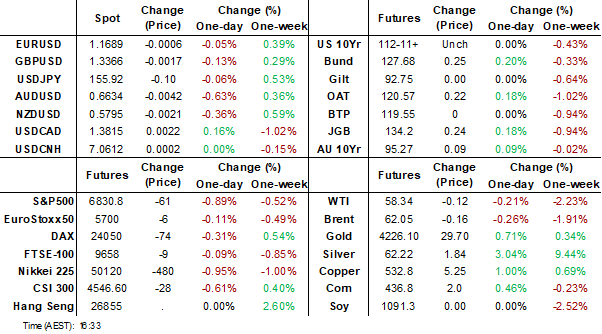

MNI EUROPEAN MARKETS ANALYSIS: Oracle Sends Tech Stocks Lower

- As markets digested a less hawkish FED than feared, a warning from U.S. cloud computing giant Oracle about lower-than-expected profit and revenue outlooks (due to higher infrastructure spending) has seen profit taking in the tech sector today with falls in AI-related stocks and major tech firms like Japan's Softbank (down -7%), Korea's SK Hynix (down -2.9%) and Taiwan's TSMC (down -2%).

- The USD outperformed higher beta plays on stock weakness, whilst the rally in US treasury yields continued, as fear of a hawkish FED receded.

- Australia was the main data focus with November's Unemployment steady at 4.3% and early month exports in Korea were strong. Markets look ahead to the monetary policy committee meeting in the Philippines soon where expectations are for a further cut in the BSP O/N borrowing rate to 4.50%.

- Looking ahead Europe's attention will turn to Sweden inflation and the decision on rates from Switzerland whilst US investors will focus on Initial Jobless Claims.

US TSYS: Yields Lower as Hawkish Fears Recede

US bond futures gained further in the Asia afternoon with the 10-Yr breaking above a key technical level. TYH6 is up +09 to 112-16, trading through the 100-day EMA of 112-14+. Topside resistance now is the 20-day EMA of 112-23+.

Cash is strong also with yields lower across the curve. Yields were lower at the opening of the trading day though appeared to falter at lunch before buyers took over again and longer bonds performed well.

- The 2-Yr is down -1bp at 3.53%

- The 5-Yr is down -2.1bps at 3.712%

- The 10-Yr is down -2.5bps to 4.125%

- The 30-Yr is down -2.2bps to 4.766%

The 10-Yr has consolidated back below the upper end of the recent range. As investors' concerns over a potentially hawkish outlook from the FED recede, the 10-Yr retreated and is now firmly back in the 4.00-4.20% range.

The market will turn it's attention tonight to Initial Jobless claims. Current forecasts are for a modest increase to 220k from 191k for the prior release.

There will be a US$69bn 17-week auction, a US$85bn 4-week auction, a US$80bn 8-week auction and a US$22bn 30-Year re-opening.

JGBS: Yields Lower As Risk-Off Grips Markets, 20Y Auction Sees Strong Demand

JGB futures are stronger but off session highs, +25 compared to settlement levels, as risk-off sentiment grips markets.

- US equity futures have been weighed by the tech side, with Nasdaq futures down 1.5% at one stage (last -1.15%). Late US Wednesday time Oracle results weighed on the market and spilled over to Nvidia in after-hours trading.

- A Reuters poll shows that 90% of economists expect the BOJ to raise its key interest rate to 0.75% in December, with 69% forecasting it will reach at least 1.0% by September 2026, 77% disapprove of the government financing its supplementary budget largely with new debt, and next year’s labour talks are expected to yield a 5.0% pay increase, slightly below this year’s 5.25%.

- Cash US tsys are 2-3bps richer in today's Asia-Pac session.

