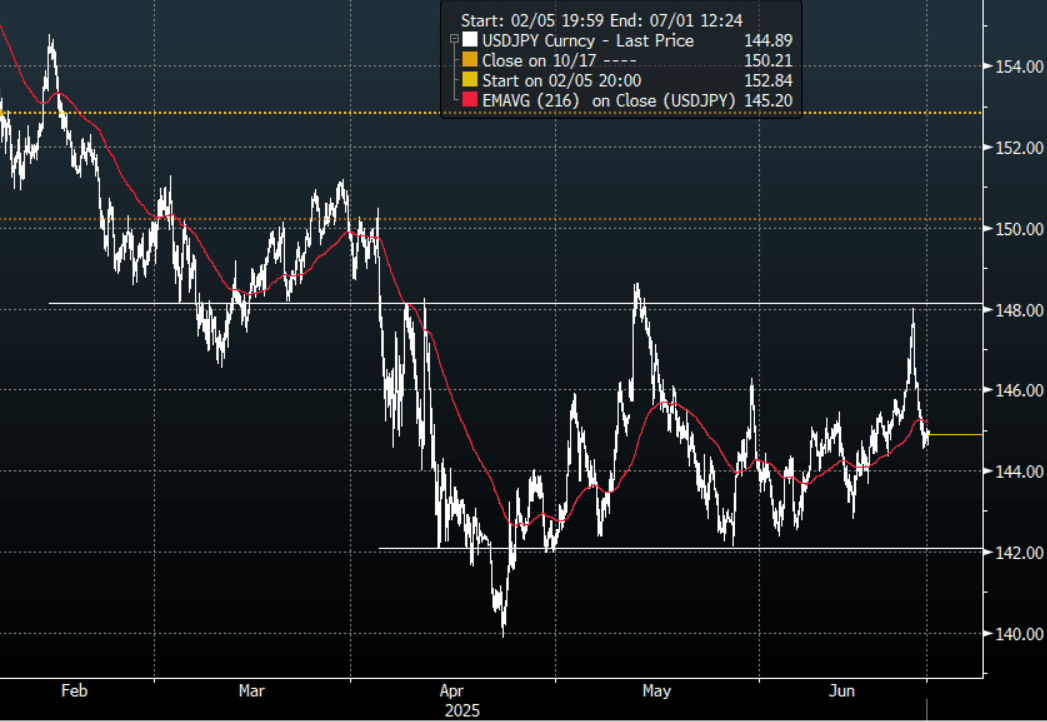

JPY: Asia Wrap - USD/JPY Finds Support Back Towards 144.50 As Oil Stabilises

The Asia-Pac USD/JPY range has been 144.61 - 145.04, Asia is currently trading around 144.90. USD/JPY found some demand back towards the 144.50 area when market tested lower on Hawkish comments from BOJ board member Naoki Tamura. The capitulation in oil also seems to have seen its momentum stall for now. The price action suggests any bounces will be met with sellers, corporate month-end USD demand might give them that opportunity.

- (Bloomberg) - “BoJ board member Naoki Tamura signaled a more hawkish stance on Wednesday, suggesting the Bank's 2% inflation target could be achieved earlier than expected and calling for a steady normalisation of monetary policy and the BoJ's balance sheet.”

- “A few Bank of Japan board members supported steadily reducing the Bank's JGB holdings, though concerns over moving too quickly were also raised, according to the summary of opinions from the June 16-17 policy meeting released Wednesday.”(BBG)

- An ugly daily shadow points to a potential top being in place now and highlights how quick the market is to return to selling USD’s, we are testing the support this morning around 144.50 where some demand was seen overnight.

- Price now back in its wider 142.00 - 148.00 range, I am not sure that the brief spike higher would have seen positioning altered too much so the long JPY trade remains alive and well.

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.50($1.88b).Upcoming Close Strikes : 142.00($1.32b June 26), 143.00($1.41b June 26)

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Bull-Flattener, US Tsys Out Today, RBNZ Policy Decision On Wed

NZGBs closed near session bests, showing a bull-flattener, with benchmark yields 1-4bps lower.

- Total new residential mortgage lending in New Zealand fell to NZ$7.58bn in April from NZ$8.49bn in March, according to RBNZ data.

- TYM5 gapped lower on the open as President Trump agrees to an extension to July 9 for Europe. The range has been 109-24+ to 110-02+ during the Asia-Pacific session. It last changed hands at 109-28, down 0-06 from the previous close. No cash US tsys today.

- Swap rates closed 1-3bps lower.

- Tomorrow, the local calendar will be empty

- RBNZ-dated OIS pricing was little changed across meetings today. Markets continue to price in 25bps of easing for Wednesday’s meeting, with a total of 64bps expected by November 2025. However, rates remain 2–18bps higher than levels observed prior to the Q1 CPI release on April 17.

- Amid firmer NZ rates and softer Australian rates—following last week’s dovish RBA pivot and Tuesday’s rate cut—the expected year-end policy rate differential between Australia and New Zealand has narrowed by 20–25bps over the past week, currently standing at +23bps.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-36 bond.

