AUD: Asia Wrap - CPI Print Finds Bids Sub 0.6500

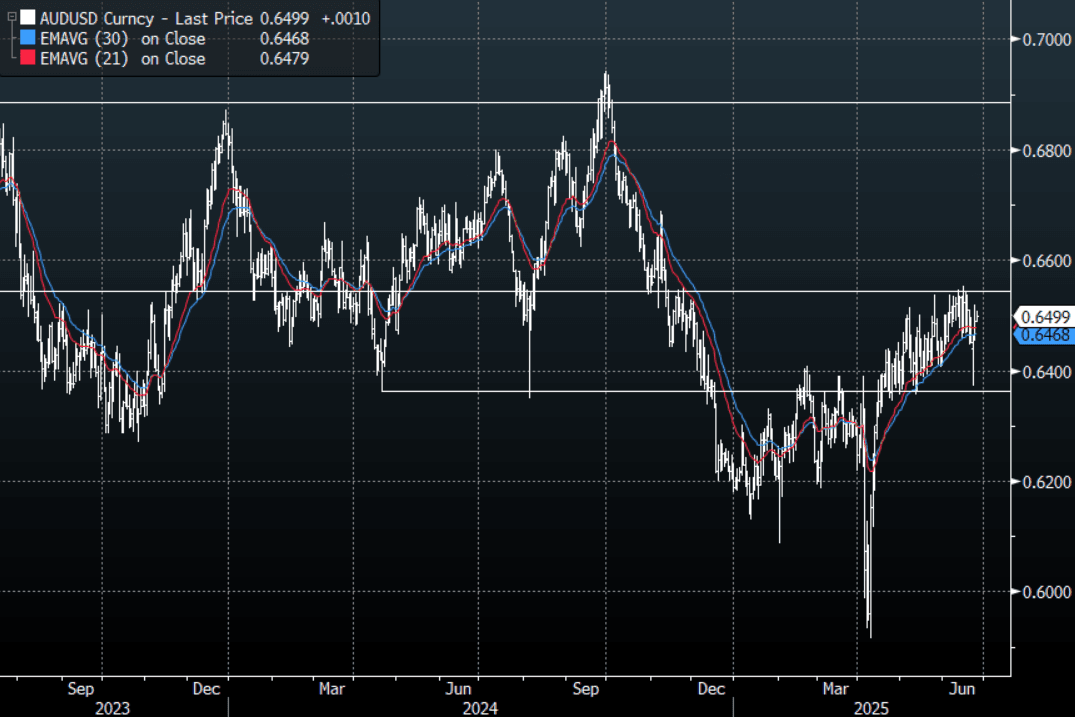

The AUD/USD has had a range of 0.6489 - 0.6508 in the Asia- Pac session, it is currently trading around 0.6500, +0.15%. The AUD attempted to move lower on the CPI print but found bids sub 0.6500 and clawed back all its losses. A quiet session sees AUD/USD continue to trade with an underlying bid tone. We are approaching the corporate month-end and this normally results in a demand for USD's so perhaps better levels could be seen for AUD buyers.

- AUSTRALIA DATA: Trimmed Mean Inflation Lowest Since 2021 Raising Cut Hopes. May headline CPI inflation was flat on the month, seasonally adjusted, driving a 0.3pp moderation in the annual rate to 2.1% driven by a broad-based easing across major components. The trimmed mean moderated to 2.4% y/y from 2.8%, the lowest since November 2021. The RBA decision is on July 8 and this data is likely to increase expectations of another rate cut but the Board prefers the quarterly CPI (due July 30) and updated staff forecasts are not provided until August.

- The AUD/USD bounced hard off its support and is now back to potentially testing the top end of its range as the USD comes back under pressure.

- We are approaching the corporate month-end and this normally results in a demand for USD’s so perhaps better levels could be seen over the course of the next day or so for those wanting to express a long AUD position.

- Price remains in the wider 0.6350 - 0.6550 range for now. The AUD needs a sustained break above 0.6550 to potentially start building towards a move higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6500(AUD2.11b June 26), 0.6425(AUD776m June 30).

