax-and-spending bill may boost supply. Inflation is also likely to accelerate ahead of the next Fed meeting. Both this week’s core PCE print for May and the June Core CPI data due in the middle of next month are forecast to show higher readings.

- FED - FOMC sitting member Schmid, Kansas Fed, affirmed Chair Powell’s comments to the Senate that it is best to watch and wait to assess the impact of tariffs and policy on the economy given its resilience, especially the labour market, rather than rushing to ease monetary policy.

- The 10-year yield was again seriously testing the 4.30% support overnight, a sustained move back below here is likely to see the move pick up momentum. 10-year yields would need to get back above 4.45/4.50% again to alleviate this downward pressure.

Data/Events: MBA Mortgage Applications, Building Permits, New Home Sales

Fig 1: US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Holding Gains Despite Hawkish BoJ Speak, Tokyo CPI On Friday

JGB futures are stronger, +14 compared to settlement levels, hovering just below session bests.

- A few Bank of Japan board members supported steadily reducing the Bank’s JGB holdings, though concerns over moving too quickly were also raised, according to the summary of opinions from the June 16-17 policy meeting released Wednesday.

- One member noted that excess reserves remained abundant, making it appropriate for the Bank to “proceed steadily with the reduction of its purchase amount of JGBs, and thereby normalise its balance sheet.”

- BoJ board member Naoki Tamura signalled a more hawkish stance, suggesting the Bank’s 2% inflation target could be achieved earlier than expected and calling for a steady normalisation of monetary policy and the BoJ’s balance sheet. Tamura said he does not view the 0.5% policy rate as a ceiling, citing both rising inflation and changes in bank lending rates compared to the previous rate-hike cycle.

- Cash US tsys are modestly mixed in today's Asia-Pac session.

- Cash JGBs are 1-3bps richer across benchmarks, with the 20-year leading.

- Swap rates are 1-3bps lower. Swap spreads are mixed.

- Tomorrow, the local calendar will see Weekly International Investment Flow data alongside 2-year supply. Tokyo CPI is due on Friday.

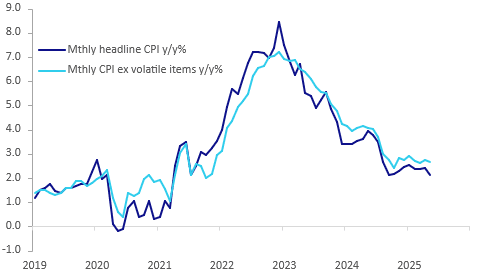

AUSSIE BONDS: Moderately Richer, July Rate Cut At 95% After CPI Data

ACGBs (YM +2.0 & XM +2.5) are trading modestly stronger.

- May headline CPI inflation was flat on the month, driving a 0.3pp moderation in the annual rate to 2.1% driven by a broad-based easing across major components. The trimmed mean moderated to 2.4% y/y from 2.8%, the lowest since November 2021. However, CPI ex volatile items and holiday travel was only down 0.1pp to 2.7% y/y. The RBA decision is on July 8 and this data is likely to increase expectations of another rate cut but the Board prefers the quarterly CPI (due July 30) and updated staff forecasts are not provided until August.

- Cash US tsys are modestly mixed in today's Asia-Pac session after yesterday's modest gains.

- Cash ACGBs are 2bps richer with the AU-US 10-year yield differential at -16bps. At -16bps, the differential is positioned in the bottom half of the +/- 30bps range that has held since November 2022.

- The bills strip has bull-steepened, with pricing +1 to +7.

- RBA-dated OIS pricing is softer across meetings after today’s data. A 25bp rate cut in July is given a 95% probability (84% pre-data), with a cumulative 83bps of easing (78bps pre-data) priced by year-end.

- Tomorrow, the local calendar will see Job Vacancies data.

AUSTRALIA DATA: Trimmed Mean Inflation Lowest Since 2021 Raising Cut Hopes

May headline CPI inflation was flat on the month, seasonally adjusted, driving a 0.3pp moderation in the annual rate to 2.1% driven by a broad-based easing across major components. The trimmed mean moderated to 2.4% y/y from 2.8%, the lowest since November 2021. However, CPI ex volatile items and holiday travel was only down 0.1pp to 2.7% y/y. The RBA decision is on July 8 and this data is likely to increase expectations of another rate cut but the Board prefers the quarterly CPI (due July 30) and updated staff forecasts are not provided until August.

