US TSYS: Asia Wrap - Front End Yield Extends Lower

The TYU5 range has been 111-17+ to 111.22 during the Asia-Pacific session. It last changed hands at 110-19+, down 0-01+ from the previous close.

- The US 2-year yield has moved lower trading around 3.79%, down 0.03 from its close.

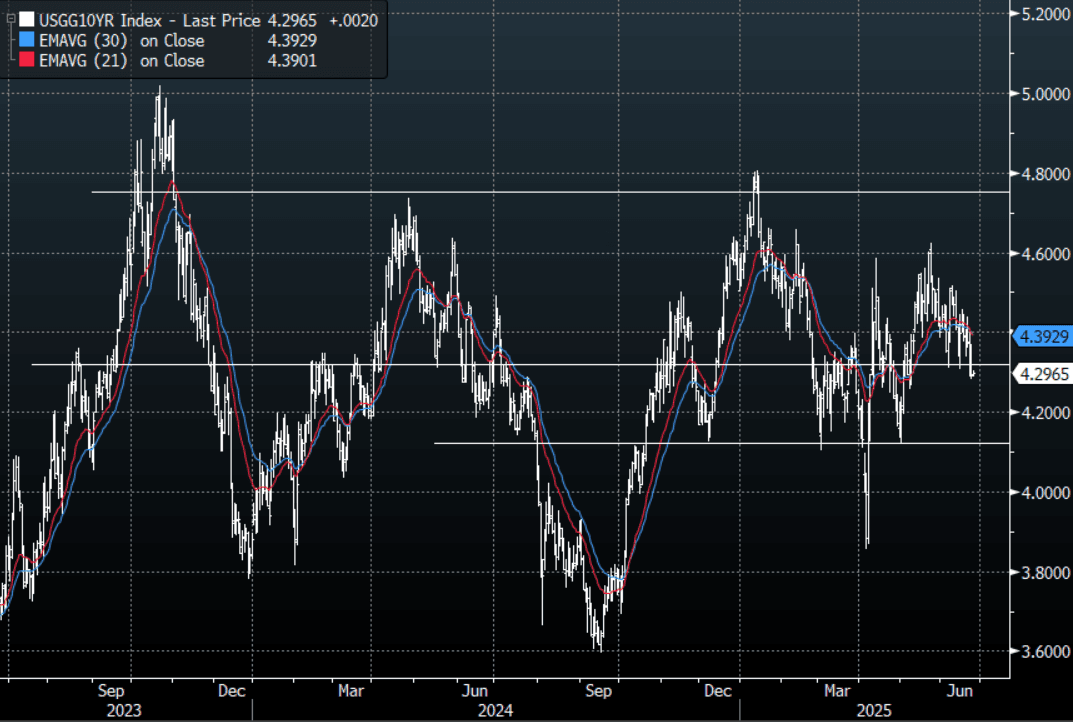

- The US 10-year yield is relatively unchanged around 4.30%.

- This has seen the yield curve steepen: 2s10s +3.61 at 50.143

- (Bloomberg) - US bond investors are too complacent about inflation and the Fed’s fears it will reaccelerate. Expectations for the decline in yields to accelerate look optimistic given that President Trump’s tax-and-spending bill may boost supply. Inflation is also likely to accelerate ahead of the next Fed meeting. Both this week’s core PCE print for May and the June Core CPI data due in the middle of next month are forecast to show higher readings.

- FED - FOMC sitting member Schmid, Kansas Fed, affirmed Chair Powell’s comments to the Senate that it is best to watch and wait to assess the impact of tariffs and policy on the economy given its resilience, especially the labour market, rather than rushing to ease monetary policy.

- The 10-year yield was again seriously testing the 4.30% support overnight, a sustained move back below here is likely to see the move pick up momentum. 10-year yields would need to get back above 4.45/4.50% again to alleviate this downward pressure.

Data/Events: MBA Mortgage Applications, Building Permits, New Home Sales

Fig 1: US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Futures Trade Lower

TYM5 gapped lower on the open as President Trump agrees to an extension to July 9 for Europe. The range has been 109-24+ to 110-02+ during the Asia-Pacific session. It last changed hands at 109-28, down 0-06 from the previous close.