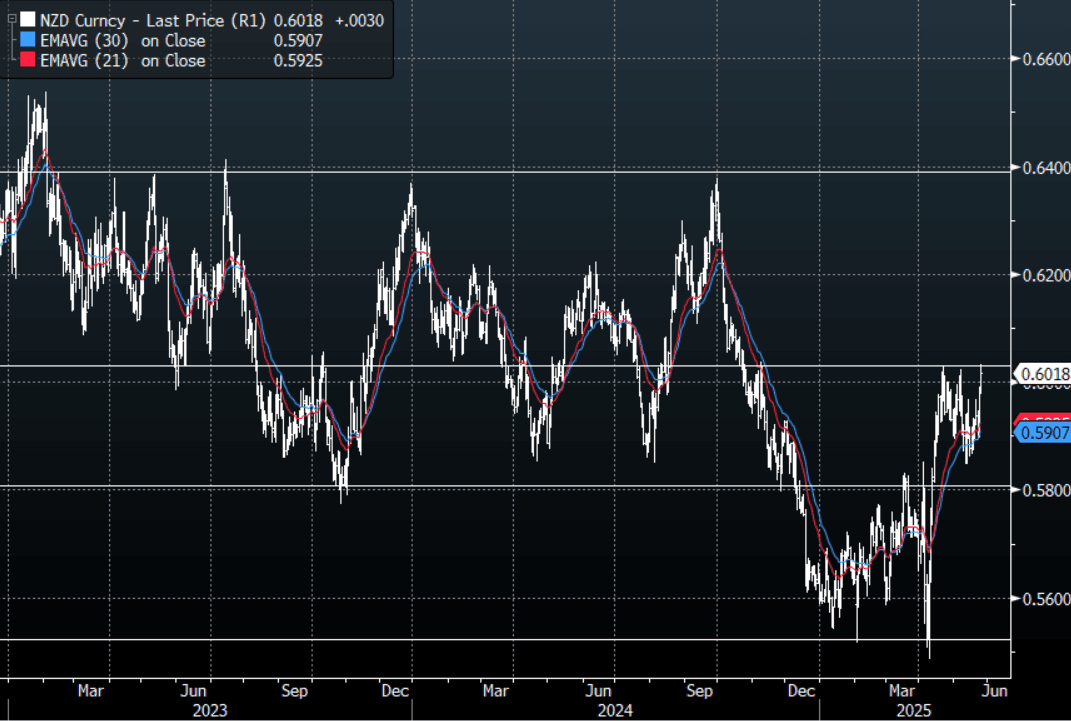

NZD: Asia Wrap - Looking To Break Higher

The NZD/USD had a range of 0.5981 - 0.6032 in the Asia-Pac session, going into the London open trading around 0.6020. The USD has opened weak again in early Monday morning trading in Asia with another leg lower.

- The RBNZ meets this week when the decision is announced on Wednesday with updated staff forecasts in the Monetary Policy Statement. It will be followed by a press conference which will be Hawkesby’s first as governor. The MPC is widely expected to cut rates 25bp to 3.25% bringing cumulative easing this cycle to 225bp. The OCR profile will be a focus as well as CPI given recent inflation developments.

- (Bloomberg) -- BNZ publishes new residential mortgage lending data for April, on its website. Lending to all borrowers NZ$7.58b, First-home buyers borrowed NZ$1.54b or 20.4% of total, Investors borrowed NZ$1.52b or 20% of total, There were 19,289 new mortgage commitments — down 12% m/m: RBNZ.

- The NZD has been bid for most of the Asian session benefitting from the broad USD sell-off and more fresh selling in USD/ASIA.

- The NZD continues to trade in a 0.5850/0.6050 range, could this latest round of USD selling provide it with the momentum to break this week ? As the “sell America” trade gathers pace.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break here could provide the spark for the next leg higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5980(NZD513m May 26), Upcoming Close Strikes : 0.5725(NZD1.09b May 28)

- CFTC Data showed Asset managers maintaining their shorts, while the leveraged community added a decent clip back to their own short.

AUD/NZD range for the session has been 1.0819 - 1.0857, currently trading 1.0830. A sustained break above 1.0930 is needed to turn the focus higher, until then expect supply on bounces.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

CHINA: Onshore News Focuses On Appeal Of Local Bonds Over US Tsys

- China's bond market has been resilient in the face of global volatility in yields, proving that it remains a low correlation bet.

- The ongoing support of the Central Bank through the daily management of liquidity in the interbank market is a key contributor to this stability.

- A report in the China Securities Journal supports this view, describing China's monetary policy as supportive.

- China’s 10-year government bond yields have traded in a 1.68%-1.72% range over the past week, while its 30-year yields stayed at 1.86%-1.89%. The relative stable performance, which was aided by the PBOC’s strengthening of counter-cyclical adjustments, stood in contrast to recent sharp increases in the yields of US and Japanese government bonds

The report points to Moody's downgrade of the US sovereign credit rating, the cold reception of US Treasury auctions, and the market's increasing concerns about the US fiscal deficit have rapidly pushed up long-term US Treasury yields. "US Treasury bonds are facing many negative factors recently, with weak demand being the core factor, Moody's downgrade of US Treasury rating, the uncertainty of Fed policy the backdrop of rising inflation expectations, and the US Trump administration's push for a tax cut bill are risk points to investing in treasuries.