Australia CPI y/y%

- Headline continued to be impacted by a number of volatile factors with automotive fuel down 2.9% m/m & 10% y/y due to global oil prices, which are likely to be higher in June given events in the Middle East. Also electricity prices fell 5.9% y/y although up from -6.5% y/y but would have been up 2% y/y without state and federal rebates. Fruit & veg eased to 2.8% y/y from 6.1%. Holiday travel & accommodation moderated sharply to 0.6% y/y from 5.3%.

- More stable components also saw a moderation with insurance at 3.9% y/y after 7.6% and rents 4.5% y/y down from 5.0%. New dwellings only rose 0.8% y/y, the slowest rate since April 2021 as discounts are offered to encourage new business.

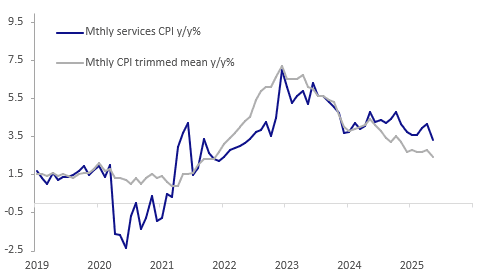

- Domestically-driven measures saw a moderation with services inflation at 3.3% y/y from 4.1%, the lowest since May 2022, and non-tradeables 3.2% from 3.6%, softest since the more recent December 2024.

- Goods inflation was stable in May at 1.0% y/y while tradeables fell to 0% y/y from 0.3% due to fuel.

Australia CPI services vs trimmed mean y/y%

BONDS: NZGBS: Closed On A Strong Note, Tracking US Tsys & ACGBs

NZGBs closed on a strong note, with benchmark yields 4-5bps lower. NZ-US and NZ-AU 10-year yield differentials were little changed.

- Cash US tsys are modestly mixed in today's Asia-Pac session after yesterday's modest gains. Yesterday, FOMC sitting member Schmid, Kansas Fed, affirmed Chair Powell's comments to the Senate that it is best to watch and wait to assess the impact of tariffs and policy on the economy, given its resilience, especially the labour market, rather than rushing to ease monetary policy. Today’s US calendar: MBA Mortgage Applications, Building Permits, New Home Sales.

- (Reuters) -New Zealand on Wednesday released a draft 30-year national infrastructure plan, which highlighted a need for the country to invest more in hospitals and electricity production and to prepare to spend more on responding to national disasters.

- Swap rates also closed 4-5bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed flat to 6bps softer across meetings. 4bps of easing is priced for July, with a cumulative 33bps by November 2025.

- Tomorrow, the local calendar will be empty apart from the NZ Treasury's planned sale of NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

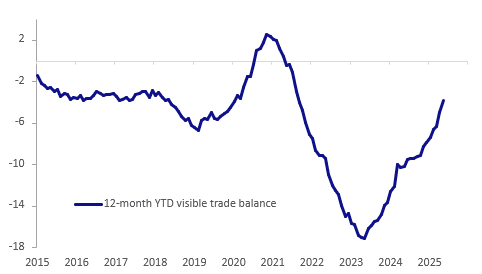

NEW ZEALAND: Trade Surplus Continues, Consumption Imports Weak

NZ posted its fourth consecutive monthly merchandise trade surplus in May with shipments to the US remaining elevated. The surplus was $1.23bn slightly narrower than April’s $1.29bn with the YTD deficit narrowing $1.18bn to $3.79bn. Both exports and imports were down on the month. The primary sector has seen solid growth with higher prices and strong exports of dairy and fruit.

NZ trade balance YTD $bn 12-mth YTD

Source: MNI - Market News/LSEG

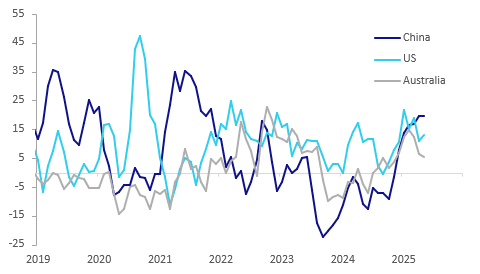

- Goods exports fell 5.5% m/m seasonally adjusted but were still up 9.7% y/y with shipments of dairy products up 18% y/y, fruit +25% y/y and meat +11% y/y. Prices for dairy and meat are higher but volumes of some products are lower.

