FOREX: Asia FX Wrap - BBDXY Finds Some Demand Towards 1200, For Now

The BBDXY has had a range of 1200.25 - 1202.09 in the Asia-Pac session, it is currently trading around 1202. The BBDXY has found some demand back towards the 1200 area in a very quiet Asian session, +0.04%%. The BBDXY extended its move lower again overnight, the price action was very revealing and points to a market that is very quick to reinstate USD shorts with conviction pretty high for a move lower. “The BOE’s Andrew Bailey and Dave Ramsden warned that the labor market is cooling and pay pressures are easing in one of the strongest signs yet that the central bank is on course to cut rates again this summer”(BBG).”Goldman said the dollar will extend its worst start to a year as foreign investors boost FX hedges.”(BBG)

- EUR/USD - Asian range 1.1605 - 1.1631, Asia is currently trading 1.1615. The EUR remains well supported on dips, potential USD demand today with corporate month-end. While the USD remains on the back foot the EUR will continue to be supported first support back towards 1.1500.

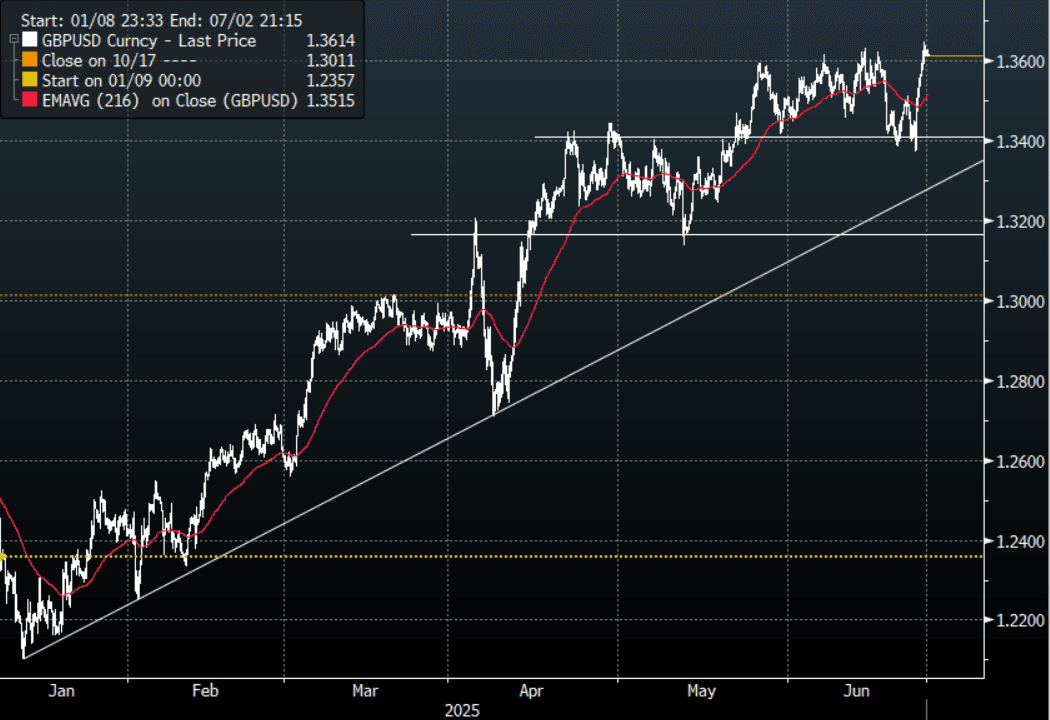

- GBP/USD - Asian range 1.3611 - 1.3629, Asia is currently dealing around 1.3615. The GBP again found solid demand around its 1.3400 support and has made new highs above 1.3600 looking for the momentum to carry it through its weekly pivot.