- AUD/JPY - Today's range 93.98 - 94.28, it is trading currently around 94.20. Choppy price action as the pair establishes a range between 92.00 - 96.00. Should risk build on this move, focus could turn back to the 96.00 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

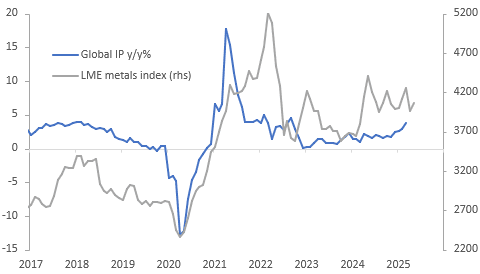

GLOBAL MACRO: IP Growth Rises In March, Outlook Uncertain

CPB data showed that global IP volumes rose 0.5% m/m to be up 3.7% y/y in March after 0.8% & 2.9% y/y respectively. This was the fastest annual growth rate since September 2022, a time when the global economy was recovering from Covid. The pickup in IP seen since December has lagged global trade growth. The global manufacturing PMI suggests that IP is likely to slow in the coming months but metal prices suggest that it could strengthen before stabilising.

- Some of the frontloading of trade to beat US tariffs may be coming out of inventories and thus IP hasn’t picked up to the same degree. Thus, IP may not slow as much in the second half of the year consistent with metal prices remaining at elevated levels.

Global IP vs LME metal prices

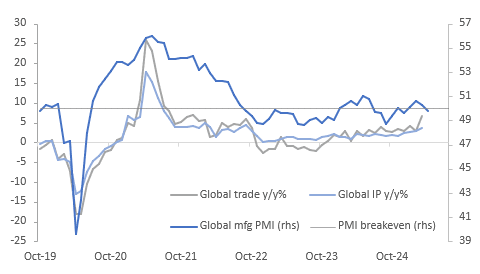

- The S&P Global manufacturing PMI signalled slightly positive growth in activity in Q1 2025 but it fell to 49.8 in April from 50.3 signalling a slight contraction. The US’ reciprocal tariffs were announced on April 2 and likely weighed on the index. There could be some unwind in the May PMI, released on June 3, due to the tariff delay.

- Central banks assume that even if trade agreements are reached by July, uncertainty in H1 2025 will weigh on demand. If deals aren’t agreed, then global growth could be significantly lower.

Global growth

US TSYS: Asia Wrap - Futures Trade Lower

TYM5 gapped lower on the open as President Trump agrees to an extension to July 9 for Europe. The range has been 109-24+ to 110-02+ during the Asia-Pacific session. It last changed hands at 109-28, down 0-06 from the previous close.

- No Cash trading today

- The EU is ready to advance talks and needs until July 9 to reach a good deal, Ursula von der Leyen said on X. https://x.com/vonderleyen/status/1926729529436913794

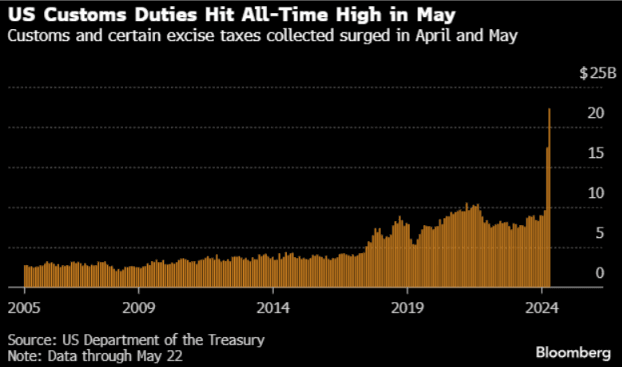

- (Bloomberg) -- “The Treasury’s latest fiscal statement is a reminder for financial markets that, despite the 90-day pause in the April 2 duties, levies have increased and they remain a risk for the economic outlook.”

- “Tariff income from excise taxes surged on May 22 to a record $22.3 billion, the first daily report to show the impact of new rates, according to the Treasury report. The one-day increase of about $16.5 billion was more than three times what was collected on the same day in May 2024 and up from $11.7 billion that was collected on April 22.” See Graph below.

The 10-year found sellers back towards 4.45% on Friday night and then moved higher to close back above 4.50%. Dips look likely to see supply in the short-term, should yields hold above 4.40% the target looks to be the 4.75% area. Watch for any announcements relating to the SLR, this could cause a knee jerk to a market that is already quite short.

Fig 1: US Customs Duties

Source: MNI - Market News/Bloomberg

STIR: Expected YE AU-NZ Official Rate Diff Continues To Narrow

RBNZ-dated OIS pricing was little changed across meetings today.

- Markets continue to price in 25bps of easing for Wednesday’s meeting, with a total of 64bps expected by November 2025.

- However, rates remain 2–18bps higher than levels observed prior to the Q1 CPI release on April 17.

- Amid firmer NZ rates and softer Australian rates—following last week’s dovish RBA pivot and Tuesday’s rate cut—the expected year-end policy rate differential between Australia and New Zealand has narrowed by 20–25bps over the past week, currently standing at +23bps.

Figure 1: RBA & RBNZ Official Rate Profile (%)

Source: MNI - Market News / Bloomberg