- Exports to China, NZ’s largest export destination rose 13.4% y/y in May. The level of exports to the US remains elevated but is now down 2.2% y/y but the 3-month average, to smooth the volatility, is up 12.9% y/y. Shipments have risen sharply as NZ frontloads ahead of US tariff deadlines, which have been shifting. They rose 10.1% y/y to Australia.

- Imports were down 1.7% m/m and 7.2% y/y. The weakness is due to volatile components such as aircraft and petroleum which was impacted by lower global oil prices. However vehicles are down 20% y/y, signalling weak demand (consumer goods imports -3.4% y/y), but electrical equipment rose 5% y/y suggesting increased investment.

NZ goods exports y/y% 3-mth ma

Source: MNI - Market News/LSEG

FOREX: Asia FX Wrap - BBDXY Finds Some Demand Towards 1200, For Now

The BBDXY has had a range of 1200.25 - 1202.09 in the Asia-Pac session, it is currently trading around 1202. The BBDXY has found some demand back towards the 1200 area in a very quiet Asian session, +0.04%%. The BBDXY extended its move lower again overnight, the price action was very revealing and points to a market that is very quick to reinstate USD shorts with conviction pretty high for a move lower. “The BOE’s Andrew Bailey and Dave Ramsden warned that the labor market is cooling and pay pressures are easing in one of the strongest signs yet that the central bank is on course to cut rates again this summer”(BBG).”Goldman said the dollar will extend its worst start to a year as foreign investors boost FX hedges.”(BBG)

- EUR/USD - Asian range 1.1605 - 1.1631, Asia is currently trading 1.1615. The EUR remains well supported on dips, potential USD demand today with corporate month-end. While the USD remains on the back foot the EUR will continue to be supported first support back towards 1.1500.

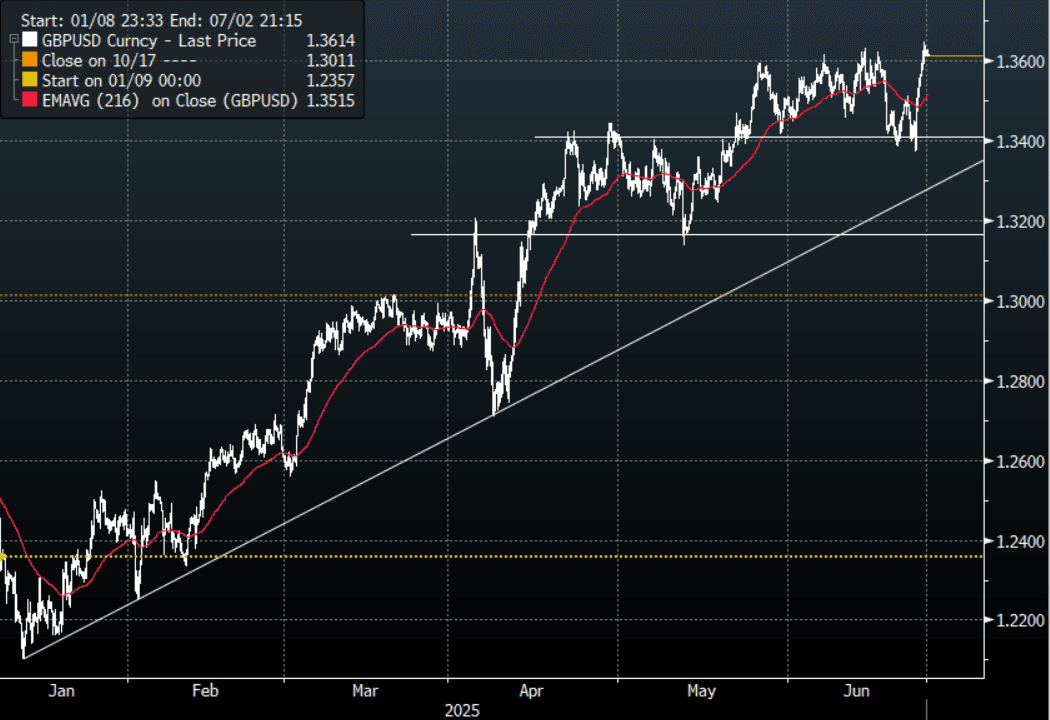

- GBP/USD - Asian range 1.3611 - 1.3629, Asia is currently dealing around 1.3615. The GBP again found solid demand around its 1.3400 support and has made new highs above 1.3600 looking for the momentum to carry it through its weekly pivot.