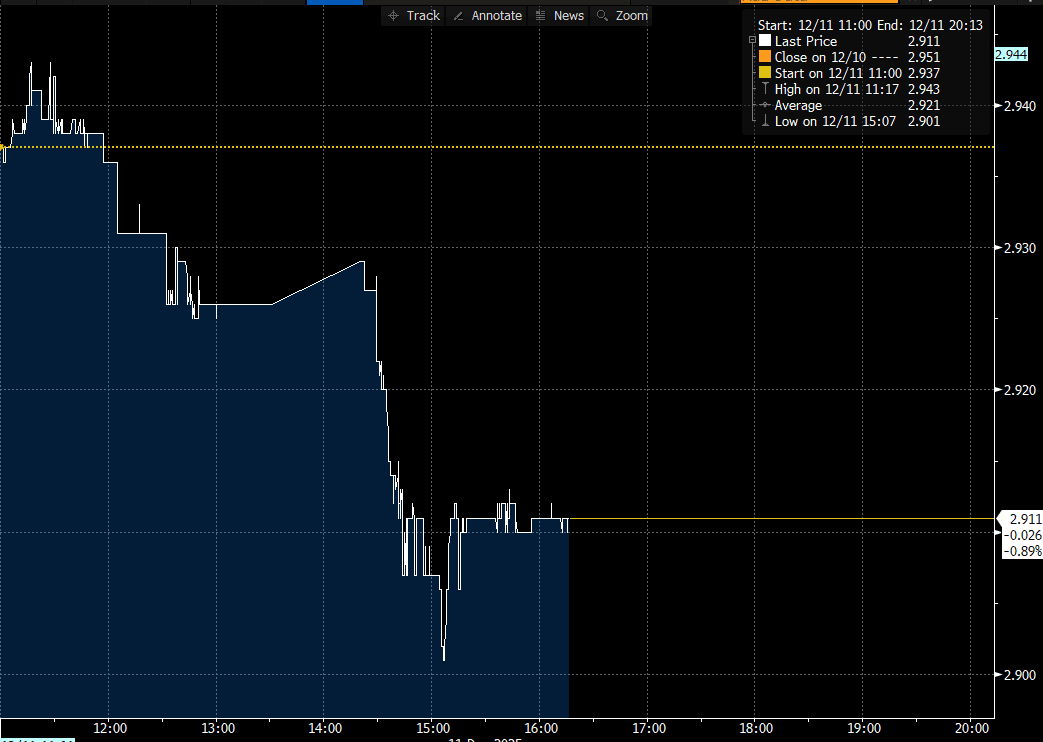

- Cash JGBs are 1-4bps richer across benchmarks, with the 20-year leading after today’s supply (see chart).

- The 20-year JGB auction drew its strongest demand since 2020. The low-price outperformed dealer forecasts, which were set at 97.10 according to a Bloomberg poll. Moreover, the cover ratio increased to 4.0958x from 3.2825x in the previous outing.

- Swap rates are ~1bp lower.

- Tomorrow, the local calendar will see October IP and Capu data.

Source: Bloomberg Finance LP

JAPAN DATA: Local Investors Buy Offshore Bonds, Indifferent On Equities

In terms of Japan outbound flows, local investors returned to offshore bond purchases last week. This marked net buying in 4 out of the last 5 weeks. Since the start of Oct, cumulative net flows for this segment are still negative though. Global bond returns have largely tracked sideways over this period and remain sub 2025 highs. Focus will be on whether we see a move higher into year end following the overnight Fed outcome, although the market may await for 2026 data trends to break us out of recent ranges for longer dated UST yields. In the equity space, we saw local investors sell down offshore holdings, but only modestly. Net flows have been quite modest over the past few weeks.

- In terms of inflows into Japan assets, we saw continued net buying of local stocks, but at a reduced pace. The general trend since the start of Q4 has been net buying in this space, as Japan stocks have remain supported on dips. The NKY 225 remains off early Nov highs.

- In the bond space offshore investors sold local bonds, although this only partially unwound the prior week inflow. Cumulative inflows have been evident since the start of Q4, but not to the same degree as bond inflows.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Dec 5 | Prior Week |

| Foreign Buying Japan Stocks | 96.8 | 655.7 |

| Foreign Buying Japan Bonds | -442.6 | 1065.8 |

| Japan Buying Foreign Bonds | 452.9 | -771.3 |

| Japan Buying Foreign Stocks | -64.5 | 78.8 |

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Strong Rally After Jobs Data, 3/10 Curve Flattener Has More To Run

ACGBs (YM +9.0 & XM +9.0) are stronger after today's employment report.

