MNI US Macro Weekly: Not-So-Hot Summer For Economic Activity

Jun-27 19:29By: Tim Cooper and 1 more...

Federal Reserve+ 1

Download The Full Report Here

Executive Summary:

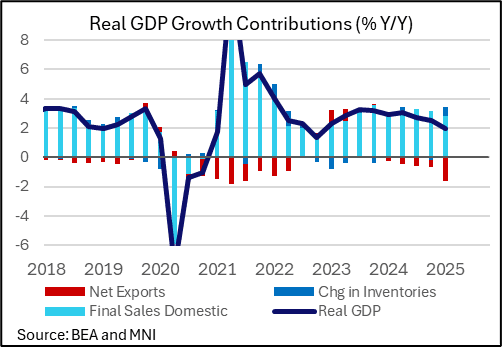

- Weaker private domestic demand was a key theme in the “hard” data this week. Not only was there a lower revision to Q1 GDP led by private consumption, we also saw a surprisingly sharp pullback in monthly PCE expenditure in May (a counterpoint to stronger-than-expected core PCE inflation after a soft April).

- Housing market data continued to deteriorate, and while initial jobless claims came in surprisingly low, continuing claims continued their rise, and in another warning sign for employment, the Conference Board’s consumer survey implied a further cooling in labor market conditions.

- In short, we came out of the week with the sense that economic activity was a little weaker through the first 5 months of the year than had previously been thought: the Atlanta Fed’s GDPNow estimate for Q2 fell to 2.9% from 3.4% last week and 3.8% a month ago, not a great rebound following Q1’s -0.5%.

- There was a deluge of post-June meeting Fed commentary, including Chair Powell’s congressional testimony. Most speakers again pointed to the need to wait for at least a couple more months of data before deciding whether it’s appropriate to ease rates, heavily implying that a July cut is off the table.

- The biggest single move of the week in rates though came following Gov Bowman’s comments that she could support a rate cut in July – this almost immediately added 7bp to the 2025 rate cut path. To be sure, she along with Gov Waller who last week eyed a July cut are the outliers, with no other FOMC participants appearing to see a cut before the fall (and it’s seen by markets as having <20% implied probability).

- Against this backdrop, Fed rate cut pricing increased notably this week, with an additional 13bp of cuts priced through end-year vs last Friday, and around one full 25bp cut added to the easing cycle.

- The data, the market pricing, and the Fed Speak are setting up for a resumption of the easing cycle in September (now almost 28bp priced), with the 65bp cumulative through December suggesting not just two but potentially three cuts by end-year.

- Next week’s July 4 abbreviated schedule brings one of two remaining employment reports before the July decision, and while jobs growth is seen slowing (to 110k from 139k prior), most attention may be on whether unemployment will finally tick up to 4.3% after being agonizingly close in May (4.244%).

- That said, it would take a fairly significant surprise to the weak side to reignite any chance of a July Fed rate cut. We also get multiple labor market data points in the days preceding the release, including ISM Manufacturing Employment, Challenger job cuts and ADP payrolls for June, and JOLTS job openings

Outside of Nonfarm Payrolls, the ISM Manufacturing and Services reports for June will be the key data of the week, and both are seen improving versus May.