- USD/CNH - Asian range 7.1604 - 7.1711, the USD/CNY fix printed 7.1668. Asia is currently dealing around 7.1680. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.01%, Gold $3327, US 10-Year 4.297%, BBDXY 1202, Crude oil $65.20

- Data/Events : Spain GDP & PPI, France Consumer Confidence

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

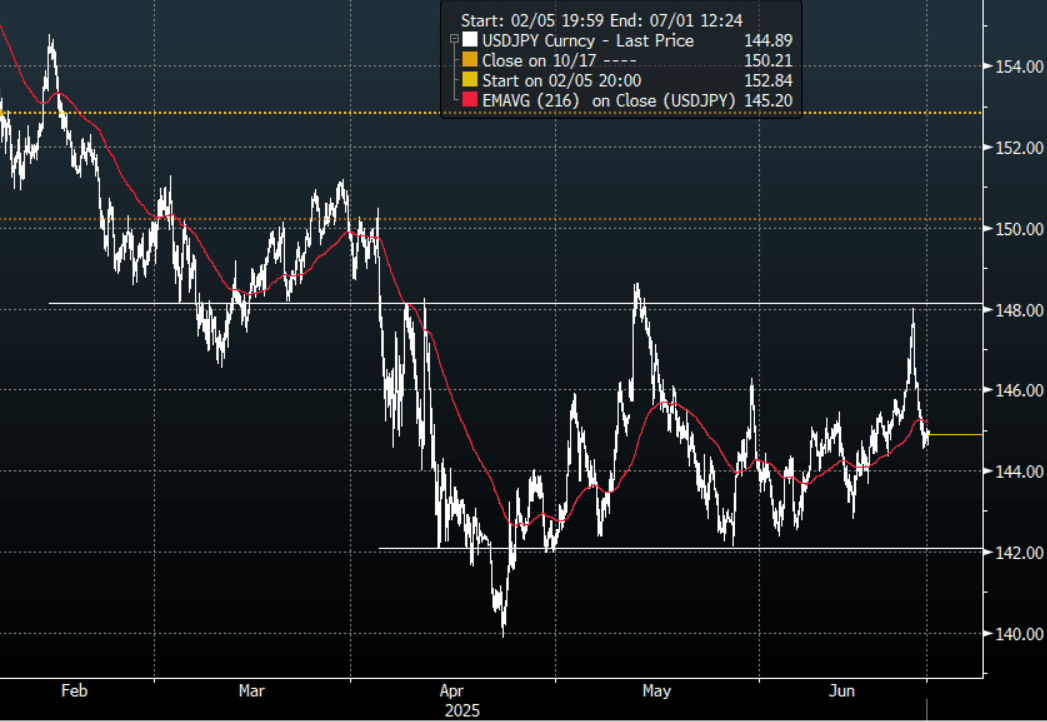

JPY: Asia Wrap - USD/JPY Finds Support Back Towards 144.50 As Oil Stabilises

The Asia-Pac USD/JPY range has been 144.61 - 145.04, Asia is currently trading around 144.90. USD/JPY found some demand back towards the 144.50 area when market tested lower on Hawkish comments from BOJ board member Naoki Tamura. The capitulation in oil also seems to have seen its momentum stall for now. The price action suggests any bounces will be met with sellers, corporate month-end USD demand might give them that opportunity.

- (Bloomberg) - “BoJ board member Naoki Tamura signaled a more hawkish stance on Wednesday, suggesting the Bank's 2% inflation target could be achieved earlier than expected and calling for a steady normalisation of monetary policy and the BoJ's balance sheet.”