- The November labour market data were softer, apart from the stable unemployment rate. However, the data is volatile and averages need to be considered.

- The RBA continues to see the jobs market as “a little tight”. Given the volatility, this release is likely to be consistent with the Board wanting more information.

- Cash US tsys are 1-3bps richer in today's Asia-Pac session.

- Cash ACGBs are 8-9bps richer with the AU-US 10-year yield differential at +59bps.

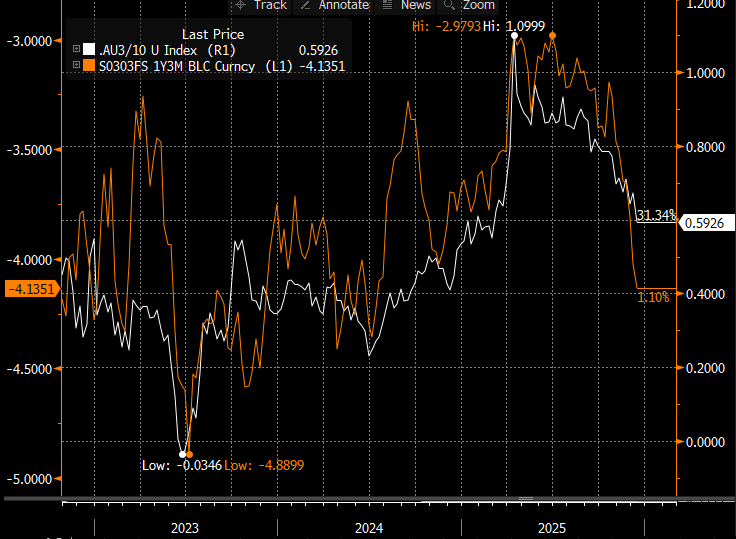

- The 3/10 curve continues to flatten, with the level now the flattest since March. The recent curve flattening has occurred alongside a steady rise in market forward expectations for the RBA cash rate. A simple regression of the 3s/10s curve against the 1Y3M rate over the past three years suggests the current curve is roughly 20bps too steep relative to its fair value (see chart).

- The bills strip has bull-flattened, with pricing +1 to +12.

- RBA-dated OIS pricing is softer after the data. Pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 24% for February to 93% by June and 170% by December 2026.

- Tomorrow, the local calendar will be empty.

Bloomberg Finance LP

AUSTRALIA DATA: Nov Jobs Market Softer But Volatile, More Data Needed

The November labour market data were consistently softer, apart from the stable unemployment rate. However, the data are volatile and averages need to be considered and they were mixed. The RBA continues to see the jobs market as “a little tight”. Governor Bullock said that the Board is likely to discuss a prolonged pause or hiking in 2026 dependent on the data as inflation and capacity pressures are rising. Given the volatility, this release is likely to be consistent with the Board wanting more information.

- There don’t seem to be special factors although the ABS notes some “operational challenges” for NSW data collection but it made adjustments and “there are no residual data quality concerns”.

- The fall in the labour force exceeded employment at -23k versus -21.4k driving a 0.2pp decline in the participation rate to 66.7%.

- The 3-month average in jobs fell slightly to +10.3k from +14k in October with Q4 growth at 1.4% y/y after Q3’s 1.5%, slightly above the RBA’s November Q4 projection of 1.3%.

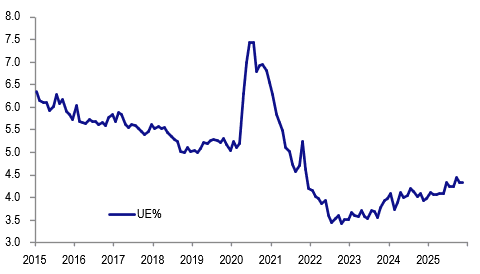

- The unemployment rate remained at 4.3% keeping the Q4 average at 4.3%, 0.1pp below the RBA’s Q4 forecast.