- USD/CNH - Asian range 7.1604 - 7.1711, the USD/CNY fix printed 7.1668. Asia is currently dealing around 7.1680. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.01%, Gold $3327, US 10-Year 4.297%, BBDXY 1202, Crude oil $65.20

- Data/Events : Spain GDP & PPI, France Consumer Confidence

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Bullion Slightly Lower On Better Risk Tone Following Tariff Delay For EU

Gold prices are moderately lower during today’s APAC session after rising close to 2% on Friday. They are down 0.2% to $3350.20/oz but off the intraday low of $3331.62 which followed some pullback in safe-have flows after news that the US and EU would continue to work towards a trade deal and the threat of a 50% US tariff on June 1 was postponed until July 9. The USD index is down 0.2%.

- Despite today’s lower gold price due to the better risk tone following more positive trade talk, it is likely to continue to find support from the US given ongoing trade negotiations are likely to be bumpy. There are also concerns over the fiscal position after the House passed the tax bill which now faces the Senate. Global relations remain fraught especially in the Middle East and Russia/Ukraine.

- Regional equities are mixed with the Hang Seng down 1.0% but KOSPI up 1.3% and S&P e-mini +1.0%. Oil prices are slightly higher with WTI +0.4% to $61.76/bbl. Copper is up 0.8% but iron ore is down to around $97/t. Silver has been range trading and is little changed.

- The US and UK are closed today for holidays. ECB President Lagarde speaks later.

JPY: Asia Wrap - Focus Turning Back To Key 140.00 Area

The Asia-Pac range has been 142.23 - 143.08, Asia is currently trading around 142.65. The brief bounce early doors this morning saw a wall of selling back above 143.00 and USD/JPY has spent the remainder of the session under pressure.

- “Neel Kashkari said major shifts in US trade and immigration policy are creating uncertainty for the Fed to move on interest rates before September.”(BBG)

- “Nvidia’s earnings this week could serve as a barometer, with the world’s most valuable chipmaker expected to post another quarter of strong growth. Revenue from its core chip business is forecast to rise over the next four quarters, and options pricing implies a post-earnings move of more than 7%, according to data curated by Bloomberg.”(BBG)

- (Bloomberg) - “Long-term Japanese yields are set to climb further with JGB traders facing a 40-year debt auction, followed by Tokyo inflation data this week.”

- USD/JPY again struggled to hold onto any gains above 143.00 this morning, fresh USD/Asia selling was seen with the USD broadly lower in our session as the tariffs on Europe are extended to July 9.

- The price action last week shows the market is still much more comfortable selling rallies, resistance is now back towards 144.00/145.00. The focus will turn once more to the pivotal 140.00 area, a break of which will open a much deeper move lower.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 144.00($1.06b), 143.00($713m) Upcoming Close Strikes : 143.00($1.71b May 28), 139.75($1.56b May 29).

CFTC data shows Asset managers maintained their already extensive JPY longs, and leveraged funds continue to build on their newly initiated shorts.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

BONDS: NZGBS: Bull-Flattener, US Tsys Out Today, RBNZ Policy Decision On Wed

NZGBs closed near session bests, showing a bull-flattener, with benchmark yields 1-4bps lower.

- Total new residential mortgage lending in New Zealand fell to NZ$7.58bn in April from NZ$8.49bn in March, according to RBNZ data.

- TYM5 gapped lower on the open as President Trump agrees to an extension to July 9 for Europe. The range has been 109-24+ to 110-02+ during the Asia-Pacific session. It last changed hands at 109-28, down 0-06 from the previous close. No cash US tsys today.

- Swap rates closed 1-3bps lower.

- Tomorrow, the local calendar will be empty

- RBNZ-dated OIS pricing was little changed across meetings today. Markets continue to price in 25bps of easing for Wednesday’s meeting, with a total of 64bps expected by November 2025. However, rates remain 2–18bps higher than levels observed prior to the Q1 CPI release on April 17.

- Amid firmer NZ rates and softer Australian rates—following last week’s dovish RBA pivot and Tuesday’s rate cut—the expected year-end policy rate differential between Australia and New Zealand has narrowed by 20–25bps over the past week, currently standing at +23bps.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-36 bond.