- No Cash trading today

- The EU is ready to advance talks and needs until July 9 to reach a good deal, Ursula von der Leyen said on X. https://x.com/vonderleyen/status/1926729529436913794

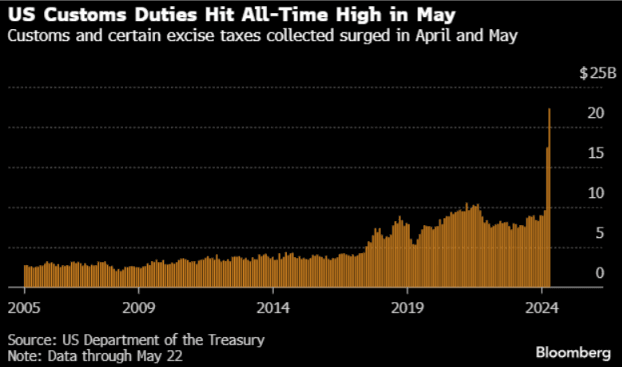

- (Bloomberg) -- “The Treasury’s latest fiscal statement is a reminder for financial markets that, despite the 90-day pause in the April 2 duties, levies have increased and they remain a risk for the economic outlook.”

- “Tariff income from excise taxes surged on May 22 to a record $22.3 billion, the first daily report to show the impact of new rates, according to the Treasury report. The one-day increase of about $16.5 billion was more than three times what was collected on the same day in May 2024 and up from $11.7 billion that was collected on April 22.” See Graph below.

The 10-year found sellers back towards 4.45% on Friday night and then moved higher to close back above 4.50%. Dips look likely to see supply in the short-term, should yields hold above 4.40% the target looks to be the 4.75% area. Watch for any announcements relating to the SLR, this could cause a knee jerk to a market that is already quite short.

Fig 1: US Customs Duties

Source: MNI - Market News/Bloomberg

STIR: Expected YE AU-NZ Official Rate Diff Continues To Narrow

RBNZ-dated OIS pricing was little changed across meetings today.

- Markets continue to price in 25bps of easing for Wednesday’s meeting, with a total of 64bps expected by November 2025.

- However, rates remain 2–18bps higher than levels observed prior to the Q1 CPI release on April 17.

- Amid firmer NZ rates and softer Australian rates—following last week’s dovish RBA pivot and Tuesday’s rate cut—the expected year-end policy rate differential between Australia and New Zealand has narrowed by 20–25bps over the past week, currently standing at +23bps.

Figure 1: RBA & RBNZ Official Rate Profile (%)

Source: MNI - Market News / Bloomberg

USD: BBDXY Focus Turning Towards Testing Pivotal 12000

The BBDXY range Friday night was 1210.77 - 1218.08, Asia is currently trading around 1208. The USD has opened weak again in early Monday morning trading in Asia with another leg lower.

- What stood out from the price action on Friday was how well the EUR held up in the face of a potential 50% increase in tariffs, and it was again the USD that took the brunt of the impact. This clearly shows the market's current outlook and leans into the growing “sell America “ theme.

- The EU is ready to advance talks and needs until July 9 to reach a good deal, Ursula von der Leyen said on X. https://x.com/vonderleyen/status/1926729529436913794

- Deutsche Bank put out a note that the Dollar would need to depreciate by up to 40% in order to eliminate the US deficit. “ If the average real exchange rate appreciation of 40% over the past 15 years were to reverse, it could likely restore the deficit to a zero balance, but the policy measures required may far exceed the simple implementation of tariffs.” https://x.com/Barchart/status/1925995602552275398

- Andreas Steno Larsen on X : “ A 25-30% weaker USD (over the next 1-2 years) solves most of Trump's problems, trade deficits will vanish. https://x.com/AndreasSteno/status/1925974036552499565

- These views highlight the broad consensus that the USD is set to embark on a decent move lower as the world reduces its exposure to the US and repatriates a lot of these flows.

We are approaching some key Weekly support towards the 1200 area in the BBDXY. A break below here could signal the move is about to accelerate.

Fig 1: Dollar Leads Swings in the US external balance

source : Deutsche Bank/Barchart on X - https://x.com/Barchart/status/1925995602552275398