Australia unemployment rate %

Source: MNI - Market News/ABS

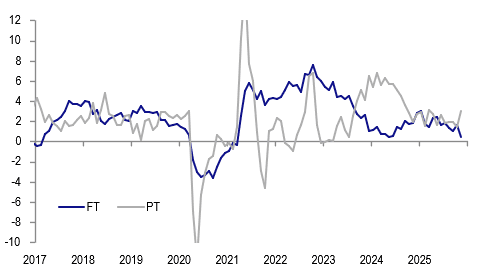

- Full-time (FT) jobs fell 56.5k unwinding October’s +53.6k while part-time (PT) rose 35.2k after -12.5k. The 3-month averages were steady.

- Hours worked were flat in November but 3-month momentum rose driven by both PT and FT. FT fell 0.2% m/m but the 3-month average annual rate was little changed at 1.3% y/y. PT hours were strong rising 0.7% m/m with momentum at 4.8% and growth up to 4.5% y/y from 3.1% driving the average to 3.1% y/y from 2.4% y/y.

- This growth in PT hours and employment may reflect employer caution if they are uncertain about the outlook. More data is needed to confirm this.

- The underemployment and youth unemployment rates also rose showing 0.2pp increases in the 3-month averages from October.

Australia employment y/y%

Source: MNI - Market News/ABS

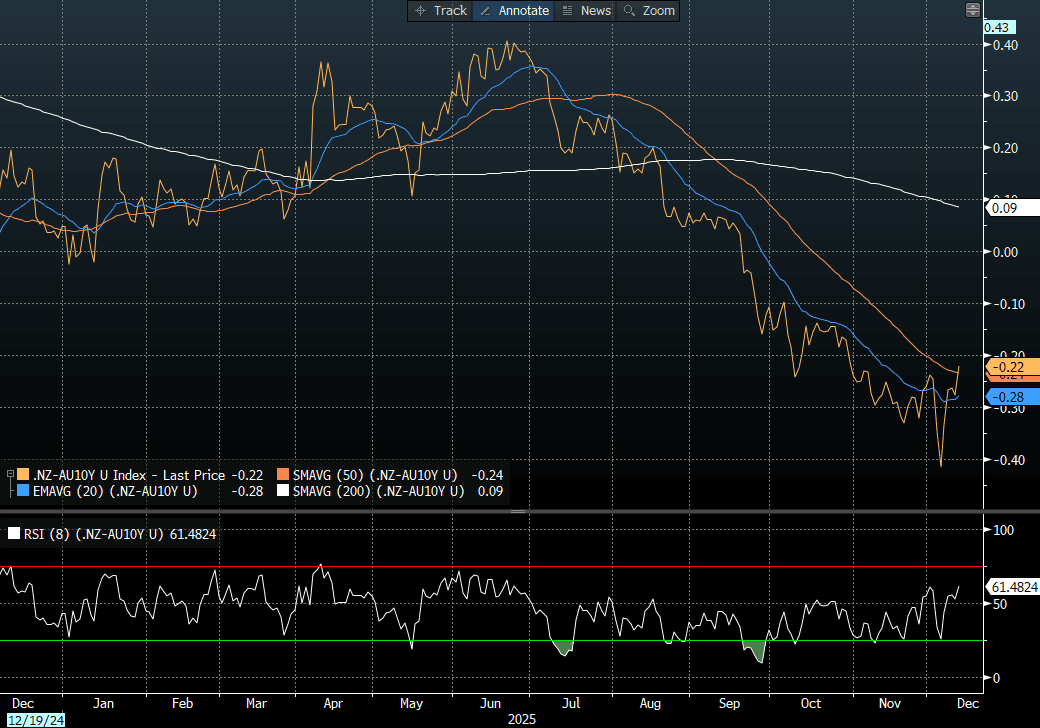

BONDS: NZGBS: Bull-Flattener But NZ-AU 10Y Diff Sharply Higher

NZGBs closed showing a bull-flattener, with benchmark yields 2-5bps lower. Nevertheless, yields remain 27-48bps higher than pre-RBNZ levels on 26 November.