- “A few Bank of Japan board members supported steadily reducing the Bank's JGB holdings, though concerns over moving too quickly were also raised, according to the summary of opinions from the June 16-17 policy meeting released Wednesday.”(BBG)

- An ugly daily shadow points to a potential top being in place now and highlights how quick the market is to return to selling USD’s, we are testing the support this morning around 144.50 where some demand was seen overnight.

- Price now back in its wider 142.00 - 148.00 range, I am not sure that the brief spike higher would have seen positioning altered too much so the long JPY trade remains alive and well.

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.50($1.88b).Upcoming Close Strikes : 142.00($1.32b June 26), 143.00($1.41b June 26)

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

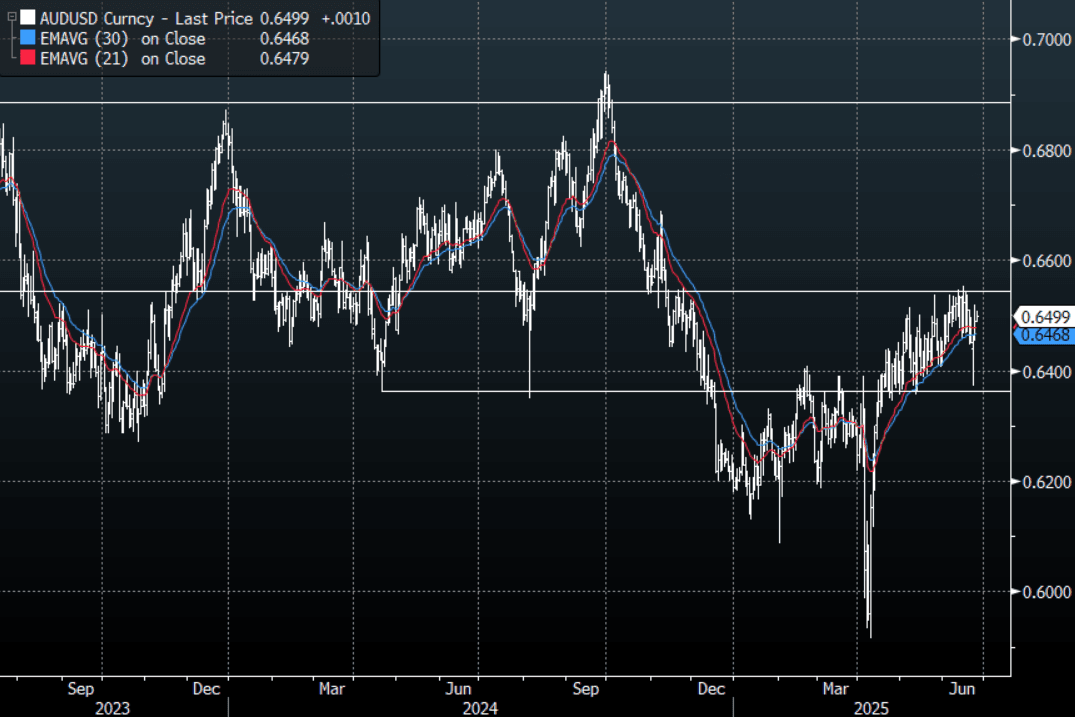

AUD: Asia Wrap - CPI Print Finds Bids Sub 0.6500

The AUD/USD has had a range of 0.6489 - 0.6508 in the Asia- Pac session, it is currently trading around 0.6500, +0.15%. The AUD attempted to move lower on the CPI print but found bids sub 0.6500 and clawed back all its losses. A quiet session sees AUD/USD continue to trade with an underlying bid tone. We are approaching the corporate month-end and this normally results in a demand for USD's so perhaps better levels could be seen for AUD buyers.

- AUSTRALIA DATA: Trimmed Mean Inflation Lowest Since 2021 Raising Cut Hopes. May headline CPI inflation was flat on the month, seasonally adjusted, driving a 0.3pp moderation in the annual rate to 2.1% driven by a broad-based easing across major components. The trimmed mean moderated to 2.4% y/y from 2.8%, the lowest since November 2021. The RBA decision is on July 8 and this data is likely to increase expectations of another rate cut but the Board prefers the quarterly CPI (due July 30) and updated staff forecasts are not provided until August.

- The AUD/USD bounced hard off its support and is now back to potentially testing the top end of its range as the USD comes back under pressure.

- We are approaching the corporate month-end and this normally results in a demand for USD’s so perhaps better levels could be seen over the course of the next day or so for those wanting to express a long AUD position.

- Price remains in the wider 0.6350 - 0.6550 range for now. The AUD needs a sustained break above 0.6550 to potentially start building towards a move higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6500(AUD2.11b June 26), 0.6425(AUD776m June 30).

- AUD/JPY - Today's range 93.98 - 94.28, it is trading currently around 94.20. Choppy price action as the pair establishes a range between 92.00 - 96.00. Should risk build on this move, focus could turn back to the 96.00 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

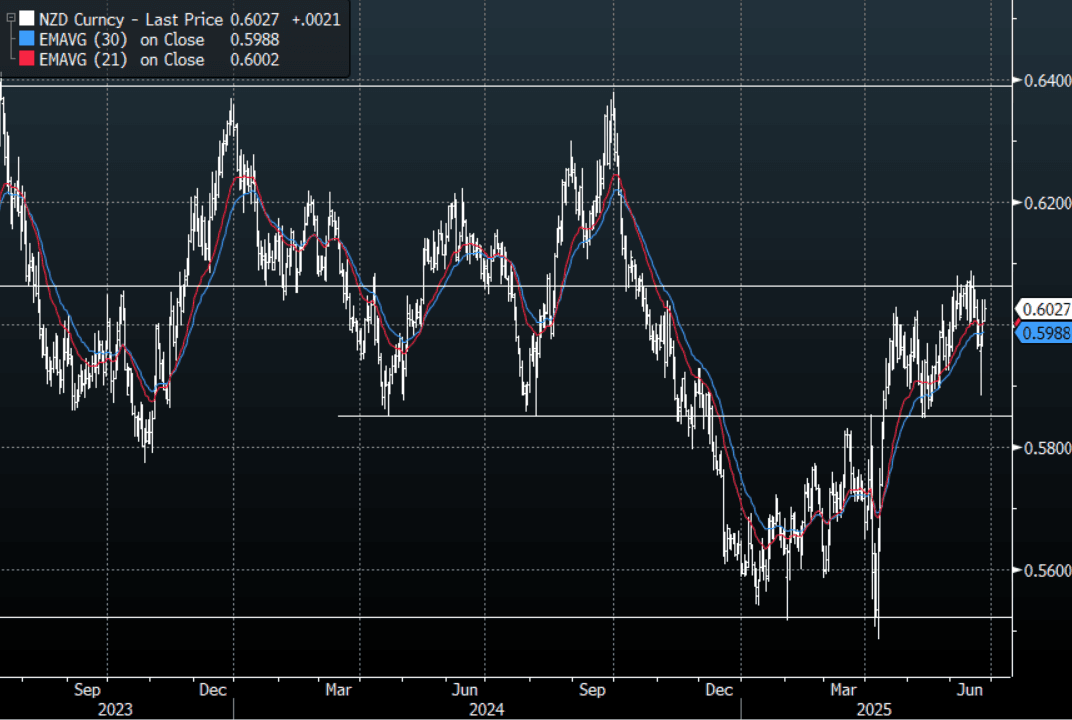

NZD: Asia Wrap - NZD/USD Builds On Momentum Above 0.6000

The NZD/USD had a range of 0.6004 - 0.6040 in the Asia-Pac session, going into the London open trading around 0.6030, +040%. The NZD has drifted higher all through the Asian session, taking us back to the overnight highs. We are approaching the corporate month-end and this normally results in a demand for USD's this could provide some very short-term headwinds.

- NZ's trade surplus narrowed to NZ$1.235b in May from a revised +NZ$1.285b in April. 12 months ytd trade deficit narrowed to NZ$3.790b from a revised -NZ$4.965b in April.

- “Goldman said the dollar will extend its worst start to a year as foreign investors boost FX hedges.”(BBG)

- A huge bounce from sub 0.5900 and the NZD is now trying to establish a foothold above 0.6000, corporate month- end could provide some headwinds but for now dips look likely to be well supported.