- Today’s weekly supply shows solid to great demand, with cover ratios ranging from 3.33x (Apr-33) to 5.09x (May-30).

- On a relative basis, however, NZGBs underperformed their $-bloc counterparts, with the NZ-US 10-year yield differential 1bp higher, while the NZ-AU differential rose by 6bps. As the chart shows, the NZ-AU spread has rebounded sharply from its lowest level since 2020.

- A simple regression analysis of the NZ-AU 10-year yield differential against the NZ-AU 1Y3M spread over the past two years shows that the 10-year differential is around 6bps below fair value based on the regression model.

- Swap rates closed 4-5bps lower.

- RBNZ-dated OIS pricing closed little changed across meetings. 1bp of tightening is priced for February, while November 2026 assigns 61bps.

- Tomorrow, the local calendar will see BusinessNZ Manufacturing PMI.

Bloomberg Finance LP

FOREX: Risk Off Stabilizes USD Index, Yen Outperforms A$ & NZD

The USD BBDXY index sits up from post FOMC lows (1208.32), last near 1210.75, with risk off trends in the equity and crypto space driving outperformance versus higher beta plays. AUD/USD is off 0.60%, with the softer local jobs data for Nov also weighing. JPY and to a lesser extent CHF, have edged up versus the USD, in line with the risk off tones from the cross asset space.

- US equity futures have been weighed by the tech side, with Nasdaq futures down 1.5% at one stage (last -1.15%). Eminis were down 1%, last off -0.80%. Late US Wednesday time Oracle results weighed on the market and spilled over to Nvidia in after hours trading. The market remains sensitive to chip/AI related developments. Crypto is also weaker, down 2.5% for Bitcoin, although dips under 90k have been supported so far.

- AUD/USD is down 0.60%, last near 0.6635, close to session lows. The November labour market data were consistently softer, apart from the stable unemployment rate. However, the data are volatile and more data is needed to determine if there is a slowing. AUD/JPY is down 0.75%, last near 103.35/40, just up from session lows.

- The AUD/NZD cross is around 1.1450, off 0.25%. NZD/USD is back under the 0.5800 pivot.

- USD/JPY got to lows of 150.49, but now sits back at 155.75/80. We couldn't sustain the earlier break under the 20-day EMA.

- EUR/USD got to highs of 1.1707, but now sits back under 1.1690. For GBP.USD it has been a similar backdrop, last near 1.3365, after getting to 1.3392 earlier (fresh highs since mid Oct).

- Later US 6 December jobless claims and delayed September trade & inventories are released. The SNB decision is announced, the Eurogroup meeting takes place and BoE Governor Bailey speaks.

ASIA STOCKS: Oracle Warning Shakes Tech Heavy Bourses

A warning from U.S. cloud computing giant Oracle about lower-than-expected profit and revenue outlooks (due to higher infrastructure spending) has seen profit taking in the tech sector today with falls in AI-related stocks and major tech firms like Japan's Softbank (down -7%), Korea's SK Hynix (down -2.9%) and Taiwan's TSMC (down -2%). The warning overshadowed the U.S. Federal Reserve's decision to cut interest rates by 25 basis points to a target range of 3.75%–4.00% in what was generally considered a dovish tone emanating from the FED.

- After a moderately positive start to the week, the NIKKEI is down heavily today with fall of -0.85% and taking the index negative for the week. The NIKKEI now sits over 4% below the October high of 52,411.