- Technically while the support around 0.5850 holds in NZD/USD it is still in an uptrend. This area held perfectly and should risk continue to move higher then the focus will turn once again back to the 0.6050/0.6100 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6040(NZD373m June 26)

- AUD/NZD range for the session has been 1.0770 - 1.0809, currently trading 1.0780. The cross seems to have failed in its attempt to push higher above 1.0800, a sustained break back below sub 1.0750 would see the downtrend reengaged.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Most Major Bourses Post Decent Gains

Following on from yesterday's positive day, most major bourses moved higher today led by Taiwan. In Hong Kong EV stocks got a boost from news that the Ministry of Commerce will require local governments to implement trade in policies with subsidies for EVs. In Korea a strong rally from Korea Electric Power on Middle East truce wasn't enough to keep the KOSPI from dipping marginally.

- In China the Hang Seng lead the way rising +0.77% whilst the CSI 300 was up half of that at +0.35%. The Shanghai Composite is up +0.28% and +1.2% in the last five days of trading whilst the Shenzhen Comp rose +0.51%

- In Taiwan the TAIEX was one of the strongest of the major markets rising +0.95%.

- The KOSPI was one of the fallers today down -0.16% in what appeared to be little more than profit taking with limited news and the index being up over 4% in the last week.

- The FTSE Malay KLCI rose +0.42% and the Jakarta Composite went the other way falling -0.50%.

- In Singapore the FTSE Straits Times is up +0.47% and the PSEi in the Philippines is up +0.47%

- The NIFTY 50 has had a strong start to the day rising +0.60% following on from yesterday's modest gains of +0.29%

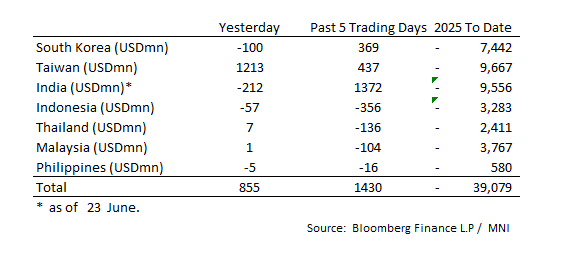

ASIA STOCKS: Huge inflow for Taiwan

Taiwan stemmed three days of losses with a substantial inflow.

- South Korea: Recorded outflows of -$100m yesterday, bringing the 5-day total to +$369m. 2025 to date flows are -$7,442. The 5-day average is +$74m, the 20-day average is +$201m and the 100-day average of -$75m.

- Taiwan: Had inflows of +$1,213m yesterday, with total inflows of +$437 m over the past 5 days. YTD flows are negative at -$9,667. The 5-day average is +$87m, the 20-day average of +$18m and the 100-day average of -$75m.

- India: Had outflows of -$212m as of the 23rd, with total inflows of +$1,372m over the prior 5 days. YTD flows are negative -$9,556m. The 5-day average is +$274m, the 20-day average of +$42m and the 100-day average of -$42m.

- Indonesia: Had outflows of -$57 yesterday, with total outflows of -$356m over the prior five days. YTD flows are negative -$3,283m. The 5-day average is -$71m, the 20-day average -$20m and the 100-day average -$31m.

- Thailand: Recorded inflows of +$7m yesterday, with outflows totaling -$136m over the past 5 days. YTD flows are negative at -$2,411m. The 5-day average is -$27m, the 20-day average of -$40m and the 100-day average of -$23m.

- Malaysia: Recorded inflows of +$1m yesterday, totaling -$104m over the past 5 days. YTD flows are negative at -$3,767m. The 5-day average is -$22m, the 20-day average of -$28m and the 100-day average of -$23m.

- Philippines: Recorded outflows of -$5m yesterday, with net outflows of -$16m over the past 5 days. YTD flows are negative at -$580m. The 5-day average is -$3m, the 20-day average of -$16m the 100-day average of -$5m.

OIL: Crude Higher After US Inventories Fall, Also Monitoring Truce

After falling around 12% over the first two days of the week on a de-escalation of Middle East tensions, oil prices are over a percent higher today. They have stabilised as markets generally monitor the Iran-Israel ceasefire which so far today has held. A reported US crude inventory drawdown has also helped. WTI is up 1.4% to $65.24 after a low of $65.00, while Brent is 1.1% higher at $67.89/bbl, just off the intraday high OF $68.16. The USD index is slightly higher.