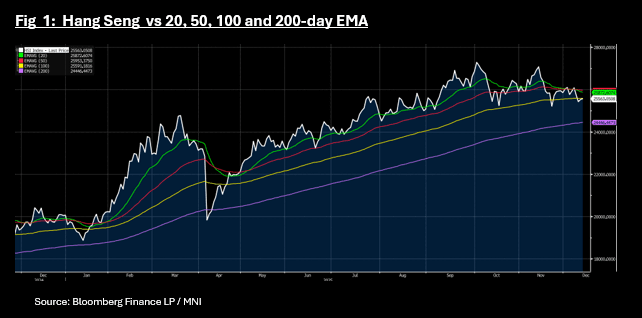

- China's onshore bourses are all down with the Hang Seng marginally positive. With onshore bourses all down -0.20% to -0.50% it took the HSI to lead with gains of +0.10% to reach 25,569 as it nears upside resistance via the 100-day EMA of 25,591

- Tech heavy bourses like the KOSPI and the TAIEX both fell with Taiwan down -1.1%, whilst the KOSPI was down a mere -0.12%

- India's NIFTY 50 has fallen the first four trading days of the week for its worst start to a week since September and is down -0.25% today.

- SE Asia bourses again a mixed with the FTSE Malay KLCI up +0.33% whilst the Jakarta Composite is down -0.25% and the SE Thai -1.1%

OIL: Gives Up Geopolitical Gains, IEA Report Later Could Focus Market On Surplus

Oil prices have given up their earlier session gains as risk appetite deteriorated. They got support yesterday from Fed easing, which is positive for energy demand, and the US seizure of a tanker off the coast of Venezuela, which according to the US attorney general was carrying sanctioned crude from Venezuela and Iran. Thursday sees OPEC and IEA reports released, which could refocus oil on supply/demand fundamentals.

- Brent is steady at around $62.20/bbl, close to the intraday low of $62.11 and off the earlier peak of $62.63. WTI is flat at around $58.46/bbl after falling to $58.39 following a high of $58.94.

- The IEA has been expecting a record 2026 surplus for some time but if it is revised higher or the more optimistic OPEC revises demand down or supply up, then oil prices are likely to be pressured.

- The US has been taking action against Venezuela due to its drug shipments and Maduro’s autocratic regime. The appropriation of the tanker is likely to dissuade other shippers from carrying Venezuelan crude reducing global supply. China is the main buyer of Venezuelan and Iranian oil. The government said it was an “act of piracy”.

- Later US 6 December jobless claims and delayed September trade & inventories are released. The SNB decision is announced, the Eurogroup meeting takes place and BoE Governor Bailey speaks.

PRECIOUS METALS: Gold Giving Up Post-Fed Gains, Silver New Record

Silver continues to outperform gold following the Fed’s cut but unchanged 2026 and 2027 rate profile. Gold has given up almost all of Wednesday’s gains in today’s APAC session possibly feeling pressure from the equity sell off and stronger greenback, while silver reached a new record high earlier. The US dollar is off the intraday low with the BBDXY +0.1% while the 2-year yield is slightly lower.

- Gold is down 0.3% to $4216.0/oz after reaching $4247.74 earlier. It fell to an intraday low of $4209.56, holding above initial support at $4155.2. With no change to the Fed outlook, bullion continues to range trade and will watch data closely for direction.

- Silver reached $62.390/oz during Thursday’s APAC session, a new record high, but short of resistance at $62.937, a Fibonacci projection. The metal is currently up 0.4% to $62.05. It has been outperforming on increased silver-backed ETF inflows given the tightness of the physical market. It has widespread use in renewable energy products.

- Equities are mixed with the S&P e-mini down 0.9% and NASDAQ -1.3% and CSI 300 -0.2%. Oil prices are flat with WTI at $58.44/bbl. Copper is up 0.5% and iron ore around $106.00/t.

- Later US 6 December jobless claims and delayed September trade & inventories are released. The SNB decision is announced, the Eurogroup meeting takes place and BoE Governor Bailey speaks.

LNG: US Gas Prices Stabilise As Large Inventory Drawdown Forecast

Natural gas is down this week but US prices stabilised on Wednesday driven by an expected large inventory drawdown while Europe fell because of expectations that recent mild weather will continue into the new year.

- US Henry Hub rose 1.1% to $4.625 but is still down 12.6% this week due to forecasts for higher temperatures going into the latter half of December. The benchmark reached $4.696 off the intraday low of $4.455.