- With the abatement of concerns that Middle Eastern oil supplies would be impacted by conflict, fundamentals are back in focus. Bloomberg reported that US crude inventories fell 4.28mn barrels last week after declining over 10mn the previous week, according to people familiar with the API data. The official EIA data is out Wednesday. It reported a 11.5mn drop the previous week.

- Also on the supply front, there are tentative indications that restrictions on Iran could eventually be eased following the ceasefire agreement. Unexpectedly, President Trump openly allowed Iran to continue selling oil to China.

- OPEC also meets virtually on July 6 to decide August’s production target. Another +400kbd increase is likely as the group normalises output after reducing it, targets market share and punishes overproducing members.

- On the demand side, the progress of trade negotiations ahead of the July 9 deadline will also be monitored closely. Increased US trade protectionism rattled crude as it feared energy demand would sink.

- Later Fed Chair Powell continues his testimonies. The Fed’s Goolsbee, ECB’s Donnery and BoE’s Lombardelli speak. US May new home sales/permits print.

GOLD: Bullion Stabilizes After Middle East Truce Drives Stronger Risk Appetite

After falling 1.3% on Tuesday, gold rose to a high of $3335.24/oz today as markets stabilised following an easing in tensions in the Middle East which reduced safe-haven flows. They are now monitoring how well Israel and Iran are sticking to the ceasefire. It has been quiet on this front so far today. Bullion has come off its intraday high to be up 0.1% to $3327.2. The USD and US yields are slightly higher from early in the session.

- Gold’s bullish theme is intact and this week’s decline is seen as corrective. Moving average studies are also still in a bull mode signalling a dominant uptrend. The yellow metal will monitor US data closely for signs of negative economic impacts from import duties and any change in the Fed’s “on hold” tone. Initial resistance is at $3451.3, 16 June high, while support is at $3286.2, 50-day EMA.

- Silver has range traded reaching a high of $35.99 and then a low of $35.90. It is currently moderately higher at $35.93. Initial support is at $35.55 and resistance at $37.32. Any sell off is still seen as corrective.

- Equities are mixed with the S&P e-mini flat, Topix down 0.2% but Hang Seng up 0.8%. Oil prices are higher with WTI +1.4% to $65.28/bbl. Copper is 0.4% higher.

- Later Fed Chair Powell continues his testimonies. The Fed’s Goolsbee, ECB’s Donnery and BoE’s Lombardelli speak. US May new home sales/permits print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 25/06/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 25/06/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/06/2025 | 0700/0900 | ** | PPI | |

| 25/06/2025 | 0700/0900 | *** | GDP (f) | |

| 25/06/2025 | 0845/0945 | BOE Lombardelli At BOE MonPol Conference | ||

| 25/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/06/2025 | 0900/1000 | BOE Pill On Panel At BOE MonPol Conference | ||

| 25/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 25/06/2025 | 1230/1330 | BOE Lombardelli Chairs Riksbank's Breman Speech At BOE MonPol Conf | ||

| 25/06/2025 | 1400/1000 | *** | New Home Sales | |

| 25/06/2025 | 1400/1000 | *** | New Home Sales | |

| 25/06/2025 | 1400/1000 | Fed Chair Jay Powell | ||

| 25/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 25/06/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 25/06/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 25/06/2025 | 1800/1400 | Federal Reserve Board Meeting | ||

| 26/06/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 26/06/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 26/06/2025 | 0830/0930 | BOE Breeden On UK Competetiveness Panel | ||

| 26/06/2025 | 0945/1145 | ECB De Guindos At Deutsch Bank Forum 2025 | ||

| 26/06/2025 | 0945/1045 | BOE Greene Chairs Panel On MonPol Communication | ||

| 26/06/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 26/06/2025 | 1100/1300 | ECB Schnabel At 'Wirtschaftsrat der CDU' Finanzmarktklausur | ||

| 26/06/2025 | 1100/1200 | BOE Bailey Keynote Speech At BCC Conference | ||

| 26/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 26/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 26/06/2025 | 1230/0830 | * | Payroll employment | |

| 26/06/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/06/2025 | 1230/0830 | *** | GDP | |

| 26/06/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 26/06/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/06/2025 | 1245/0845 | Richmond Fed's Tom Barkin | ||

| 26/06/2025 | 1300/0900 | Cleveland Fed's Beth Hammack |