- EIA data for gas inventories for last week are released today and expected to fall 167 bcf compared to the 5-year average to 5 December of -89 bcf, according to Bloomberg. At the end of November they were still 5.1% above average.

- European gas fell 2.4% to EUR 26.820 after rising 1.9% on Tuesday and is down almost 7% in December. Prices trended lower through yesterday to EUR 26.535 before recovering slightly.

- Storage levels continued to trend down falling 0.2pp to 71.6% on Tuesday as low prices are impacting LNG imports. Pipeline flows from Norway were impacted by unplanned maintenance.

CROSS ASSET: Risk Off In Equities/Crypto, Eminis Near 20-day EMA Support

Risk off evident in the equity space earlier, has accelerated somewhat in recent dealings. US futures sit just up from session worst levels. Eminis last off around 0.80%, Nasdaq futures down 1.25% (we were off 1% and 1.5% respectively at the lows). The session started off poorly following late Oracle news from Wednesday's US session. Via IBD: "Oracle earnings topped fiscal Q2 but revenue came in short. Capital spending was significantly higher than expected in Q2 and Oracle hiked full-year capex plans. Nvidia stock fell slightly late after Oracle's Larry Ellison said the tech giant has adopted "chip neutrality," buying Nvidia chips but also will use other options if customers prefer."

- Crypto weakness has also been a feature in recent dealings, Bitcoin back under 90k. This has likely added some pressure at the margins to broader risk trends, with intra-day swings in US equity futures and Bitcoin still reasonably well correlated.

- This is unwinding the post FOMC risk rally. Eminis are back near the 20-day EMA support point, although this hasn't been a strong inflection point for futures in recent months.

- In the FX space, AUD/JPY is down around 0.65%, last close to 103.50 (with the softer earlier jobs data weighing on A$ performance as well). AUD/USD is back under 0.6650.

- US yield losses are also a little larger but not beyond 2bps at this stage. The 10yr yield is close to 4.13%.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0830/0930 | *** | SNB Interest Rate Decision | |

| 11/12/2025 | 0950/0950 | BOE Bailey Pre-recorded Chat on Financial Stability | ||

| 11/12/2025 | 1000/1000 | BOE Bailey Gives Evidence At Covid-19 Inquiry | ||

| 11/12/2025 | 1100/0600 | *** | Turkey Benchmark Rate | |

| 11/12/2025 | - | *** | Money Supply | |

| 11/12/2025 | - | *** | Social Financing | |

| 11/12/2025 | - | *** | New Loans | |

| 11/12/2025 | - | ECB Lagarde and Cipollone at Eurogroup Meeting | ||

| 11/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 11/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 11/12/2025 | 1330/0830 | * | Household debt-to-income | |

| 11/12/2025 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 11/12/2025 | 1330/0830 | ** | Trade Balance | |

| 11/12/2025 | 1330/0830 | ** | Trade Balance | |

| 11/12/2025 | 1500/1000 | * | Services Revenues | |

| 11/12/2025 | 1500/1000 | ** | Wholesale Trade | |

| 11/12/2025 | 1500/1000 | ** | Wholesale Trade | |

| 11/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 11/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 11/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 11/12/2025 | 1800/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 12/12/2025 | 0430/1330 | ** | Industrial Production | |

| 12/12/2025 | 0700/0700 | *** | UK Monthly GDP | |

| 12/12/2025 | 0700/0800 | ** | Unemployment | |

| 12/12/2025 | 0700/0700 | ** | Trade Balance | |

| 12/12/2025 | 0700/0700 | ** | Index of Services | |

| 12/12/2025 | 0700/0700 | ** | Index of Production | |

| 12/12/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/12/2025 | 0700/0700 | ** | Output in the Construction Industry | |

| 12/12/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/12/2025 | 0745/0845 | *** | HICP (f) | |

| 12/12/2025 | 0800/0900 | *** | HICP (f) | |

| 12/12/2025 | 0930/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey |